The Bank of Japan is run by clowns. All of their major moves have blown up in their faces. The NIRP fiasco of January 2016 was one of the most stupendous moments of technical ineptitude ever displayed by a central bank; and that’s saying something, being able to choose from such a long and prominent list of monetary policy errors.

Having written that, I’d still take the BoJ over the Federal Reserve, Bank of England, or Bank of Canada. The ECB isn’t yet in the same class as those but it is making noises about moving in their direction. While BoJ is a destructive joke, these latter are thoroughly and insidiously corrupt. There is at least some honesty in Japanese policy that is missing from the rest in the West.

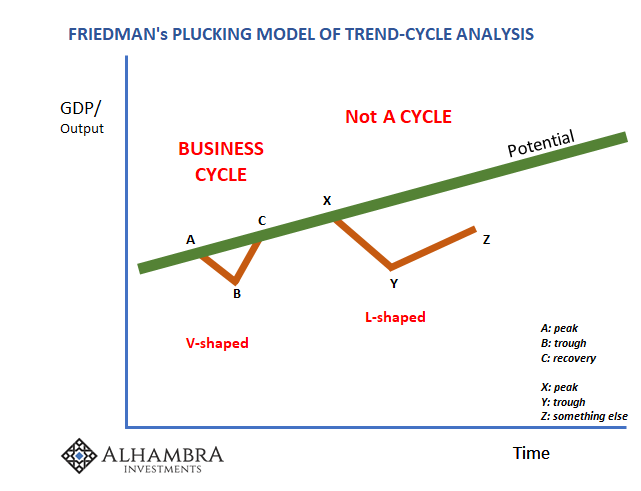

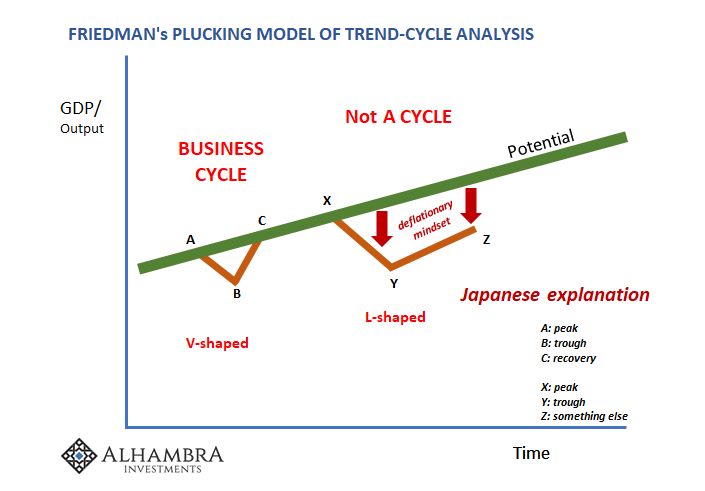

Let’s start with the basic problem confronting the whole global economy – without yet getting into why the whole global economy is following the same pattern. Central banks are prepared, or at least they think they are, for a business cycle. A regular recession is a temporary deviation from trend, also called potential. It used to be that a central bank’s job was to try not to screw up so much that you make B worse, longer and deeper.

Nowadays, the task has been redefined so that any central bank believes it must intervene so as to push B up and left; shallower and shorter. There was even a time during the Great “Moderation” when Economists actually thought they had found the Holy Grail of monetary policy – eliminating B altogether. Such folly and hubris is relevant to the right side.

After a decade of seemingly doing the same things as the BoJ had been doing for a decade before they started, US and English central bankers have somewhat changed their tune. They might have been into QE and ZIRP like BoJ, but the reasons why aren’t exactly equal.

