In a world where everything is transitory, nothing is. The FOMC in its latest statement referred to that word yet again. As always, the context is weakness. But if such is always unexpected yet occurring, even if temporary, “transitory” doesn’t apply. Yet we go through the ritual each time anyway.

The last (March) statement read:

The Committee expects that with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace, labor market conditions will strengthen somewhat further, and inflation will stabilize around 2 percent over the medium term.

The current version now says:

The Committee views the slowing in growth during the first quarter as likely to be transitory and continues to expect that with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace, labor market conditions will strengthen somewhat further, and inflation will stabilize around 2 percent over the medium term. [emphasis added]

Try as they might to do otherwise, they had no choice but to address Q1 GDP. Not only was it fresh in everyone’s mind, poor timing for them, but it actually deviated substantially from the March statement. A rate of 0.7% is not moderate anything (it’s not really expansion).

It’s odd that the FOMC reacted this way because one year ago there was no mention of slowing or weakness, even though conditions last year were verging on outright recession. The relevant wording within the policy meeting statement from April 27, 2016, is identical to the March 2017 version except in reference to inflation. At that time, only the deviation of measured inflation rates was designated “transitory.”

If you go back one year further, to April 29, 2015, the statement reverts back to “transitory” weakness, though in that case the word itself was again applied only to energy prices, leaving economic growth as merely “slowed”, leaving the remainder of the passage as its usual, recognizable platitude.

Although growth in output and employment slowed during the first quarter, the Committee continues to expect that, with appropriate policy accommodation, economic activity will expand at a moderate pace, with labor market indicators continuing to move toward levels the Committee judges consistent with its dual mandate. [emphasis]

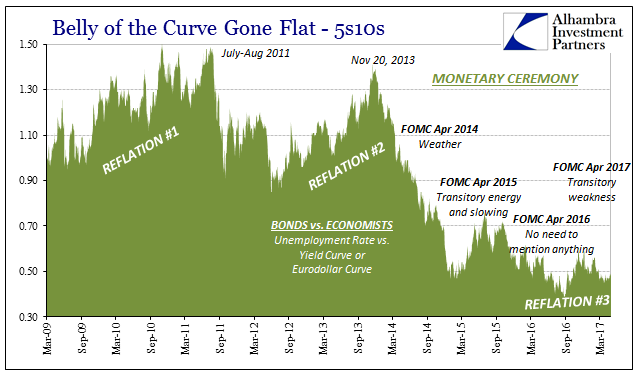

One year before that, the last day in April 2014, it was frozen temperatures. “Information received since the Federal Open Market Committee met in March indicates that growth in economic activity has picked up recently, after having slowed sharply during the winter in part because of adverse weather conditions.” For four years in a row, ever since the economy has been judged officially with risks finally balanced, there is always “will expand at a moderate pace” actually balanced with reasons why it didn’t. Or, in the case of early 2016, no mention at all of what was perfectly obvious.

