Why don’t economists understand bonds? The long answer involves several detours into parts of Economics that have nothing to do with interest rates or even money. More so these places are dominated by discussions of stochastic calculus and partial differential equations. Thus, the short answer is:

Affine models of the term structure of interest rates are a popular tool for the analysis of bond pricing. The models typically start with three assumptions: (1) the pricing kernel is exponentially affine in the shocks that drive the economy, (2) prices of risk are affine in the state variables, and (3) innovations to state variables and log yield observation errors are conditionally Gaussian.

When this becomes your operative view of the bond market, you are already in trouble. By this conditional approach, you have no choice but to break down bond yields into measurable variables, starting with the subjective assumptions that you are able and wise to do so. As you can already tell by the language in the quoted passage above, it’s not very easy or straightforward to do.

Economists will argue that decades of research has gone into developing especially affine models and they might even generally agree that they work well for their limited task (of making more models). Anyone with common sense will easily counter with “conundrum” and everything Janet Yellen claims is “transitory.”

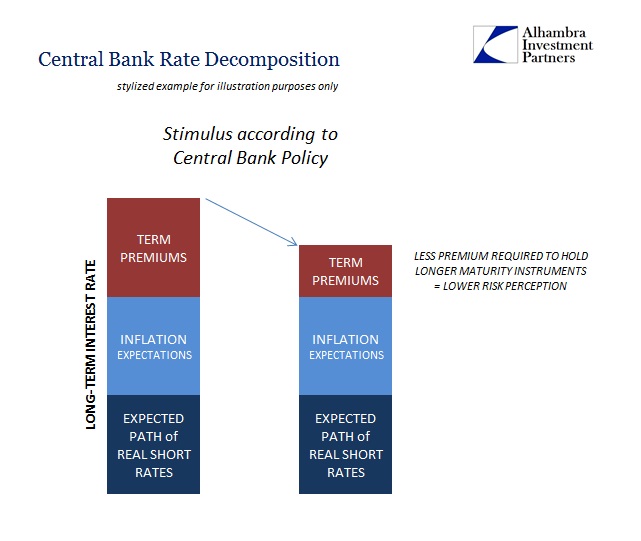

This questionable statistical approach starts by breaking down interest rates into two parts (and then the first part into two other parts). There is the expected path of short-term interest rates, which is split into expected future money rates plus inflation expectations, leaving off as a remainder these things economists call “term premiums.”

A term premium is in theory the extra yield a bond investor demands for holding a relatively longer dated security of the same issuer and type. The yield curve which is supposed to display the upward slope of these time expectations is actually both parts (or all three) put together. Thus, it is possible, theoretically, where the yield curve might be upward sloping but that term premiums are also negative at the same time.

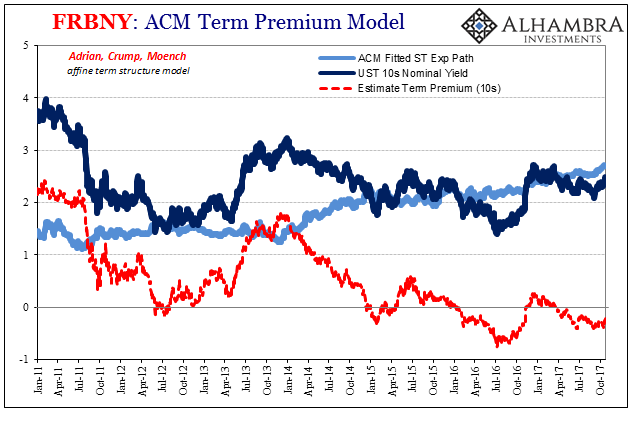

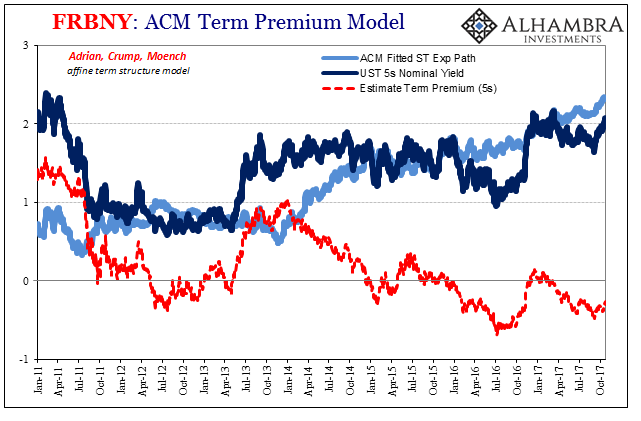

It is not, of course, an expected situation but several mainstream models, including one FRBNY uses referencing the paper quoted at the outset, suggest term premiums have been negative in the US Treasury market for several years now. Accordingly, economists who don’t get bonds are once again stumped.

