I was going to write that there was bad news out of Japan last night, but is there really any other kind? I know that from time to time Japan’s various rebounds over the years are characterized as the greatest economic achievements in human history, but by and large very few outside the media actually believe that. Thus, there is really only three classifications for Japanese economic statistics: bad; becoming more bad; and, unusually bad.

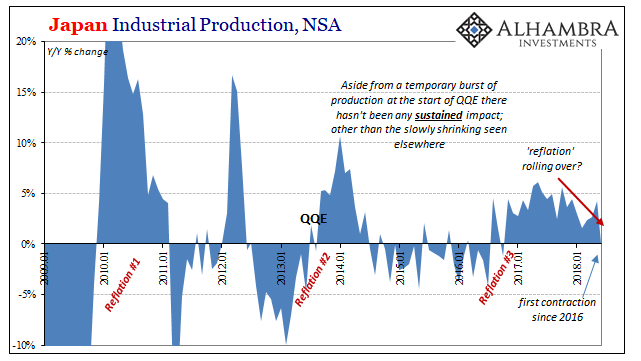

From that point of view, Industrial Production in Japan is perhaps the best, most accurate barometer of the global economy and whatever its marginal direction. It follows pretty closely these reflation/deflation cycles we find everywhere starting in the global eurodollar system. As I wrote back in April:

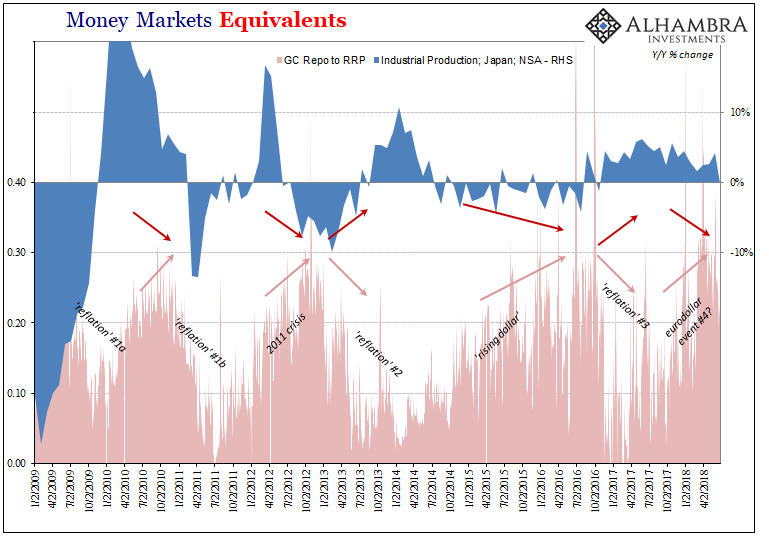

In other words, for almost all of Japan’s post-crisis experience its IP statistic is contracting. The positives are far fewer than the negatives. They correspond easily with these obvious “reflation” episodes we find all over the world created by the abatement of destructive eurodollar impulses unleashed in intermittent fashion (nothing goes in a straight line).

Therefore, Industrial Production in Japan just may be the best “reflation” indicator there is anywhere in the world. If that is the case, and it’s hard to argue otherwise, a potential rollover in it starting in the middle of last year would be quite concerning as it stands starkly against both inflation hysteria and “globally synchronized growth.”

Since nothing ever goes in a straight line, Japan’s IP rebounded ever so gently in the few months since then. Not in the latest data, though, as we find Japanese industry contracted slightly in June 2018 for the first time since 2016. It would appear in the larger trend Reflation #3 is indeed rolling over and out into what may be this Eurodollar Event #4 (or dollar disorder four, if you like).

This is somewhat confounding at least to the idea that this is all trade war stuff. If that was so, then why isn’t Japanese manufacturing in particular truly booming? Trade wars are essentially zero-sum games, meaning that if the US is going to lose market share under retaliation then that should be someone else’s gain.

With the yen where it is, Japan Inc. should otherwise be poised for success especially with globally synchronized growth as the background. If there would be one true positive for the Japanese economy, it would be for all its biggest partners to fight it out politically while Japan’s companies waited patiently on the sidelines to offer a non-controversial alternative to one another.

Instead, as would be the case under another significant monetary episode, it appears as if things are getting bad for everyone. Or, properly classifying Japanese IP, becoming more bad all over again.

Stay In Touch