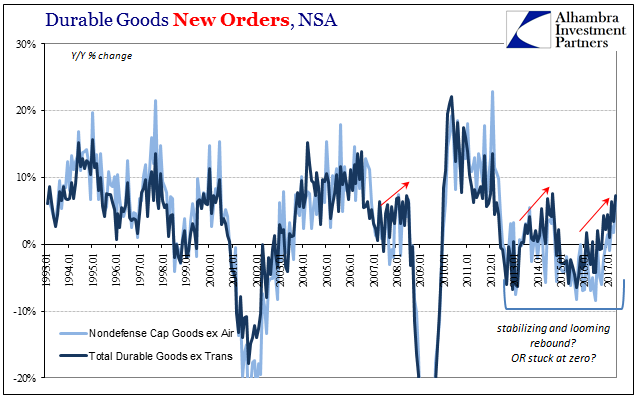

The status of durable goods in May 2017 appears to be up for debate. Once more there is major disagreement between the seasonally-adjusted figures and those unadjusted. In the estimation of the latter, May was a relatively good month for US manufacturing. Orders were up 7.3% year-over-year, the highest growth rate in nearly three years. It continues the track of improvement that started late last fall.

Seasonally-adjusted, however, new orders for durable goods were down 1.1% month-over-month, the second consecutive monthly decline. That possibly indicates whatever improvement may have been occurring has stalled out or at the very least paused.

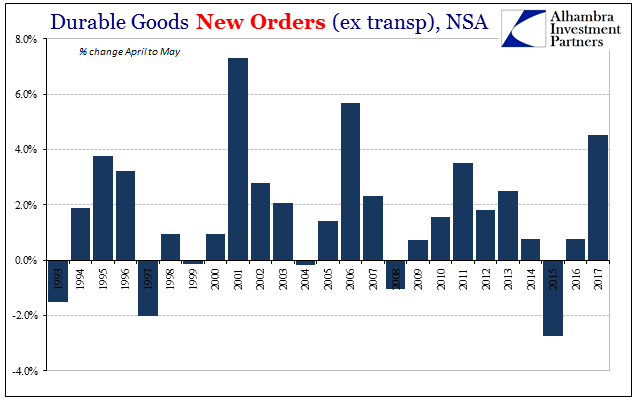

Exactly why the seasonal adjustments were so unhappy with the May data is unclear. Unadjusted, April to May is typically a swing month. During what are clearly growth periods we would expect orders (as well as shipments) to rise from the one month into the next; the opposite during more distressed circumstances such as those in 2015 and 2016.

In 2017, the unadjusted change April to May is one of the larger in the series. Of the last few years, it is more so. On the surface, without knowing the full reasons behind the ARIMA X- formulas, May 2017 should have been a positive result month-over-month. The calendar location of Memorial Day could not have made much if any difference.

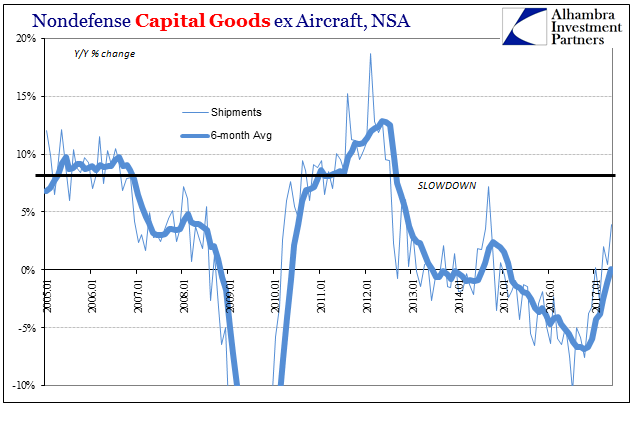

It might be that for reasons unknown the seasonally-adjusted estimates are finally seeing their way to the real underlying economic problem. Though orders and shipments are growing again, they are doing so from a low base (early 2016), at a rate so far more like 2014 than 2011, and from month to month unevenly. Durable goods have fallen into a distinct pattern of being good one month (unadjusted year-over-year) only to disappoint the very next, and so on.

It does seem to be the message received by even the mainstream media when confronted with consistently less than robust results in either series. At last month’s durable goods report (the one in May for April 2017), the New York Times lamented:

The big economic bounce that some experts have confidently predicted for later in the year may turn out to be only a small bump.

It is not that the economy is weakening, or that a recession is in the offing. Rather it appears as if the pace of growth in 2017 will not be much faster than it was last year, or the year before that.

However you view durable goods, and not only durable goods, that appears to be the correct interpretation once more unlike “expert” commentary. The economy is moving forward again after taking a few years off, but not so much forward that it means what everyone might want it to.

