If everything was going to plan, non-standard monetary policy at the zero lower bound (QE) would have raised inflation expectations increasing the level of aggregate demand as businesses and consumers ramped up their activities in anticipation of higher costs. The more this “overheating” goes on, the more forceful it becomes. Eventually, by virtue of the Phillips Curve, aggregate demand is so strong for so long that any slack in the labor market is absorbed leaving businesses to energetically compete for workers.

At that point, companies have no choice but to pay more for marginal labor which then leads them to pass along those costs to consumers in the form of higher prices. Consumers, as workers, are getting paid more so they absorb those higher costs but in turn raise their own pay expectations. These then feed back through the labor market in the form of spiraling wage demands, which companies pass back to workers, and so on.

The net result: 1978. This has become the obsession for central bankers. They have decided that the worst case is repeating the Great Inflation, and largely because they’ve decided repeating the Great Depression, in kind, isn’t possible. Their primary fear is not without good reason, at least in their own self-interest. The last time the world was joined together in its righteous anger over Economists’ incompetence was at the tail end of the seventies.

They always fight the last battle, never look ahead to the next one.

But since they’ve also banished any study of money within their statistics-based discipline, how will they know in which part of the process the current economy resides? And if there are questions about that, how can they possibly know what comes next?

This is the world Jay Powell has inherited from Janet Yellen, who in turn had inherited the same ambiguousness from Ben Bernanke. If they were sure that they had made aggregate demand sufficient, enough to have absorbed any lingering slack leftover by the Great “Recession” an embarrassing ten years ago, they wouldn’t be “raising rates” a little here and there, just a few hikes each year.

They claim confidence about the economy but act very differently. For one, the data just isn’t behind them. The end of slack remains in the future tense.

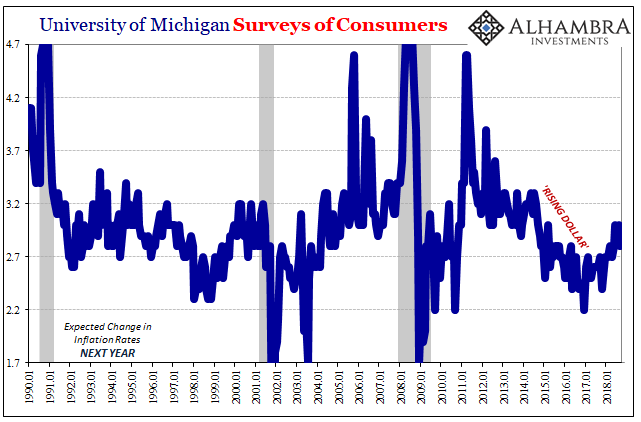

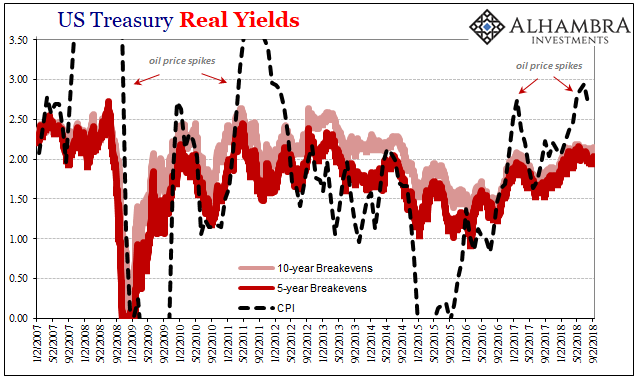

Though short-term expectations have ticked up from the lows of 2016, they remain suspect. By comparison with 2014, for example, expectations are still equal (market-based, TIPS) or in many consumer surveys significantly below. Rising oil prices, the main component of the PCE Deflator and CPI’s latest spike, haven’t been viewed as anything more than commodities.

