In early July, the Bank of Japan may or may not have contemplated the mother of all “stimulus.” Rumors began to fly that the Japanese central bank was, in fact, seriously considering an actual monetary helicopter as a way to boost flagging confidence rightly suspicious of any more QQE (or NIRP). We won’t know for some time (when the meeting transcripts are released in the future) whether BoJ was truly contemplating the idea, but whether it was or not the rumors had the intended effect (which I believe raises the likelihood that the central bank was involved in them).

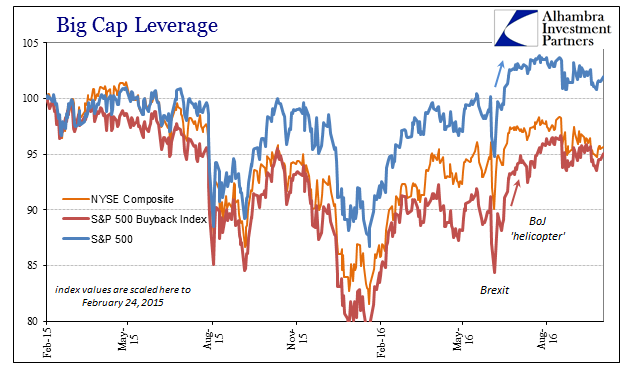

It wasn’t just Japan that felt the kick of possibly different “stimulus.” US stocks, for example, had hit a rough spot in the wake of the Brexit vote. It was short-lived bearishness, as once the potential “helicopter” was added into the mix of factors the S&P broke to a new record high, with other stock indices similarly intrigued. That euphoria was also short-lived, however, as since then the market seems far more unsure what all this might actually mean. In fact, since August and early September, stocks are overall slightly lower if still mostly sideways.

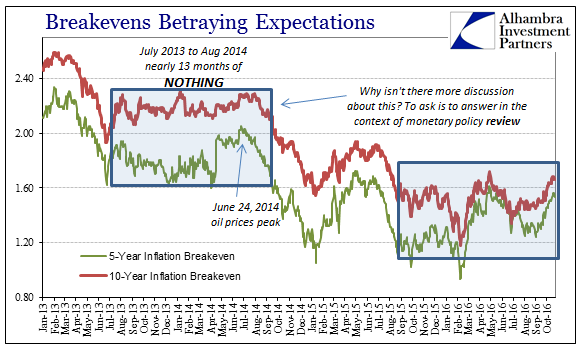

It isn’t just the stock market as other parts of other markets have joined in the glow of “helicopter” and like possibilities. Inflation expectations which had sunk near or to new lows suddenly reversed. After rising in September, breakevens are at the upper end of a range that has lasted since last summer when all this “global turmoil” first broke.

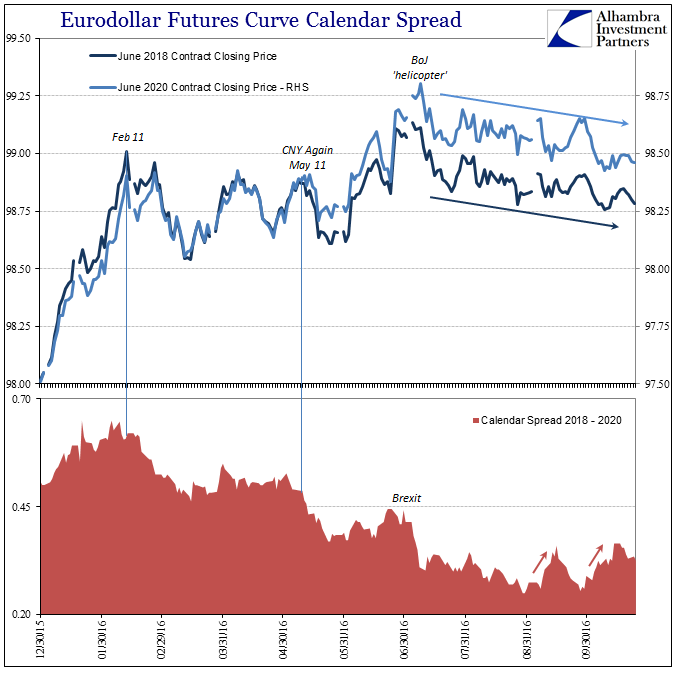

Of course, the bond market sold off and the yield curve steepened somewhat, too, though not in direct connection to the whispers of early July. Despite that, what I think is most convincing of these effects is the eurodollar curve. Eurodollar futures are mostly sideways but slightly higher (price) since the BoJ gossip. That was a clear break in the prior trend which had been the resumption or continuation of the prior upward track (bid). From the time CNY began to fall in its third strike of the ticking clock until the start of July, the eurodollar curve shriveled and flattened just as it had in all the worst parts of the past few years.