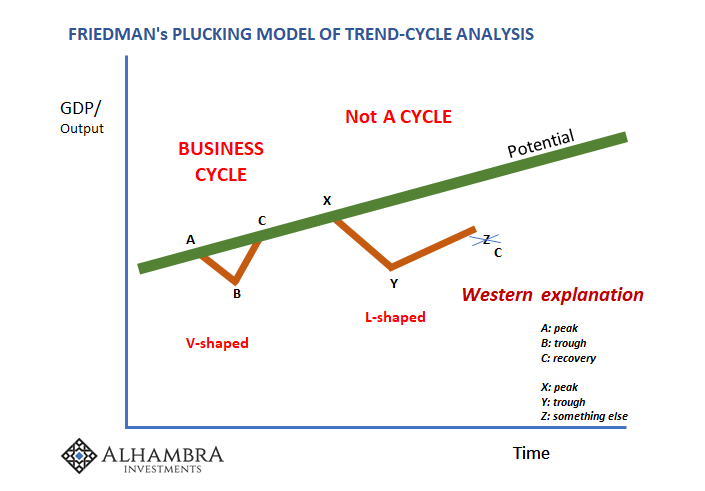

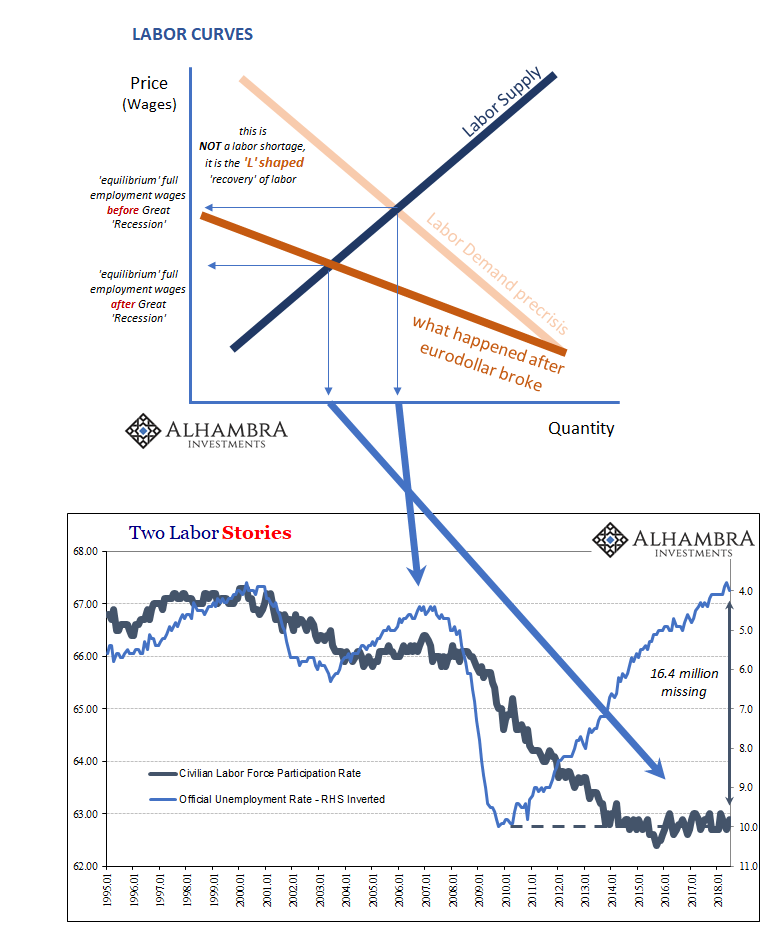

As 2015 turned the wrong way again, the idea of secular stagnation gained strong currency (pun intended) in Western policy circles. The lack of recovery following the Great “Recession” wasn’t a lack of recovery at all. The “L” shape of it remained, obviously, but it came to be viewed as a completed cycle if still a very weird one.

Central banks hadn’t failed the economy, the economy had failed them. QE accomplished what it was supposed to, sort of. The US economy in particular has resumed its trend at C, they say, therefore recovery.

