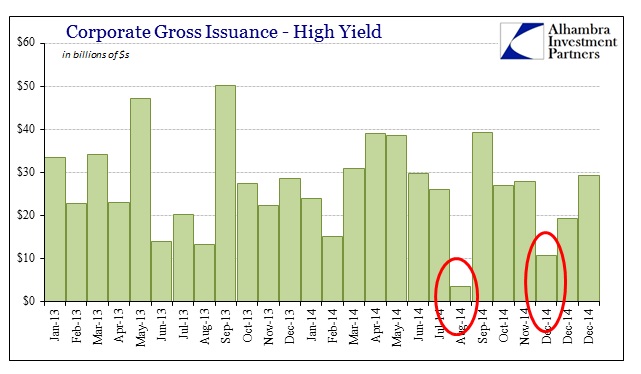

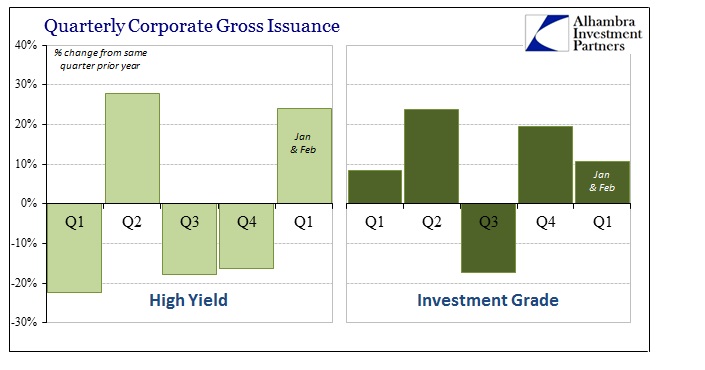

With liquidity running somewhat perilously noncommittal since June, you would think the riskiest parts of the credit market would be most affected. That is incorrect and once again stands out as to the bubbly nature of the current age. Aside from liquidity draining enthusiasm into and around October 15 and December 1, high yield debt has not only repriced itself back toward its prior levels but has also seen increasing exuberance in terms of volume.

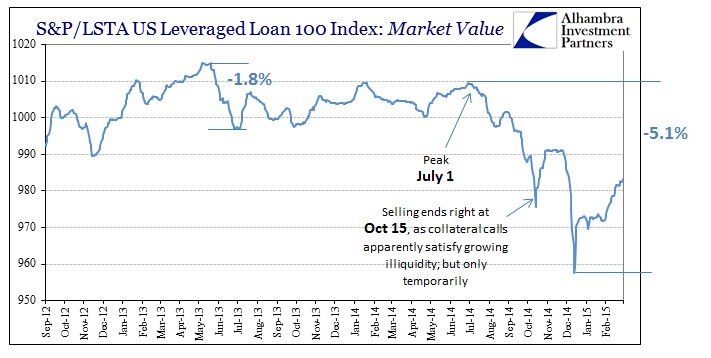

The effects of the October 15 liquidity event remain as a reminder about volatility, but the dent itself has not yet appeared permanent or even durable. Starting with leveraged loan prices, the recent “pause” in “dollar” disruption has meant not just sideways trading in this highest of risk tiers but an actual retracement to a significant degree.

As of early March, the index price of these leveraged loan tranches is about halfway back to the July peak and already a bit above the October 15 decline. That apparent fervor for the riskiest offerings is almost universal, as high yield bonds have been reborn so far in 2015.

Again, where liquidity had a direct impact on issuance in late 2014, likely through pricing, that has disappeared come 2015. As if to emphasize that further, Actavis PLC sold $21 billion in high yield bonds today at stunningly low yields. Almost the entire issue was rate BBB- junk, but it priced at just 175 bps above the benchmark UST. Not only was that incredibly low in historical context, it was actually quite a bit below even recent trading and indicating that there is still intense “demand” for any corporate paper of any size.

The Actavis sale is the latest sign of a booming market for new bond issues. Underscoring that point, Exxon Mobil Corp. announced plans to sell $7 billion in new bonds on Tuesday morning.

A 10-year Actavis bond was priced to yield 3.843%, or 1.75 percentage points more than benchmark U.S. Treasurys. That is on the lower end of guidance released earlier Tuesday and lower than the yields suggested on Monday.

