A major part of any yield curve is inflation expectations. Nominal growth particularly toward the longer end of curves sets the agenda for trading. But further out there are several confluences that may cause distortions. For Economists, these are conundrums.

There are times, however, when curve dynamics remain pretty simple. These are not usually the best of times. As my colleague Joe Calhoun points out, it’s backward in convention. In other words, what Wall Street may call a bull steepener case for the bond market is actually bullish only for those bonds contained within the curve. For everyone else, particularly the macro economy, this change works out over time decidedly bearish.

This bear steepener in reality (bull steepener in bond trading) is perfectly clear. The short end drops quickly with the long end following if at a slower rate. Nominally, the whole curve shifts lower but because the short end is moving fast the curve steepens while it shrinks. Traditionally, this is the recession signal.

If curve inversion suggests a good probability of economic contraction ahead, this bear steepener indicates that it’s close or even already arrived. The short end falls largely because authorities panic and begin the frenzied process of reducing benchmarks and such or just trying to flood money markets with what they perceive as excess liquidity in the hopes of somehow staving off the looming macro bear turn.

For most of the last year, everyone has been paying close attention to the UST curve for these same alarms. So far, treasuries have only threatened inversion. The bull steepener therefore remains only a possible future association.

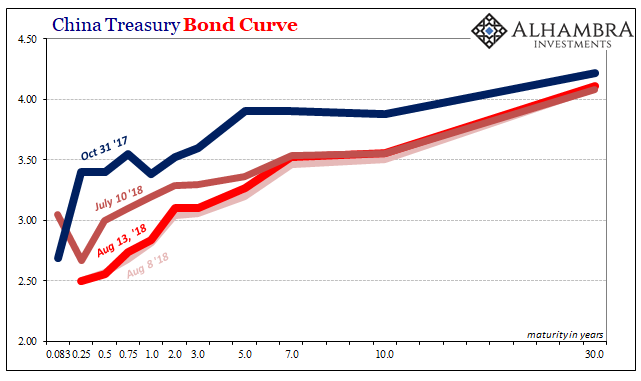

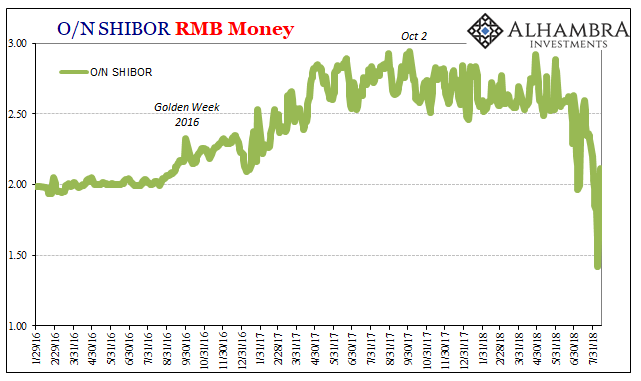

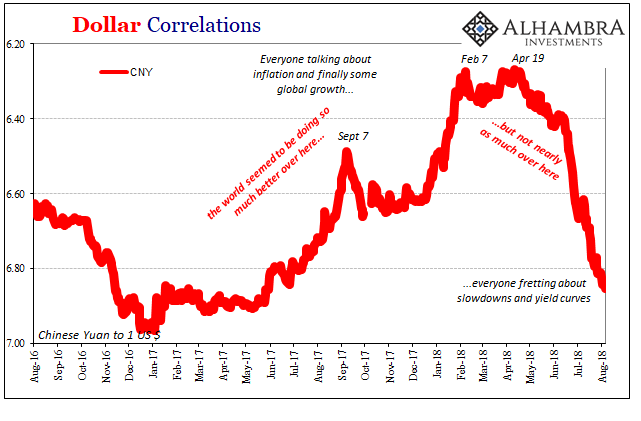

Other global curves, however, are in varying stages further along. Most importantly, China’s federal bond curve inverted at several times last year. And since the RRR cuts particularly the latest this year, money rates have recently plunged. The net result, since short-term government bonds are treated as close money substitutes, is a Chinese yield curve that last year inverted and now clearly displays the bear steepener case.

The overnight SHIBOR rate has rebounded from its low last week of 1.422% to today 2.113%. This still represents a substantial move on its own terms, as well as still the reason for the curve’s shape today.

Globally synchronized growth increasingly disappears from even expectations. Last year was supposed to represent the opening stages for a worldwide inflationary breakout; a burst of welcome positive pressures representing the first real steps toward normalcy in more than a decade.

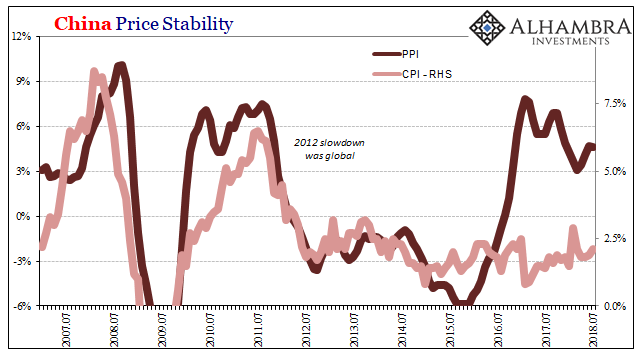

Many curves traded in that way, if only in parts. The UST curve as well as China’s bond curve both resisted at their long ends, therefore leading to their relative distortions. “Everyone” knew that inflation was going to shift to the primary problem for the Chinese from years of deflationary undershooting.

