Correctly interpreting the bond market is more than just how and when to invest your money in UST’s. Not that it isn’t useful in such a money management capacity, but interest rates starting at the risk-free tell us a lot about what is wholly unseen. There is simply no way to directly observe inside an economy what is taking place at all levels and in all transactions. We try to estimate as best we can in the aggregate, but the real economy works itself out far over the horizon.

The closest we might get to a more accurate description is provided by market prices. Though incomplete by themselves, they are derived of the same dispersed knowledge of actual conditions. The bond market by its nature and its history is one of the best sources of information.

The specific issue is, as always, opportunity. An economy’s monetary circumstances will always be described first in those terms. As Keynes proposed for consumers, it is opportunity that dictates liquidity preferences; without it, economic and even financial agents will hoard money, near-money substitutes, as well as highly liquid instruments like UST’s.

This relationship between interest rates and the hidden economic money condition was first stated by Knut Wicksell in his theorizing about a natural interest rate.

In good times, when trade is brisk, the rate of profit is high, and, what is of great consequence, is generally expected to remain high; in periods of depression it is low, and expected to remain low. The rate of interest on money follows, no doubt, the same course.

Milton Friedman much later stated it plainly as the interest rate fallacy. You can have all the central bank statistics you want claiming that money supply is “loose”, but if interest rates behave as Wicksell and Friedman ably described then in actuality the unobservable monetary condition in the real economy must be contrary to those numbers.

In the 21st century this may seem instead a settled affair. The Federal Reserve dictates dollars, full stop. In truth, however, the Fed does nothing of the kind. The textbook all say that open market operations are the key to money stock, but it just hasn’t been the case if a very, very long time. This is a condition which past officials have from time to time fully admitted. Most people never much paid attention to what were and are treated as at most philosophical digressions.

Alan Greenspan, for example, in a speech given at Stanford University in 1997 said:

Nonetheless, we recognize that inflation is fundamentally a monetary phenomenon, and ultimately determined by the growth of the stock of money, not by nominal or real interest rates. In current circumstances, however, determining which financial data should be aggregated to provide an appropriate empirical proxy for the money stock that tracks income and spending represents a severe challenge for monetary analysts.

Inflation is at its core another proxy for opportunity, more of a lagging indication of its presence in the real economy and thus the successful dehoarding of money. But in Greenspan’s view, since no one in 1997 had any real idea what money was, the only way to truly measure the monetary condition inside the real economy was through things like inflation – and bonds. His Fed did so they thought correctly up until the 2000’s using a discretionary (not monetary) interest rate policy that was never actually fully revealed.

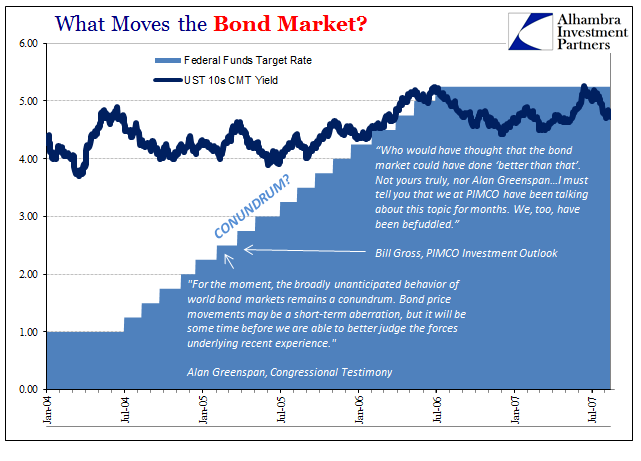

This largely why in the last fifteen years in particular bond markets have remained largely at odds with mainstream economics and orthodox economists. Through mostly the legend of Greenspan rather than actual monetary understanding, economists came to believe the Fed at the expense of the treasury market. If the maestro was tightening in the mid-2000’s, who was a treasury investor to say otherwise?

