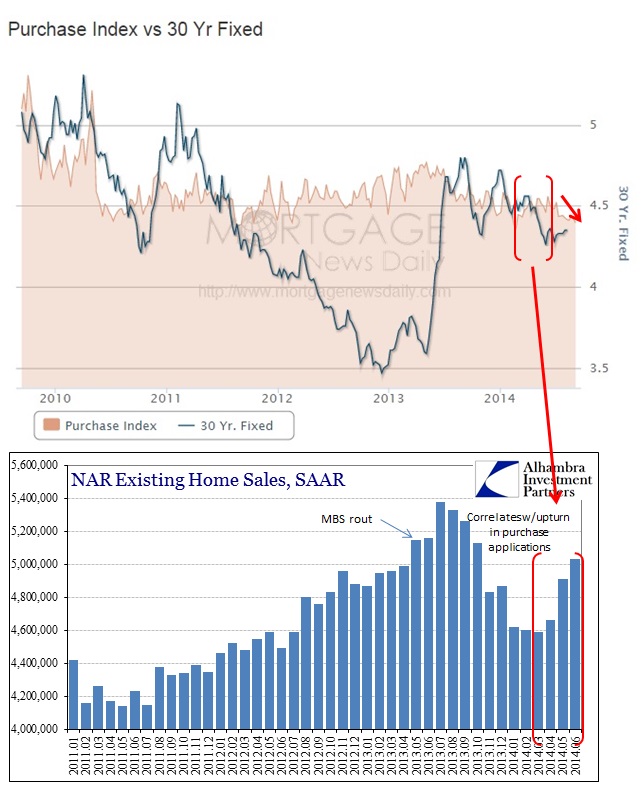

With the main flow of housing data a few weeks off, there is more discouraging news in the area of housing finance. Despite the retracement of interest rates, the 30-year conventional fixed in particular, since last year’s dramatic rout has done absolutely nothing toward re-establishing volumes consistent with the interim mini-bubble of 2011-12. With every week that passes under these constraints the more it looks like banks have fled the area not to return.

The Market Composite Index, a measure of mortgage loan application volume, decreased 7.2 percent on a seasonally adjusted basis from one week earlier, to the lowest level since December 2000. On an unadjusted basis, the Index decreased 17 percent compared with the previous week. The Refinance Index decreased 11 percent from the previous week, to the lowest level since November 2008. The seasonally adjusted Purchase Index decreased 3 percent from one week earlier, to the lowest level since February 2014.

With home construction having already entertained essentially a flattened trend since early 2013, this isn’t likely to provide any boost to what was counted on as a burgeoning economic “tailwind.” Instead, with purchasing activity dropping to what is really the floor reached at the worst part of the housing bust, the ability of the real estate sector to simply stay out of further erosion is seriously in doubt.

Beyond that in the housing market at large, the rebound in sales activity coincided with the rebound in purchase activity, modest as it amounted to on both ends, so the lagged effects of a further drop in mortgage finance for purchases will likely bend the existing sales trend bank lower once more. That has to be a very unwelcome development given the large rise in the number of homes for sale in the past year (as pleaded by the NAR itself). With prices already slowing back to the earliest parts of the mini-bubble, there is a real danger for negative numbers.

This is made all the more poignant given that effective mortgage rates have actually declined even recently.

The average contract interest rate for 30-year fixed-rate mortgages backed by the FHA decreased to 3.97 percent from 3.99 percent, with points increasing to 0.08 from 0.03 (including the origination fee) for 80 percent LTV loans. The effective rate decreased from last week.

Of course, what is uncounted in the above quotation is the production spread in the MBS “market” with the Fed no longer “enriching” the subsidy to the degree it was pre-taper threats. In the end, it doesn’t make much difference other than to project exactly how monetary interference both creates massive distortions and fails to work as intended. Clearly, the MBS spread subsidy “worked” in the sense it “pulled” banks into the mortgage market after they had fled the first time, but to what ultimate avail? That created a mini-bubble, or a distortion upon a distortion, that left housing finance just as sour as when this all began (where are the banks now?). And where house prices have accelerated, which was certainly a primary goal of all this, the distortions leave behind not a healthy advance but another questionable future of vulnerability and potential reversal.

Of course, the orthodox “explanation” will be written exactly as it has before, namely that monetary policy can only create the conditions for a sustainable advance, and that if it fails to materialize there must be a deficiency in the “market” (or economy, as it were). The Fed supposedly is limited to “pump priming” in that role, an essential element of monetary neutrality, but that doesn’t mean its distortions don’t come with very real costs. Some of those costs are easier to determine than others, such as when house prices decline and foreclosures surge “unexpectedly”, but the less tangible costs are no less important. There needs to be an account for when monetary intrusion of this nature changes the very character of these “markets”, including the means and methods by which they operate and bend their operations toward nothing but those policy impositions themselves.

In this instance, it is almost empirical fact that banks came back into the mortgage market chasing nothing but that QE3 subsidy of production coupons and price appreciation in MBS. The end of the subsidy and appreciation trend coincides with the end of bank participation? Taper wasn’t supposed to be tightening, but that is the nature of artificial intrusion shorn from its source.

Click here to sign up for our free weekly e-newsletter.

“Wealth preservation and accumulation through thoughtful investing.”

For information on Alhambra Investment Partners’ money management services and global portfolio approach to capital preservation, contact us at: jhudak@4kb.d43.myftpupload.com

Stay In Touch