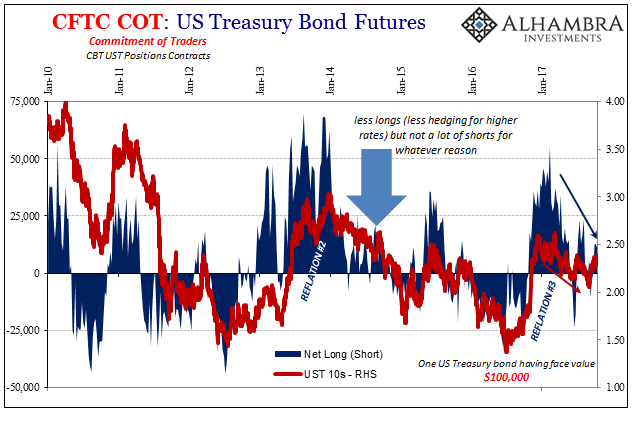

As usual, it takes no knowledge of or familiarity with differential equations to see what’s wrong. The Fed’s models simply assume that the path of short-term interest rates is rising and has been especially since the start of 2014 once the tapering of QE was enacted. That means a great deal to economists working at the Fed, and almost nothing to bond market investors trading 10s, 7s, 30s, or whatever else.

Like a low or even negative R*, negative term premiums aren’t what economists think. They are instead a nonsense result trying, desperately, to tell these statisticians that their whole frame of reference is wrong. Economists believe their models even when those very models spit out gibberish. Thus, they are drawn deeper down the rabbit hole trying to figure why an investor is taking a discounted term premium on a UST 10s when nothing of the sort is really happening.

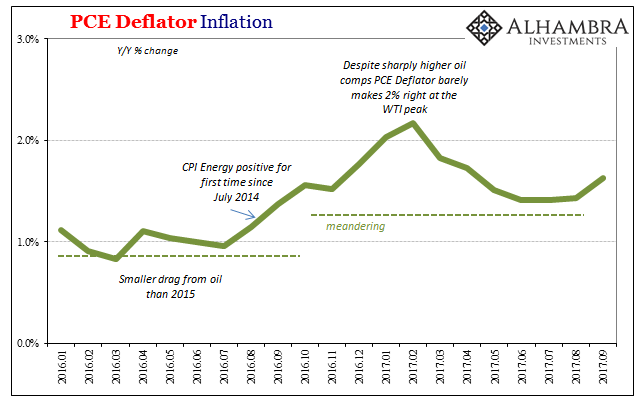

Unlike Economics, markets aren’t bound to ideology, which in practice hardens these assumptions into philosophical anchors that twist and pervert what would otherwise be straightforward meaning. Today’s report on inflation in the form of the PCE Deflator is yet another reminder of this fact.

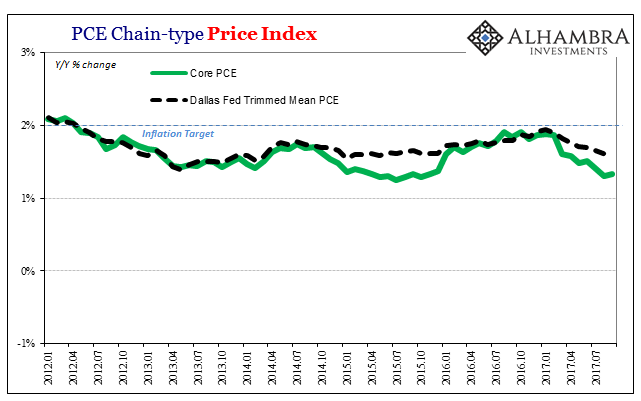

For the month of September 2017, this version of consumer price inflation rose 1.63% year-over-year, the 63rd month out of the last 65 that hasn’t been at or above 2%. Rather, inflation in what cannot be classified as transitory tends to remain low and underneath the explicit monetary policy target defining a sustained 2% PCE Deflator as “price stability.”