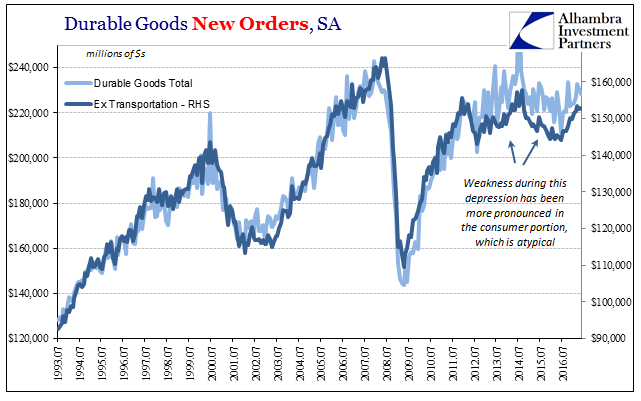

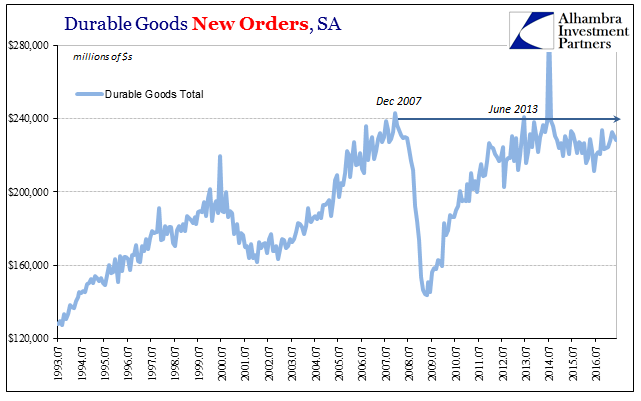

Total durable goods orders, including aircraft and transportation equipment, have been stuck at less than 2007 levels for going into a fifth year (and also having been revised lower at the May 2017 benchmark).

By any reasonable definition, it indicates serious economic problems with which uneven growth however presented would be consistent. Thus, we are left to consider the state of manufacturing in May 2017 as either good or bad, but in either case it was almost certainly not nearly good enough.

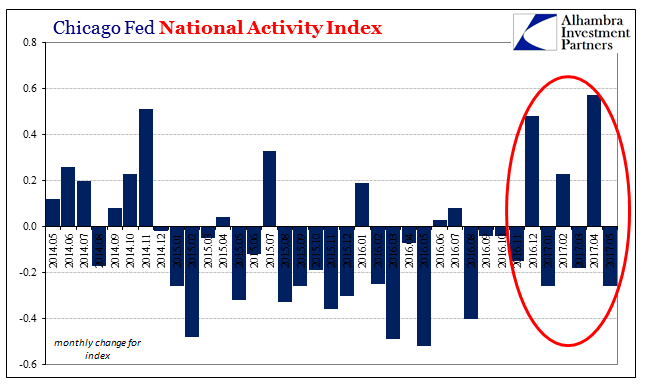

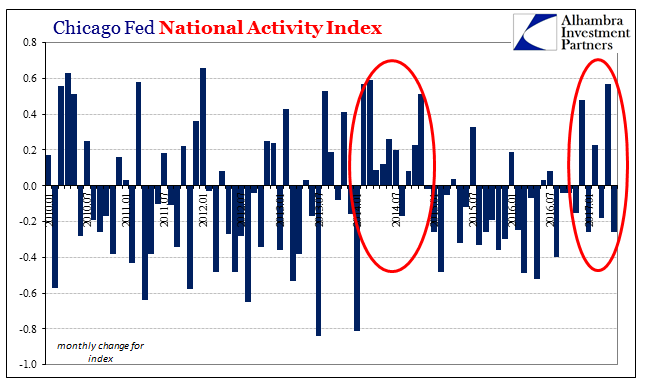

Other broad economic measures have included this same irregular economic advance. The Chicago Fed National Activity Index, for example, has like unadjusted durable goods orders and shipments alternated monthly between positives and negatives.

Altogether, the bad months don’t cancel out the good ones, but they do pull them back enough so that on net there really isn’t left much of an improvement. In the case of the NAI, it is a much weaker result than when compared to 2014.

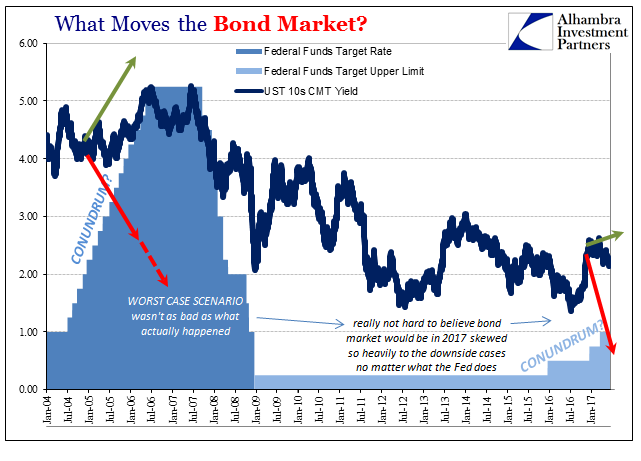

It’s all yet more evidence that the Fed is acting not on current data or even expectations for future growth, but for entirely different reasons – there is nothing left for monetary policy to accomplish. The economy is what it is, and therefore maintaining a low interest rate won’t change the situation. The growing sense that the economy’s situation hasn’t really changed even compared to last year and the year before can only underscore that policy rationale.

It’s all yet more evidence that the Fed is acting not on current data or even expectations for future growth, but for entirely different reasons – there is nothing left for monetary policy to accomplish. The economy is what it is, and therefore maintaining a low interest rate won’t change the situation. The growing sense that the economy’s situation hasn’t really changed even compared to last year and the year before can only underscore that policy rationale.

It’s a very different set of circumstance than what “reflation” was supposed to represent. There just isn’t ever going to be a recovery, or at least not until people start asking the right questions (why was there a 2008 in the first place?) and demanding proper answers from the right people. Until then, these problematic and uneven months are the best of times.

Stay In Touch