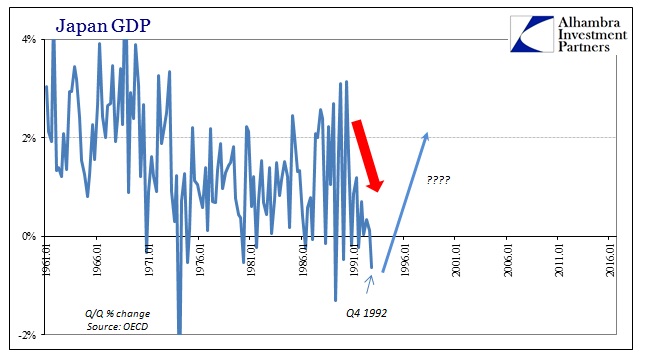

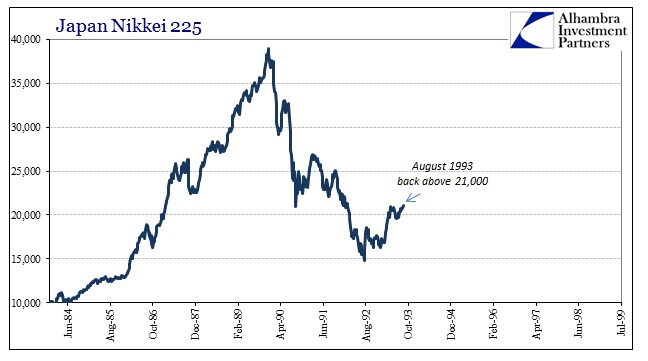

After being pummeled by a concurrent stock and real estate crash, Japanese officials by late 1992 felt that enough was enough. The Nikkei 225 stock index that was nearly 40,000 toward the end of 1989 had crashed to below 15,000 by August 1992. From that point, however, Japanese stocks had started rising again. Through the summer of 1992, things looked somewhat better, and the Nikkei seemed to reflect growing optimism that sufficient “stimulus” had been introduced that would lead all the way past any painful adjustments.

In Q4 1992, GDP was slightly negative (Q/Q) again, but as stocks that seemed more like a bottom for the overall economy than a further threat. Government officials reflected that view increasingly in outward fashion to a public quite eager for any possible good news. When in October that year the Japanese Finance Minister began to more confidently talk about recovery, it seemed in the mainstream entirely appropriate.

Japan’s economy is in a “difficult position” but could launch into a full- scale recovery early next year, Finance Minister Tsutomu Hata said Tuesday.

Speaking at the Foreign Correspondents’ Club of Japan, Mr. Hata, a leading member of the ruling Liberal Democratic Party’s huge Takeshita faction, was confident that inventory adjustments by Japanese companies in the first few months of 1993 will pave the way for a significant business rebound. The minister said he expects the government’s $88.4 billion pump-priming package to spark the economic takeoff, but added that local governments are economically healthy and are expected “to help too.”

At first, that did seem to be the case. Where GDP had been -0.6% to end 1992, it jumped up to +1.1% to start 1993. That was the highest growth rate in almost two years prior (sound familiar?), and only the second time since mid-1990 that GDP was more than 1%. Faith in “stimulus” being then what it still, somehow, seems today, assurance was in no short supply.

But it didn’t amount to anything good, unless you count false hope under that categorization. Very quickly Japanese officials and markets began to see that there was, actually, no economic improvement in 1993, and began to struggle as to what that might actually mean about the future.

Bank of Japan Gov. Yasushi Mieno acknowledged in a Wednesday [Nov. 11, 1993] speech that upbeat official forecasts of this spring have proved wrong. “There seem to be no signs supporting economic recovery in the latter half of fiscal 1993,” the central bank chief said.

In a report Tuesday, the Economic Planning Agency dropped optimistic language about an impending recovery that was contained in previous monthly reviews.

This is something that ten years on the Japanese would be severely criticized for. In several cases, studies, and policy settings, US officials and economists, in particular, chastised the Japanese for first being too optimistic and then giving up and admitting when that optimism proved wholly inappropriate. It was at that June 2003 FOMC meeting that I continue to emphasize where this discussion was especially poignant:

KOHN Another problem in Japan was that the authorities were overly optimistic about the economy. They kept saying things were getting better, but they didn’t. To me that underlines the importance of our public discussion of where we think the economy is going and what our policy intentions are.