This despite four QE’s (in the US) and coming up on a whole decade since ZIRP. Even after almost three years of “rate hikes”, the FOMC still characterizes less than 2% federal funds and money rates as “highly accommodative.” If that was so, consumers aren’t seeing its anticipated products. Not even constant pronouncements and official emphasis of this “strong” or “booming” economy has moved the needle.

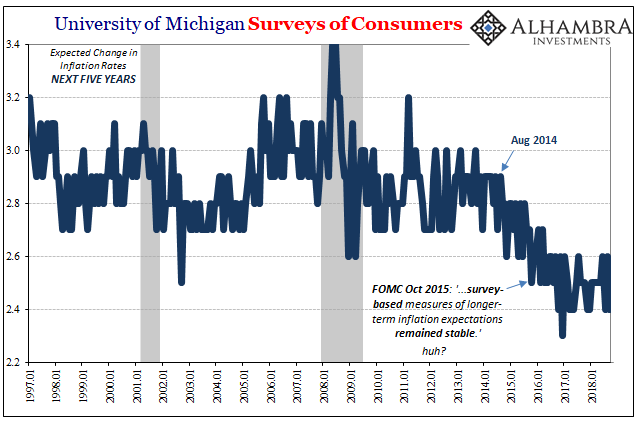

Longer-term expectations are an even bigger problem for Powell’s view. They tumbled in 2014 as the dollar rose and deflation re-emerged at exactly the moment everything in the economy was supposed to go the other way. Consumers appear to have learned when, and what, central bankers didn’t, or won’t.

Instead of seeing these data signals for what they clearly are, Economists instead have dismissed them. The media is drowned in one-off anecdotes of a labor shortage that consumers aren’t finding, nor does it show up in actual data. One St. Louis Fed branch VP in 2016 suggested Americans were too stupid to notice the central bank’s great success in fostering this recovery process.

The above evidence suggests that monetary policymakers may want to think hard about how they use individual inflation expectations surveys to inform monetary policy—at least until the nation’s economic education program raises the public’s understanding of inflation.

“The above evidence” consisted of nothing more than professional forecasters professionally producing forecasts that like central bankers keep expecting this pickup in inflation; Economists agreeing with other Economists. Two years later? Workers are still waiting; the data confirmation curiously remains missing. Better education is required, alright.

That’s the consistent message from muted inflation expectations, both surveys and markets, as well as data.

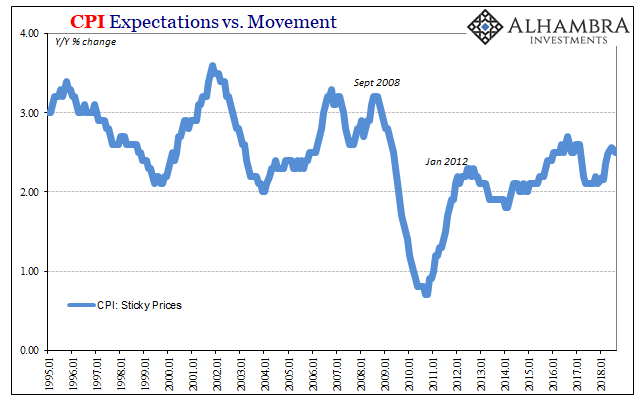

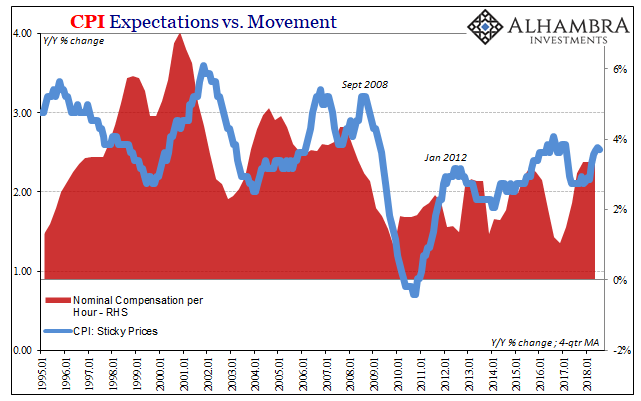

For example, the CPI’s “sticky” components are where we would expect to find broad inflationary pressures to begin registering. These are items in the CPI basket which would only accelerate if what Economists think has happened has actually happened (thus the term “sticky”). Once wage pressures are at a national rather than purely anecdotal scale, the inflationary spiral can then begin.