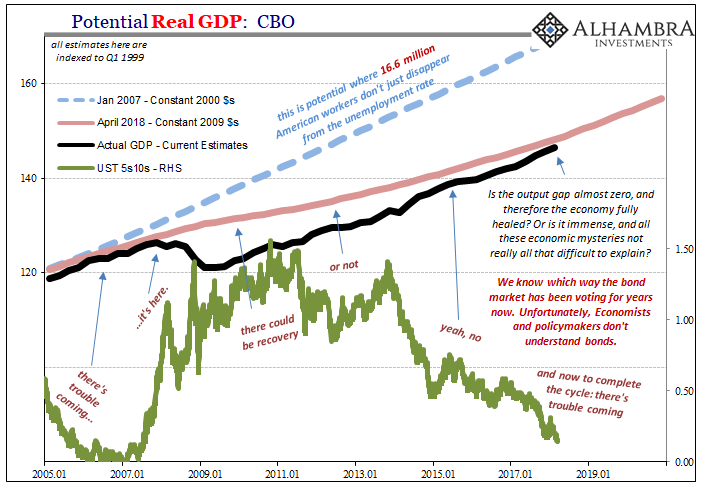

If you reach C, or just get close enough, you remove any further accommodations, wind down all QE’s, and begin raising rates while talking about “above potential” growth that isn’t at all the same potential as it used to be. Blame drug addicts and retirees as needed for the change in potential should anyone bother asking.

This is pure corruption.

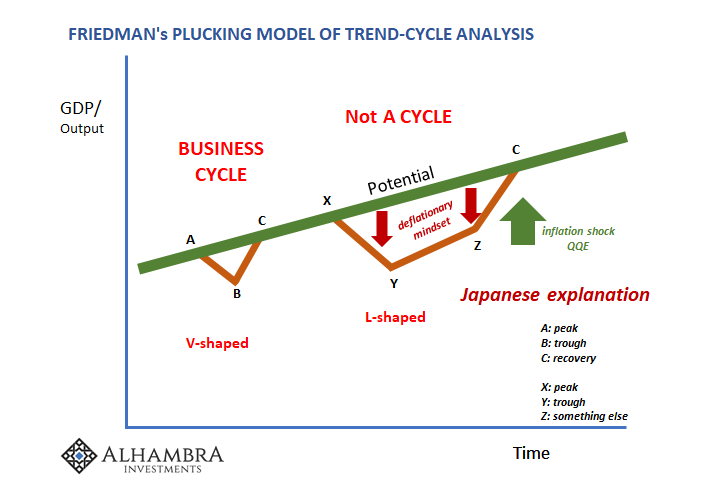

Having been in this condition for longer and having experimented with monetary policies in all shapes and sizes, it isn’t necessarily strange that the Japanese would have come to a different conclusion. For their nearly three lost decades, all 28 years falling under this “L”, they’ve blamed a “deflationary mindset” that had supposedly gripped the Japanese people after the big bubble collapse in 1990 and never let go of them.

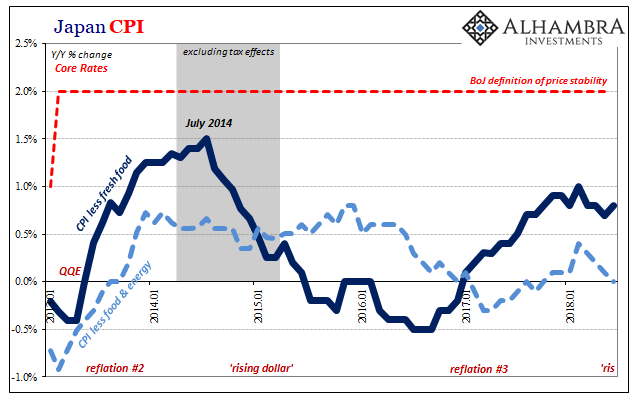

In that case, what would be required is an inflationary shock of sufficient degree so as to push out of Z and get the economy back to C. Academic arguments about Japan’s predicament have mostly been focused on what counts as “shock.” This is why you see a rising scale of intervention that has increased in quantities at intervals while also expanding the ways in which this “shock” is carried out (increasing bank reserves, then buying JGB’s, now adding ETF’s, why not stocks, too?) And this is why the CPI is of paramount importance in Japan whereas something like the PCE Deflator can be set aside by “transitory” differences.

In the late nineties, economists like Milton Friedman proposed QE before there was any, hoping that a purposeful increase in bank reserves would qualify. Paul Krugman argued that in order for this to work, the central bank had to also credibly promise to be irresponsible lest the market fall back on perceived monetary policy prudence to thwart the shock before it was ever offered.

These were the basic ideas that went into 2013’s QQE. It was to be so big and huge and sustained that it would fulfill both requirements, leaving no doubt as to the scale of “money printing” so as to pull off this double S curve attempt.