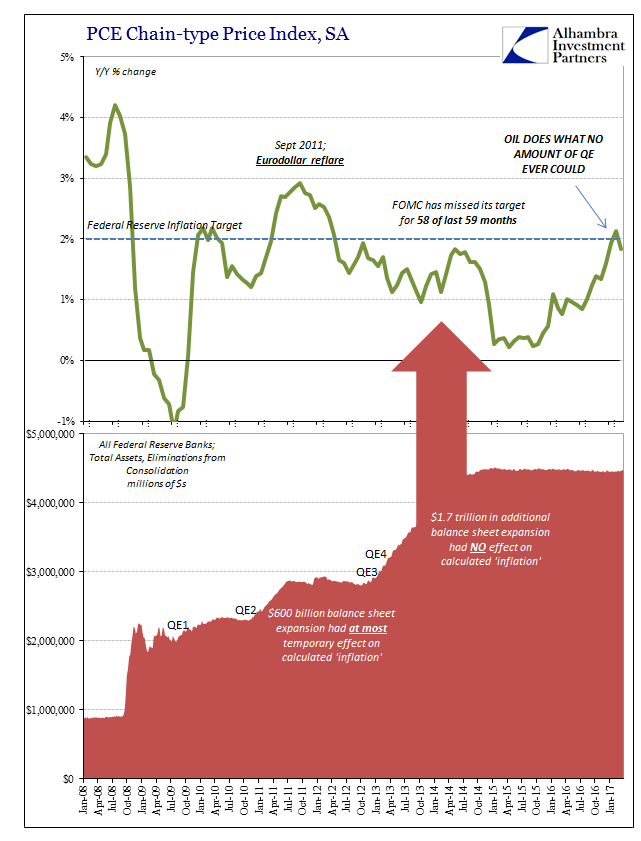

How can it be “transitory” then, when if year after year of what should be balanced risks there are only those to the downside? Even the statement on inflation, and the evolution of the official position on inflation, betrays these definitions. The FOMC says that “transitory” energy price differences will give way and that in the “medium term” inflation will stabilize around 2%. Given the history of the PCE Deflator as well as that wording we can only conclude that “medium term” no longer applies to something like a five-year period.

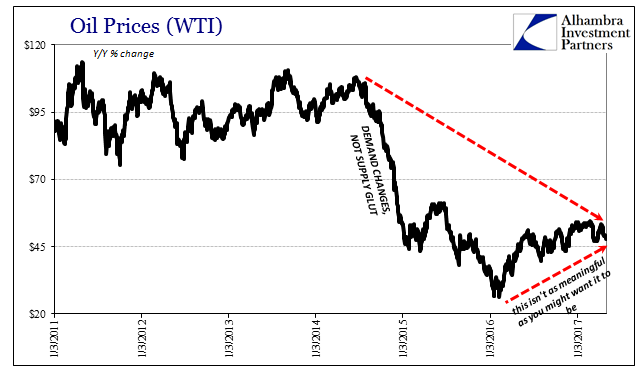

One out of 59 months does not indicate “stabilize” at all, especially when ironically it was oil prices, still not “transitorily” weak, that achieved what no amount of monetary policy could. It is overlooked in the year-over-year comparisons, but WTI remains less than half of what it was in 2014 when the weather was so bad. It immediately proposes what constant if temporary weakness might actually mean.

That is, almost nothing in the FOMC statements over the past four years is or has come true. It is a bunch of words that excite people in the media but for practical purposes intends solely to mislead about an economy that “should be”, but in reality would have been long before now if it was going to happen. Weakness year after year cannot be transitory even if the individual occurrences of it are.

This uneven economy is everything that defines the depression, for it is always one step forward, one or sometimes, as unmentioned in 2016, two steps back. Moderate expansion can only apply to a situation where there is at the very least expansion, a condition that might be technically true but only if you ignore that massive contraction cleaving all global economic history by remaining somehow unanswered still after almost ten years.

The good news for all of this is that the FOMC has been reduced largely to ceremony. For good and relevant reference, when the English Parliament is opened each year, the Queen arrives to great pomp and audience, carrying with her both a millennium of tradition as well as the legal sovereign of that nation. After leading her Royal procession through Royal Gallery and into the House of Lords, she sends her official representative, the Gentleman Usher of the Black Rod, to fetch the MP’s from the House of Commons straight in line from the Lord’s Chamber down the axis of Westminster.

Arriving at the door of Commons, it is slammed in his face, forcing the Black Rod to ceremonially pound, very heavily, three times with his rod square on the door in order for that Members might rudely follow him to the official Sovereign’s speech rightfully opening the session. Though the Queen still rules, the House of Commons is law.

These FOMC statements are in many ways quite like that; the Fed continues to act as if it portrays any useful economic meaning when long ago, almost six years, to be exact, the bond and funding markets slammed the door of real power on it. They may from time to time appear interested in the rambling ruminations of the perpetually confused, but for all that really matters these things are whittled down to mere televised ceremony. It’s a big deal for the financial channels and even for filling media page views, but eurodollar futures truly designate what moves the Earth now. And it isn’t transitory.

Stay In Touch