The lesson to be drawn, apparently, was that you don’t get too excited as a policymaker and claim too much of your policy, but more so that when that policy doesn’t seem to work you also can’t just admit it. This is, of course, rational expectations theory where people’s expectations, in this case the Japanese, matter as much if not more than actual yen or dollars.

As ridiculous as that sounds, that is what moves modern monetary policy especially in the 21st century. It was the judgment of the FOMC, and really mainstream economics, that the failure of Japan in its “lost decade” of the 1990’s was as much mistakes about policies as the policies themselves. Very little consideration was given to more fundamental values (and I do mean values).

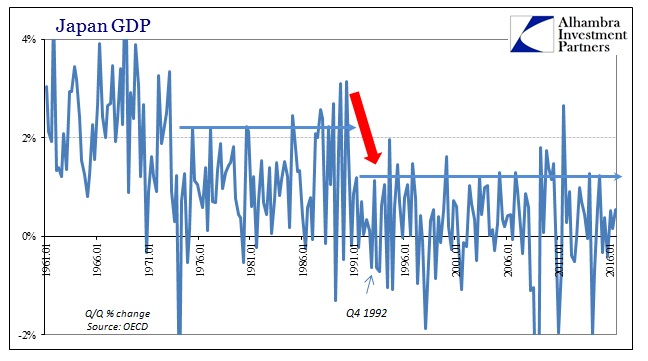

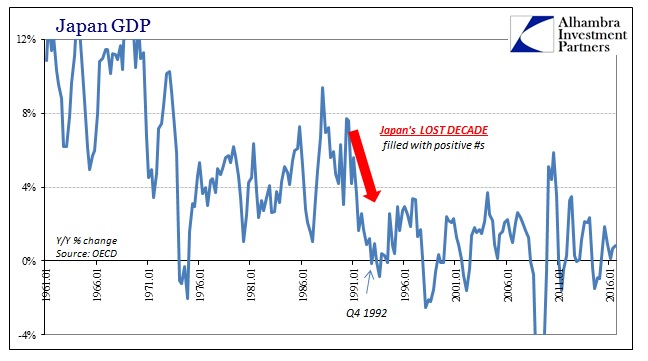

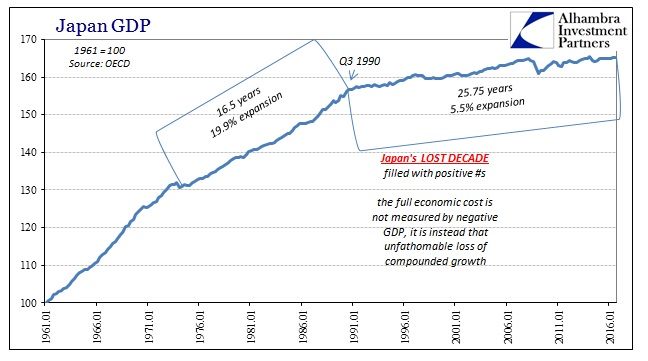

We have often heard quite well into the 2010’s about the Japanese’ “deflationary mindset” which, I believe, has the effect of creating mistaken impressions, particularly about Japan’s economy. The 1990’s were not one great crash spread out over ten years or so, they weren’t even all that much negative. Indeed, for most of Japan’s economic existence after 1990 there were plentiful positive numbers in all kinds of accounts and measurements, including GDP.

As you can plainly see on the chart immediately above, Japan’s Q/Q GDP was as volatile as it had been in the years before only it was downshifted closer to the zero level. The difference doesn’t seem like all that much, from an upper range of around 2.5% to one that was more like 1.6% to 1.75%. But the cost of that difference spread out over enough time is incalculable not just as a counterfactual but in what it does beyond these quantitative efforts.

Japan’s lost decade(s) was truly lost compounding from where growth would have been had the dislocation in 1990 been a true recession. A cyclical contraction is very easy to comprehend in every day terms, as we know quite well what that means for unemployment and lost business opportunities. But as painful as that often is, there is no way for us to conceive of the far worse fate of how the economy just stops growing as it had just a few years before. There is nothing in our personal experience by which we can benchmark and more easily process “missing” growth that doesn’t fit the recession/recovery mold.

When all the economic stats you see on TV or read about wherever there is mainstream analysis are negative, you expect recession and all those foul consequences. But when those same stats are almost always positive, just a little less perhaps than maybe you remember, with an occasional negative perhaps regularly too, your experience doesn’t prepare you for understanding what that means. As you can see above, recession, even a large one, isn’t actually the worst case. It is where the economy grows slowly over a long period of time so that the costs of compounding become unfathomable.