Not only hasn’t it worked, it has further wrecked the Japanese economy for the attempt.

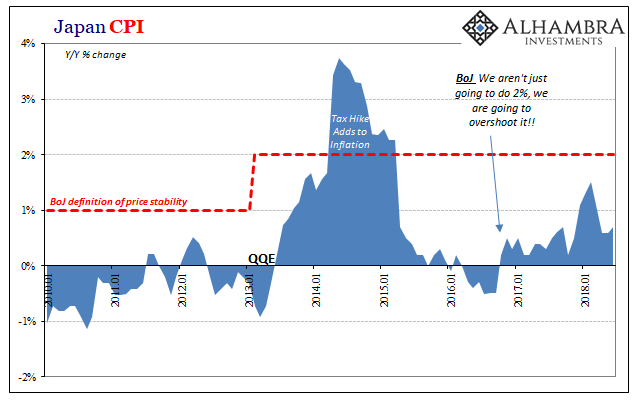

Japan’s CPI rose just 0.7% year-over-year in June 2018. That’s up slightly from April and May, but nowhere near what was supposed to happen particularly after the inflationary bump earlier this year during the worldwide inflation hysteria. Economists and central bankers especially in Japan briefly thought that QQE had taken five years to work but now they’re back to reality again.

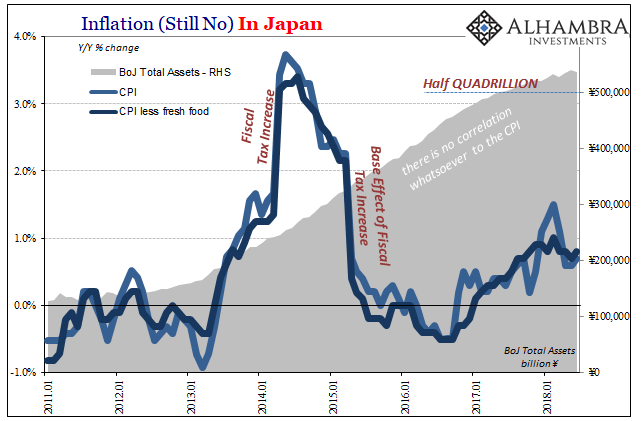

There is just no correlation whatsoever with the more than half a quadrillion in assets now sitting on the BoJ’s books and consumer prices in Japan. Core rates either suggest a restored “deflationary mindset” or, more likely, common elements with other global economies – the reflation/dollar crisis cycle of the post-Great “Recession” eurodollar decay.

If inflation is faltering again in Japan it is as likely little or nothing to do with BoJ’s QQE with YCC. Instead, as with economic uncertainty gaining elsewhere, there are warning signs registering in Japan, too.