This more recent behavior is highly unusual as it shows such a narrow range. In September and again to start October, the curve shape itself decompressed perhaps as acknowledgement of inflation expectations, the yield curve, or simply less blatant pessimism.

There are, of course, a great number of other factors to consider, including that a great many market participants still find the FOMC’s federal funds rate relevant. But that so much traces back to July and the BoJ is for me highly significant in what I think is the central story of this year. The way last year ended and this one began was a direct slap in the face of QE and all the world’s central banks who trumpeted it for so long. For quite some months, markets lost faith, with good reason, and central bankers knew it.

What is clearly different this year is how they are more responsive to the challenge. This doesn’t mean they are or have been more effective, just that they are no longer so obstinate in their refusal to let go of QE in a more realistic assessment. Not only have we seen the BoJ back away from QQE and possibly consider other means (which was a valid interpretation as proved when in September they initiated yield curve “control” or “targeting”, whatever that is), the Jackson Hole gathering this year carried a wholly different tone, not quite repentance but perhaps as far as the world’s major central bankers may ever come toward regret.

Overall, I think, the message has been sent and received; monetary policymakers acknowledge that they were wrong and are now for the first time more receptive to softening about QE in favor of whatever else that might mean. For markets now more suspicious of policy than perhaps at any other point, it was a step toward restoring faith; not a full move in that direction, but almost as if these markets are at least willing to bet on an increased upside because there is the possibility now of something besides the usual.

Given where markets were heading to start July, the difference may be trivial in the end. Though stocks are up and the S&P hit a new high, as I wrote above it has been nothing like 2012 and the dual shot of Draghi’s promise and then QE3 (and 4). The UST market sold off, but not really all that much. And as much as inflation breakevens have risen, the 5-year/5-year forward inflation rate suggests that the UST market’s renewed “optimism” is but the difference between a hugely bad skew of scenarios to one now that is just really bad.

It does appear as if markets almost “want” to believe that central bankers have changed, but what does that actually mean? The fact that they admit their mistakes doesn’t immediately equate to sudden efficacy for whatever might come next. I think that is why any renewed optimism has been so subdued; markets are, as always, receptive to a possible answer beyond QE (or NIRP), but they are going to need much more than that. Central bankers are going to need to prove themselves this time for full effect, and that means legitimate ideas rather than just rumors. Ditching QE opens the door to something better, but without specifics not all that much.

This general skepticism is highly warranted and not just by past events. At the same time the eurodollar futures curve was in more agreement with stocks about ever so slightly more optimism, other markets further inside global money conditions took to the opposite interpretation focused more so on why central bankers actually need to do something else. In other words, there is a reason QE didn’t work and just figuring that out so late in the game doesn’t really change why it didn’t work. The “dollar” looms and the chances that the Fed, ECB, or BoJ (or PBOC) does something, anything that makes an actual difference is exceedingly slight.

By contrast, swap spreads fell more negative (10s, 30s) on Japan not about the “helicopter” rumors but later in July when BoJ instead essentially confirmed Japan’s great “dollar” problem. To stocks and surprisingly eurodollar futures, maybe that was a small positive sign about intellectual growth and acknowledgement; to the swap market, interest rate as well as currencies, it was confirmation that the “dollar” is actually just that bad and perhaps just that unfixable.

I think those are the two sides that have kept markets in more sideways action of highly uncertain terms. Now that central banks are open to more and different, it could accomplish more than just bloated rhetoric, but still a long shot. Against that is the “dollar” that has frustrated and overwhelmed more and different since August 2007. Even in global markets that really, really want to believe in the happy ending and magic of monetarism, it’s still no wonder the reaction has been so muted.

Stay In Touch