Here they come. After spending more than a year talking about nothing but good things ahead for the global economy, Economists are beginning to sound worried. In 2017, there wasn’t anything that could stand in the way of synchronized growth. In 2018, there’s no longer any synchronized growth, so now we can talk about what was standing in the way.

The latest is the IMF’s Managing Director Christine Lagarde. From earlier today:

Six months ago, I pointed to clouds of risk on the horizon. Today, some of those risks have begun to materialize.

That’s all well and good, but where were you last year? Lagarde last October:

Well, we would see that the long-awaited global recovery is taking root…Measured by GDP, nearly 75 percent of the world is experiencing an upswing; the broadest-based acceleration since the start of the decade. This means more jobs and improving standards of living in many places all over the world.

From recovery taking root to recovery being uprooted in about a year. Well done.

What happened was Trump, she says, but also, according to Bloomberg’s paraphrasing, “A strengthening U.S. dollar and tightening financial conditions have increased challenges for many emerging markets.” That’s the thing about starting from such a low-grade rebound as was actually the case last year; even if the trade war stuff was really the cause, had the global (in particular Chinese) economy been living up to the words the trade wars would’ve been small issue in 2018.

Instead, they are being made into the issue when the deficiency and therefore real economy drag is the same as we’ve seen (three times) before. Not that Christine Lagarde would know.

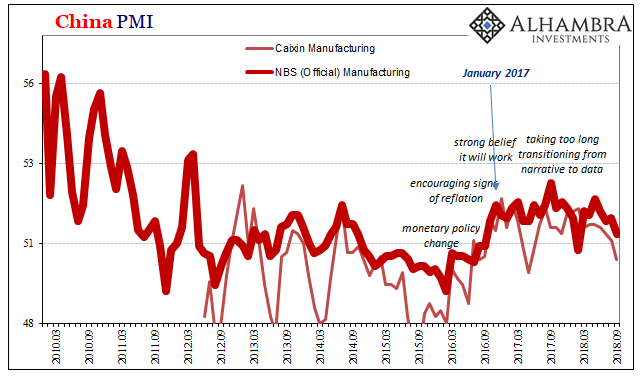

Ahead of their Golden Week National Holiday, China’s National Bureau of Statistics reported that manufacturing sentiment is down again. It’s not a slowdown that is materializing across Asia, it’s a rolling over.

The official PMI for manufacturing dropped to 50.8 in September from 51.3 in August. That’s the lowest since February’s distorted number, together the only two months less than 51 since September 2016 way back at the start of Reflation #3.

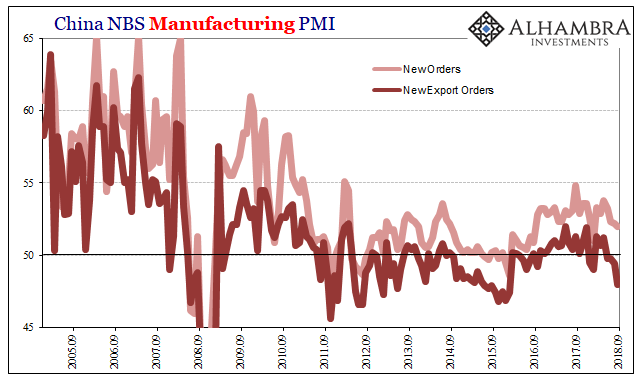

The private Caixin manufacturing survey fell right to 50. Down from 50.6 the month before, this sentiment indicator was the lowest since May 2017. In both manufacturing indices, new orders particularly relating to goods intended for export have fallen considerably. Trade wars throwing up barriers, or global demand falling under a revisiting eurodollar squeeze?

Speaking out on global inequality, the leader of the IMF forgets from where she opines:

In too many cases, workers and families are now convinced that the system is somehow rigged, that the odds are stacked against them.

Could it be that workers and families are sick of hearing about a long-awaited global recovery taking root, only to then sit idly by while the same officials after a suspiciously short period quietly admit both that it really isn’t coming and its further painful absence just isn’t their fault?

It wasn’t the first time she used that particular line, either. In a speech all the way back on June 17, 2015, Lagarde told assembled Catholics in Brussels:

In too many cases, poor and middle-class households have come to realize that hard work and determination alone may not be enough to keep them afloat.

Too many of them are now convinced that the system is somehow rigged, that the odds are stacked against them. No wonder that politicians, business leaders, top-notch economists, and even central bankers are talking about excessive inequality of wealth and income.

She never once mentioned the dollar in that speech, not yet five months after the Swiss National Bank’s shock response to it and less than two months before the PBOC’s. The next time any IMF official mentions eurodollar will be the first.

Politicians, business leaders, “top-notch” Economists, and certainly central bankers don’t really have to worry about such things. It apparently does them no good to be talking about it, they don’t ever deliver anything. The unexplained slowing and even the possible halting of China’s unimaginable demographic transformation won’t hit any in the establishment classes in their wallets in a way it will be felt far outside of Chinese borders. They are all perfectly insulated from the lack of economic growth permeating underneath.

The funny thing is that people like Lagarde know what the problem is, even if they don’t know who’s responsible for it (mirrors are apparently forbidden equipment). The first priority for “stronger, more inclusive, more sustainable growth”, according to the IMF as well as central bankers, is sound policy she said back in 2015.

If you do not apply good monetary policies, if you indulge in fiscal indiscipline, if you allow your public debt to balloon, you are bound to see slower growth, rising inequality, and greater economic and financial instability.

If you can’t define money, how might you “apply good monetary policies?” Good according to whom? If you keep saying recovery only to see it fizzle for yet another time, some might reasonably conclude the system really is “somehow” rigged – and begin to act in defiance of such obvious dishonesty. Lagarde wants you to know she cares about the poor, just not enough to actually do something for them. The IMF and central bankers would be far better served if they just came and said, “We really don’t know what we are doing.”

At least then people would realize Economists have no idea which way the economy will go in any given year and expectations could remain properly tempered. It would be a place to start.

From globally synchronized recovery to darkened skies. It’s amazing what a dollar (short) will do.

Stay In Touch