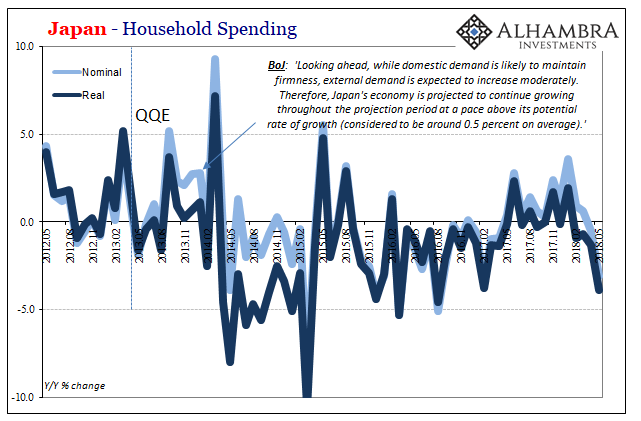

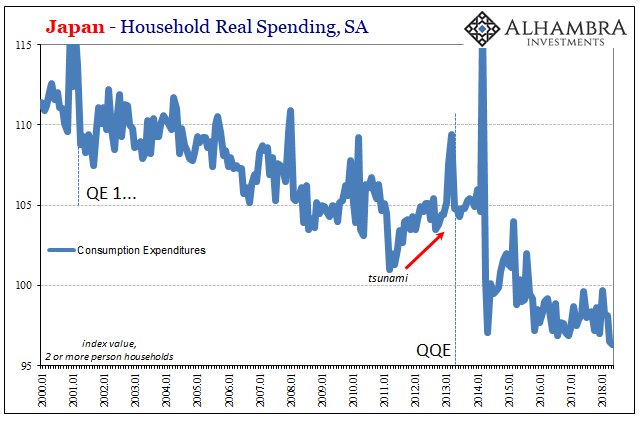

Household spending which had rebounded very modestly during Reflation #3 has tumbled especially in the last few months. In May 2018, the latest figures, Japanese household spending dropped sharply, by 3.1% in nominal terms and by 3.9% in real terms. These are more like 2016 than the 2018 acceleration that was supposed to follow 2017’s unexpected modesty.

Japan was hit by the same “dollar wave” that disrupted financial markets in January. The Nikkei had been on a very good run until earlier this year when liquidations pushed shares sharply lower there as everywhere else. Similar to European economic figures, there is a decided change in trend right as the “dollar” re-rises in 2018 (even as JPY isn’t caught up with CNY as it had been in the worst of 2015-16).

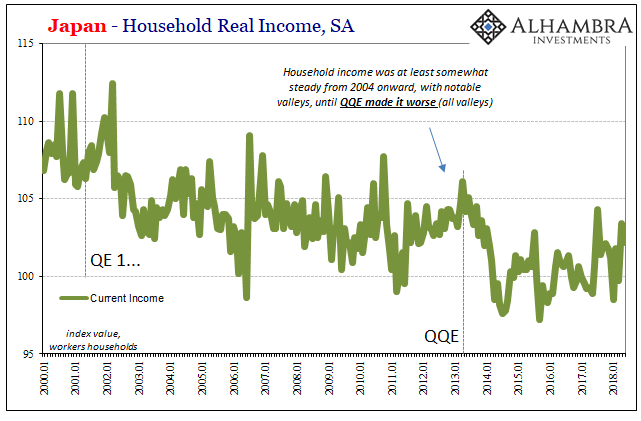

And also like Europe, this possible turn out of Reflation #3 comes even as Japanese households are much worse off for the past half-decade without the “proper” monetary shock of any of QQE, QQE2, NIRP, and now QQE with YCC.

In short, the Japanese economy remains an utter disaster, one in which it is very likely QQE contributed toward making it that much worse. And yet, I’d still take the Bank of Japan over the Federal Reserve any day.

Japanese central bankers, though they are clowns, at least recognize there is a major problem that still needs to be resolved. Japan’s authorities don’t appear capable of offering any actual solutions, but at least they are still trying because they realize that “something” just isn’t right. It’s inept but at least it’s honestly incompetent.

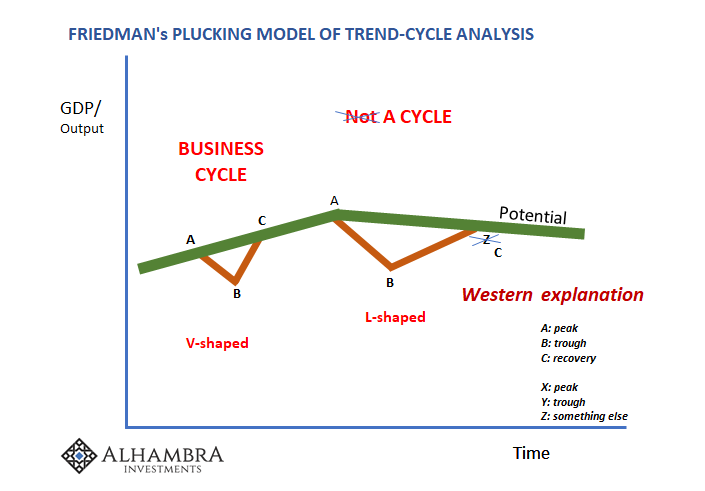

The Federal Reserve and BoE (and BoC, for that matter) are so much worse. They’ve done nothing, solved nothing, and added nothing but they’ll call it a day anyway. Their actual contributions are nothing more than increasing the divide of mistrust and the incivility that follows, all of which will eventually lead to much worse consequences down the road so long as they continue to claim Z is actually C. It’s not.

Stay In Touch