So in that respect illiquidity is a distant memory even if it continues to be a problem elsewhere in the “dollar” world. That has led to this inversion again, seen closely in the 2013 taper selloff, where the riskiest assets perform the best, making the first and sharpest comeback.

Some will say this is all a sign of resiliency and robustness, but I think it more a tendency of rationalizations covering up the fundamental disparity evident here. Investors are just too eager to “risk up” with this low quality paper after each and every blip, serious as it was on October 15. That sounds an awful lot like the behavior of equity markets rather than credit.

In that respect, there is a linkage between these two “markets” that provides emphasis on that point.

Stock buybacks, which along with dividends eat up sums of money equal to almost all the Standard & Poor’s 500 Index’s earnings, vaulted to a record in February, with chief executive officers announcing $104.3 billion in planned repurchases. That’s the most since TrimTabs Investment Research began tracking the data in 1995 and almost twice the $55 billion bought a year earlier. [emphasis added]

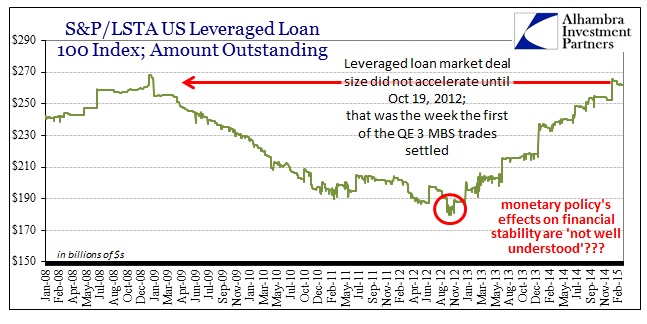

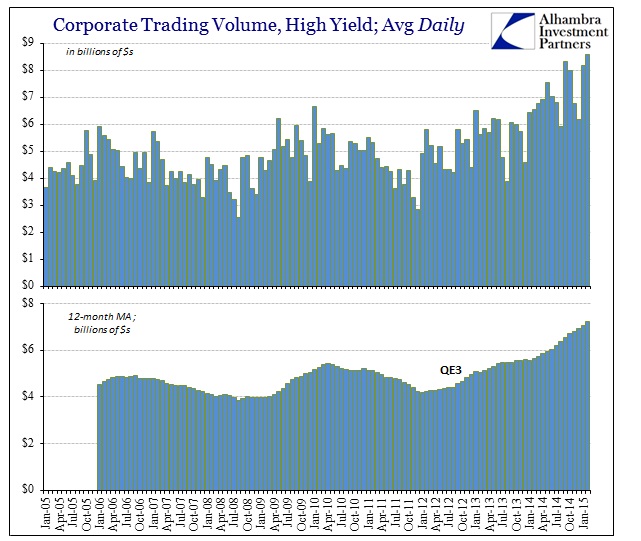

If there is a bubble, and even the FOMC continues to refer in that direction, it isn’t so much stocks vs. bonds as it is in the corporate space altogether. There is an unquenchable appetite for anything that has to do with US corporate paper and it is so increasingly divorced from the actual productive capacity of those corporations to service it – that is, beyond QE’s capacity to perpetually reduce debt servicing and increase rollover likelihood through the oppressed “reach for yield.” That is probably the most evident in how corporate bond trading volumes, especially junk, have simply exploded almost literally from the moment QE3 was implemented.

This is all yet another example of how QE has the opposite effect as intended. While there can be no doubt about especially QE3’s (and QE4) role in pushing the corporate bubble forward and upward, the tendency toward financialism through that process leads to lower productive capacity and spending – depressing actual economic formation. It has gone on so long and attained such heights as to become almost self-serving, which is why the corporate area so easily shrugs off what desperately plagues the rest of the planet.

“Companies that are earning a lot of money and generating cash are borrowing money at basically zero rates and buying back,” said Neil Grossman, the St. Petersburg, Florida-based chief investment officer at Tkng Capital Partners. “From an investor’s standpoint, you want the highest return on your dollar, period. If the highest return comes not from growing your business but buying your shares back, that’s fine.”

That may well be entirely true, but what happens in an economy where the “highest return” is nothing but corporate bubbles unto themselves? Nobody tends to “growing your business” anymore as the “froth” is the only objective “worth” pursuing, so that in the end the economy itself, the whole point of all this repression and asset inflation in the first place, remains stuck. Eventually that disparity becomes more than a small problem, which the “dollar” may already hint at.

Stay In Touch