Like a lot of inflation indices, this one is higher in 2018 than 2017 or 2013, but not meaningfully so.

Compared to prior periods of tight labor markets or recovery dynamics, consumer prices aren’t really accelerating as they would if Economists have it right. In fact, this major part of the CPI is following along very closely to wage and compensation data.

Both wage data as well as “sticky” prices are joined in their quite dour economic assessment.

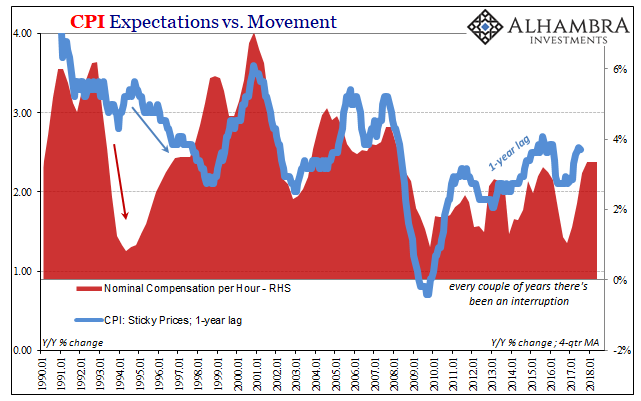

In series after series, wage growth is as tepid as the CPI, sticky or not. If companies are experiencing a labor shortage, they are neither paying up for labor nor passing along any increased costs to consumers (and if they aren’t doing they one there is no need to do the other). Adjusting for lags in the process (below), as Economists theorize there is a very clear historical relationship between wages and consumer prices.

Unfortunately for Powell and Economists, this only confirms their forecasts as irrational and their protests as unprofessional.

A big part of the problem becomes clear in this particular comparison – every few years the labor market as macro economy is interrupted. As reflation gets going it is “unexpectedly” halted by these intermittent problems, the last one, the third in 2014-16, having finally been absorbed by all sorts of measures of inflation expectations. Americans aren’t at all uneducated about money, inflation, and economy, the data having since continued to corroborate their deepening pessimism.

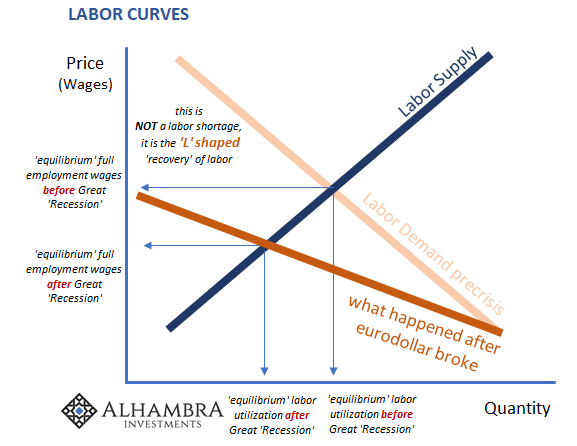

This is all part of what Janet Yellen was trying to say last week, but was too careful lest she forthrightly admit to her part in what has been a tremendous, and catastrophic, failure. In this context, the economy can’t be anywhere close to the inflationary spiral because it hasn’t yet made up so much lost ground over the last ten years. Slack in the labor market must still be huge simply because all the data, inflation, wages, and expectations, agree.

No wonder Jay Powell, as Janet Yellen, is going so slow. They’ve got nothing right. If Powell makes it the whole four years, I’m sure he’ll eventually make his own cryptic admission, too. The data, at least to them, only matters once they’re out. The rest of us aren’t so lucky.

Stay In Touch