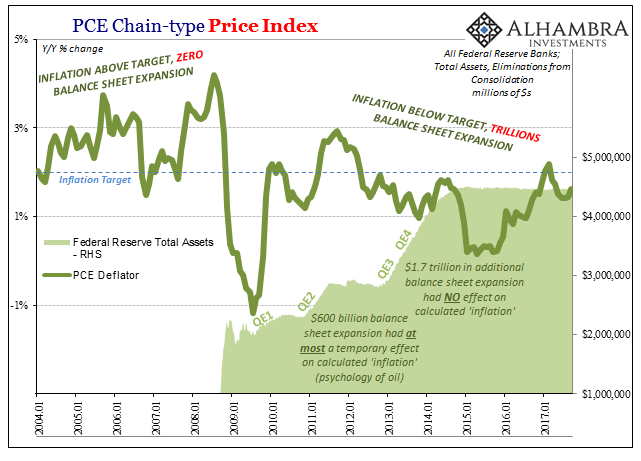

This is the opposite case from before 2008 when both the PCE Deflator as well as the CPI tended to be significantly above 2% consistently. More calculated inflation before when the Fed did little or nothing, and less once the Fed started to do a whole lot. The difference then and now is not just economy but also the monetary policy response to it; which leaves the monetary situation upside down. The more the Fed has done (LSAP’s, or large scale asset purchases otherwise known as quantitative easing), the less inflation responds positively.

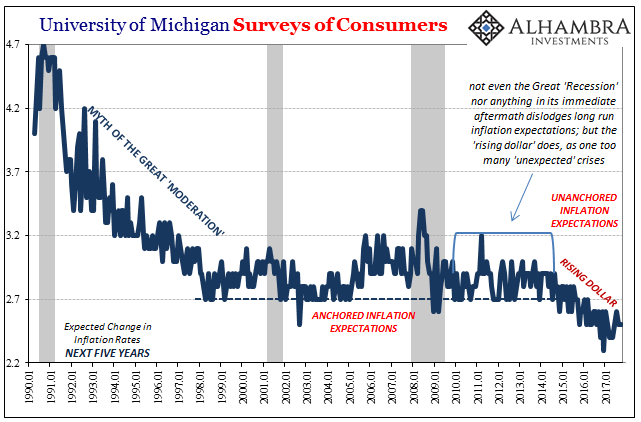

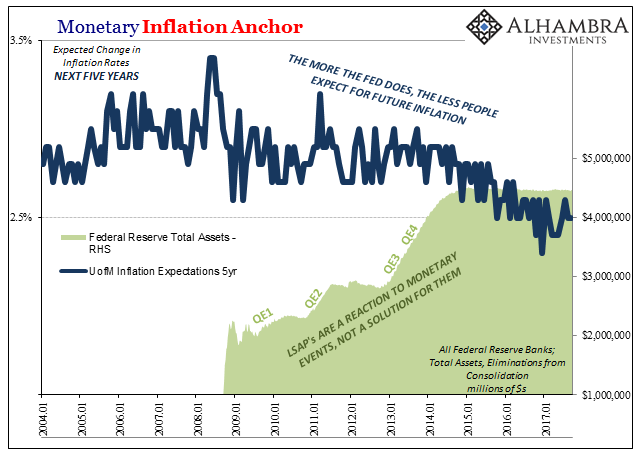

It’s difficult not to notice this difference, and notice people have in everything from TIPS to consumer surveys that show a remarkable difference in the path of expected inflation. What the Fed actually did during those years of LSAP’s doesn’t any longer matter, as the results of what the Fed did are not inflationary in the least. You can’t “print money” and have inflation behave this way, especially compared to how it behaved when you didn’t “print money.”

What we are left to conclude, to only conclude, is that LSAP’s are nothing more than poorly designed, unsuitable reactions to grave monetary events. They tell us what the Fed did in response to what already occurred not what the economy will do left unshielded to be damaged by the very same things. Therefore, Economists extrapolating short-term interest rates in their aftermath are attaching meaning to those regressions that isn’t appropriate.

That means they expect the bond market to behave one way according to their assumptions when in fact it is behaving the opposite way according to (monetary) reality. The “interest rates have nowhere to go but up” people are making the dangerous assumption that economists know what they are doing (generally) especially when it comes to bonds, inflation, and money (oh boy).

By not being wedded to that orthodox ideology, in no small part by not being dazzled and distracted by the mathematics, we can instead see common sense clearly play out where to Economists there is some great puzzle or enigma. The only riddle is why Economists continue to produce nonsense results and try to fit the world into them rather than being faithful to a truly scientific endeavor which would appreciate and gracefully welcome such falsification for an almost Ptolemaic worldview and mode of understanding. It can’t be easy for Economists, but still they should pay close attention when their own math tries to tell them that they really don’t know what they are doing.

Stay In Touch