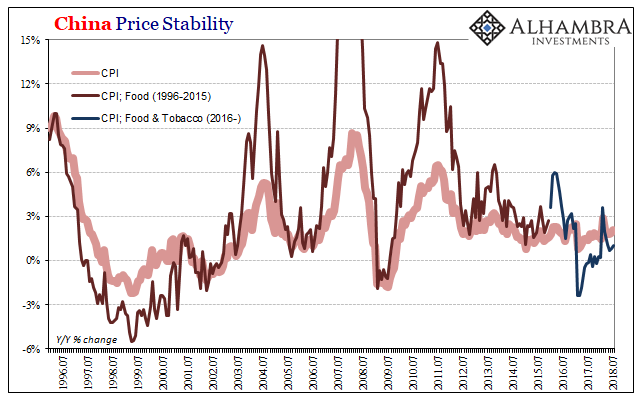

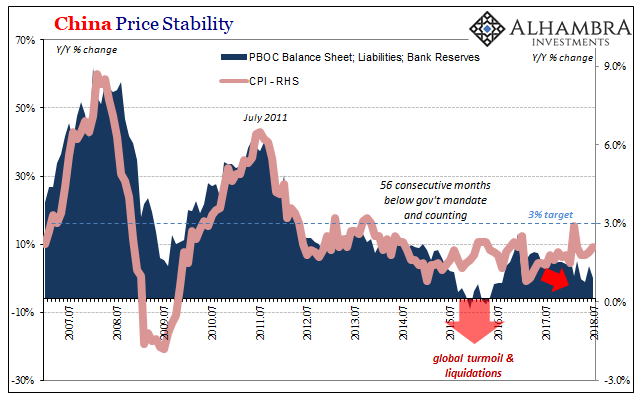

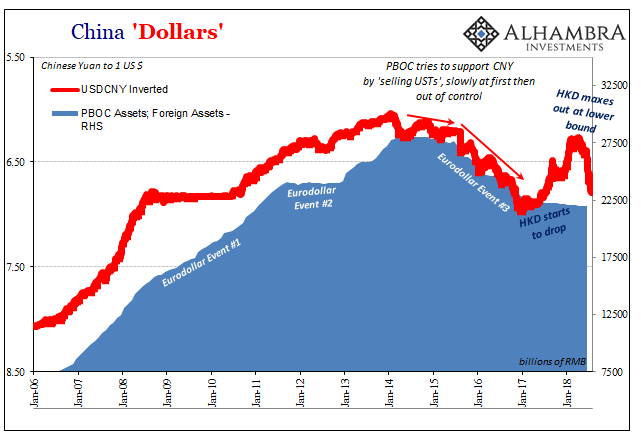

Only there is no indication of anything having changed on that important account. The latest inflation estimates from China’s National Bureau of Statistics are just as low and tame as they have been since the end of 2013; that was both the last time the Chinese CPI matched the government’s mandated level of price stability (3%) as well as the start of the PBOC’s still epic struggle with the asset side of its balance sheet (“dollars”). At just 2.1% in July 2018, the CPI remains conspicuously unmovable.

The lack of any acceleration in inflation at all, let alone an actual break higher, now up to July in 2018 data is pretty substantial evidence that there is no economic basis for China’s part in globally synchronized growth. Nothing has changed, at least toward the positive side of things.

Balance that against a growing list of severe negatives, and the bear steepening in China’s federal curve actually makes more sense than perhaps anything else out there among major prices and indications.

This doesn’t necessarily mean that a full-blown Chinese recession is imminent. We have to maintain even and rational analysis so as to avoid the making the opposite mistake as inflation hysteria. In other words, China’s bond market is projecting a dramatic shift in perceived risks. The Chinese economy may not yet be set afire.

Whereas there was more limit worries last year (long end) those are less heterogeneous this year. There was at least in 2017 a relatively widespread belief in the media as well as some markets that some upside was possible. Reflation sentiment had engineered a change in the spectrum, so that a sizable chunk of economic and financial agents considered and acted upon (PPI) what that might look like if it was to materialize.

Without any tangible progress along those lines, China’s economy like the rest of the global system has at best stalled, dreams of the upside fade further into the same tortured memories as these past reflation cycles. In their place are these all-too-familiar indications of markets more obsessed by a growing downside gravity.

As cycles-within-cycles play out, like the first few months of 2015, it doesn’t appear on the surface as if there is anything really to worry about. There is lots of financial smoke, but none as yet economic fire. It can lead to a false sense of comfort in certain places (the economy is strong!)

China’s bond curve and the continued stickiness of their CPI are adding a whole bunch of smoke.

Stay In Touch