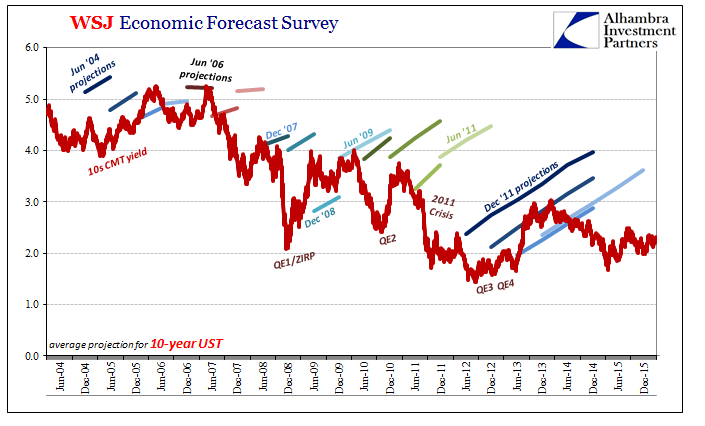

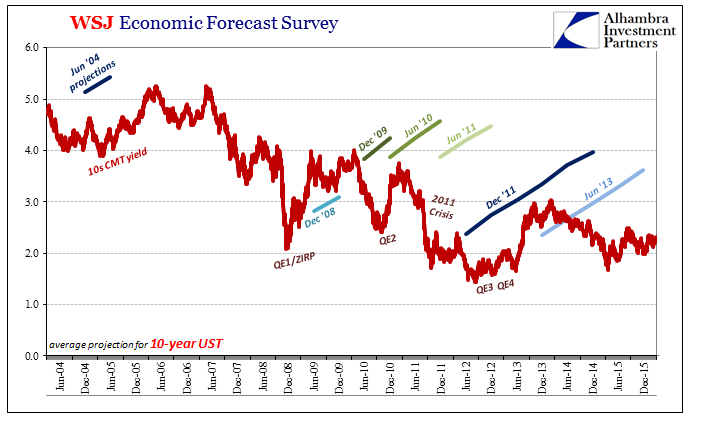

What we observe, then, of the “conundrum” as well as the inability of economists to correctly identify economic and financial risks is really a bias of policy, not money. We can see this directly in the wider suite of forecasting history produced by the Wall Street Journal I alluded to earlier today. In almost every case, shown above, economists forecast rates moving upward based on perceptions of money through the lens of the Federal Reserve; even when directly contradicted by the bond market.

This policy bias is especially clear when new policy measures are undertaken, starting first with “rate hikes” in June 2004.

The most egregious misses in the collective mainstream forecasts are all clustered around these policy initiations (the exception for the December 2008 forecasts isn’t clear whether those projections were made before or after QE1/ZIRP; my guess is before, thus the undershoot of the actual 10-year rate). In other words, economists always assume that the Fed dictates monetary conditions, thus inflation as well as opportunity, when instead it has been shown time and again that it just doesn’t work that way. The hidden monetary circumstances of the US and global economy is displayed by bond yields, a fact that should have been considered the final authority rather than just dismissed in favor of a settled view of Greenspan’s legacy that even he wasn’t ever really comfortable with.

If the Fed and the rest of the central banks had little idea what was taking place with money demand, they had no idea what was going on for money supply. In fact, they really didn’t want to know, preferring instead to focus on what Ben Bernanke would later specify as the “aggregates”; things like income, GDP, and most especially inflation rates. If those aggregates were well-behaved, particularly inflation, then, once again, it was simply assumed monetary policy was the reason.

You can already see the conundrum for what it really was. If inflation or whatever other monetary characteristic was not well-behaved, where would the Fed even begin? That has been the history of the last ten years in particular, where once things started to go wrong none of the central banks had a real idea what it was that was wrong, let alone any further idea what to do about it.

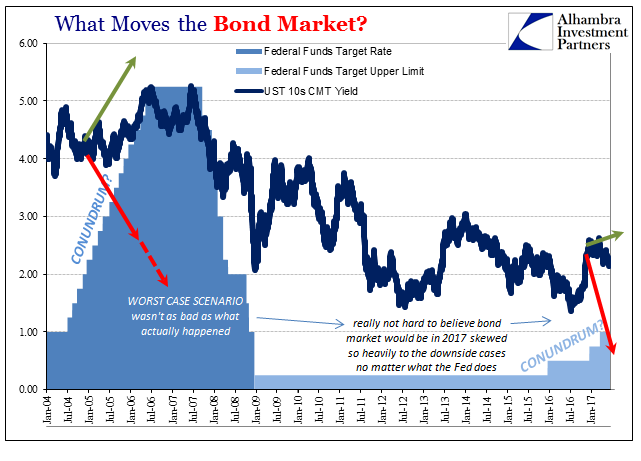

Instead, they ended up repeating not just QE’s but also predictably their lack of results – the state of the actual money stock included. Despite four of them in the US and in dollars, UST interest rates kept suggesting (if not declaring outright) economic opportunity low and stubbornly insufficient, meaning that no matter how many trillions in bank reserves were created by the Fed’s balance sheet expansion they did not add to the hidden, functional economic money stock globally.

The idea that interest rates have nowhere to go but up has been thoroughly tested for longer than the already-lengthy crisis and post-crisis periods. It has as its basis the exact wrong idea about true economic circumstances, derived as a bias from other bias.

In other words, the bond market is one of the few legitimate windows into hidden monetary conditions, and what it has said about the 21st century isn’t what economists and policymakers want to hear. The conundrum and its current revival are just that simple.

Stay In Touch