The economic statistics themselves begin to lose all meaning; as positive numbers, they say the economy is growing, yet most people (outside the prior non-Japanese economics profession) can tell that “something” is very wrong. It’s a vague sense of lost opportunity and maybe an occasional personal reference to how things do seem different in terms of vitality and movement or change. The lingering display of low positives that serve to obscure the real problem are the true enemy.

While GDP in the 1990’s in Japan was far more often positive if low, it was still highly uneven as presented by the occasional negative quarter or even a cluster of negatives that fit the “technical” recession definition. As the economy swung between positives and negatives, the positives began to be recast as hope simple because they weren’t negative. It was certainly the most nefarious aspect, where the slightest increase or acceleration which once would have registered as widespread concern is recalibrated down so that the pittance is applauded or even celebrated.

As bad as all that sounds, what makes it worse is that at its root is incompetence and ideology often blended together. It may astound you, but in that June 2003 FOMC meeting, the committee members actually identified where it all went wrong:

POOLE Japan made the same mistake at that time that we did in the early 1930s, when the Federal Reserve and many others thought that policy was becoming easier because interest rates were going down but when, in fact, the central bank was pulling liquidity out of the system. Certainly one important lesson from both the early ’30s in the United States and elsewhere and from the early ’90s in Japan is to pay some attention to the aggregates in these extreme circumstances.

To the modern central banker, money was the “aggregates” (M1, M2, etc.) and thus there was belief that any central bank in the future, say 2007, would be able to the same trap. Knowing that systemic liquidity (functional money supply) is always the root cause of not just the crash but also the instability that follows which drastically impedes economic efficiency such that there seems to be an unseen yet unmovable lid on economic growth (positive #s), the FOMC surely wouldn’t make the same mistake, would they?

GREENSPAN The presumption is that if you increase the supply of money indefinitely, the price level has to go up, no matter what, or we all should turn our economic degrees back in to the universities that gave them to us. But what we don’t know and what unfortunately we assume, I think more subconsciously than anything else, is whether the pattern of going from increasing supply to increasing price levels is a continuum. We tend to believe that there is, in calculus terms, no discontinuity in the structure. I submit we don’t know that that is true. Indeed, I’ve always been concerned about the fact that the Japanese are pumping in, pumping in, and pumping in money. They’re going to increase their monetary base inordinately. The price level is going to stop moving down, then it’s going to start up, and then it’s going to explode, and the discontinuity there is a very dangerous phenomenon. We know the size of their debt, the supply of their instruments, and what their monetary system is doing. There is no credible long-term possibility that a central bank can keep creating money, in many cases high-powered money, and the price level will continue to fall. That just is not credible. [emphasis added]

Unless it’s not money. Calling modern, virtual bank reserves “high-powered money” doesn’t make them so, it just further reveals the deficiency of monetary models that always have assumed they were, and still do even now. The Japanese mistake of the 1990’s was not that they admitted their inefficacy, it was that they didn’t know anything about functional money.

Thirteen years later, Japan is still gripped by its so-called “deflationary mindset” even as bank reserves there might be heading toward the quadrillions. In the United States, despite four QE’s that expanded the “high-powered money” of the assumed “monetary base” the lack of inflation isn’t quite Japanese in its deflation, but certainly far more disinflation than that which Alan Greenspan suggested would cause him and his fellow committee members to “turn our economic degrees back in to the universities that gave them to us.” And, most importantly of all, our economy, like the whole global economy now, celebrates the smallest of positive numbers because the costs of lost compounding are here, too, already beyond our imaginations.

Alan Greenspan in June 2003 essentially set up an infallible test. The results perfectly clear from all over the world through a quarter century of economic history, and there is no money in monetary policy; what has been proved as not credible is monetary theory, calling into doubt all those economic degrees that Alan Greenspan used for a joke to make his point. But the point he made shows that the joke is on us for allowing this to continue since all that it is left now are some positive numbers that get many people really excited just as in Japan heading into 1993 and the surefire fruits of “stimulus.” They will try to claim it is actual growth worth heralding even though it looks more and more like Japan’s lost decade the further we go. The world’s economy problem is not what policy Janet Yellen or Haruhiko Kuroda might carry out now, it is Janet Yellen and Haruhiko Kuroda.

Stay In Touch