China’s economy is not crashing. Hyperbole works both ways. Last year and this, the smallest increment above a prior number was broadcast out as the greatest thing ever (US wage growth in particular), irrefutable proof of globally synchronized growth. Now that that’s over with, largely, there will be a tendency toward the other extreme.

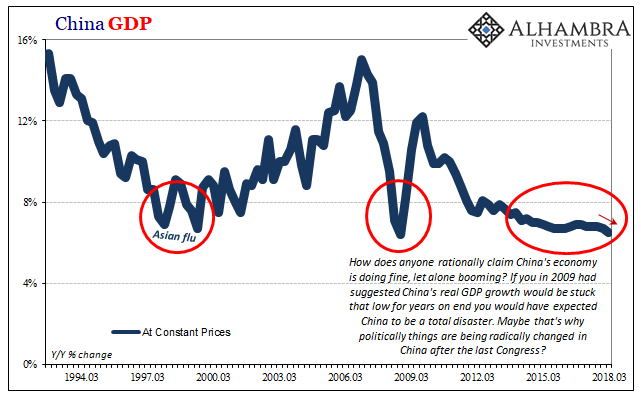

The latest Chinese economic statistics are for several of them the lowest in some time. Starting with real GDP, at just 6.5% in Q3 2018 it’s the slowest pace since the first quarter of 2009. That’s not good especially for a statistic of such dubious practices often specifically crafted to be the best it can be.

What that suggests is not immediate catastrophe, offering instead more complete confirmation that this major economy is slowing. Again. This is the real story in China and therefore for everywhere else.

In other words, the real danger presented by these statistics is not imminent crash but rather the total disappearance of any upside potential. Even during 2017, the narrative about globally synchronized growth continued as a future property. The global economy in that year was clearly better than it was during the worldwide downturn 2015-16, easy comparison, and that was expected only as the first step toward meaningful acceleration and then recovery.

Where Economists and central bankers jumped the gun was in assuming that 2017’s improvement was the only evidence they needed for those complete expectations. As it has turned out, as it always turns out, changing from minus to plus signs is a necessary condition for better days but not by itself a sufficient one.

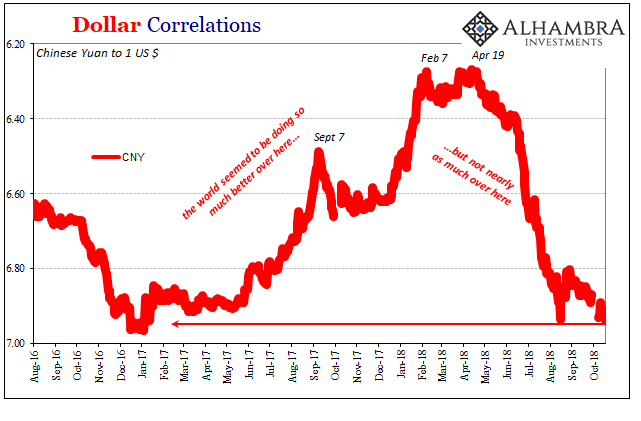

Acceleration requires momentum among other factors, and momentum is derived from conviction. The best days of 2017 never really had that, the absence perhaps clearest in China (particularly the hollow rebound of CNY which “somehow” lacked “capital inflows”).

Everyone kept waiting for the Chinese to zoom on ahead and bring the whole up with them. Meanwhile, in China they kept waiting for the rest of the world to take the lead so as to pull them up out of their funk. That’s been the thing about “global growth” since 2011, everyone expects that someone else will solve their economic problems for them. Momentum will arrive, you see, it’ll come from somewhere else.

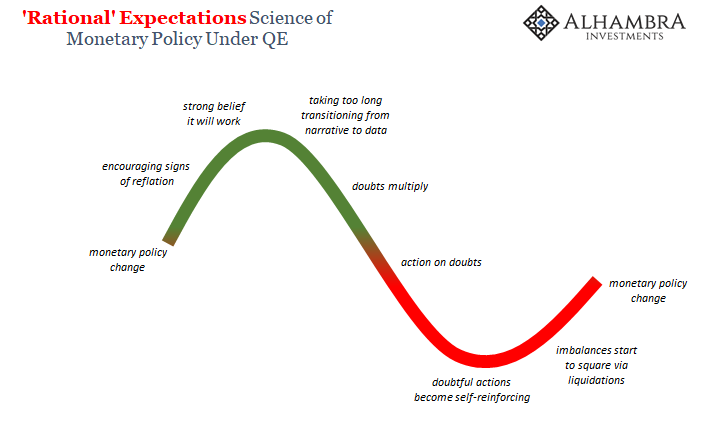

Without a clear path to that next step toward recovery, doubts multiply rather than abate. What was for a time mild opportunity, reflation, sinks back toward the malaise of liquidity risks that over time can only return to self-reinforcing.

This is what’s significant about China’s numbers today. They practically declare reflation dead and gone. There is no upside left, what you saw in 2017 was the best of it – and it wasn’t very good. It was, in honest analysis, not really that much better than 2016 at all; certainly less than the prior peak.

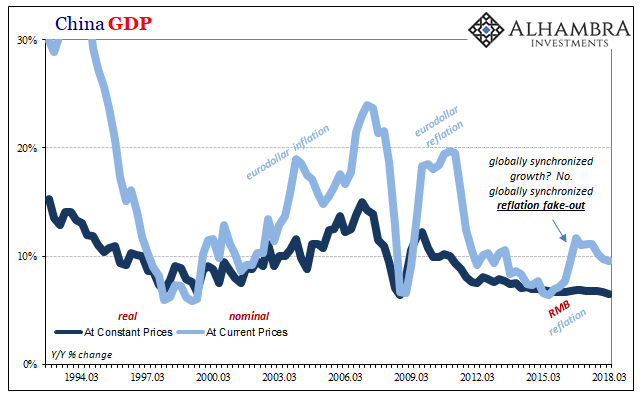

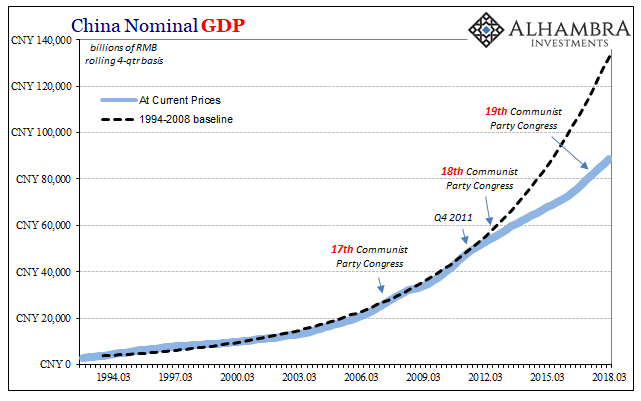

The rest of the statistics bear this out. Nominal GDP, perhaps a more appropriate measure of China’s economic conditions, decelerated yet again in Q3. Year-over-year, it rose just 9.6%, down from 9.8% in Q2 and a peak of 11.7% set way back in Q1 2017. The more time passes without clear acceleration, the more it has to sink in (everywhere but Washington DC) that this really is a rising dollar “L.”

The world economy has never recovered from the 2011 eurodollar crisis (squeeze). The system broke in August 2007, and created all sorts of devastation immediately thereafter. But for a time in 2010 and the first half of 2011 it looked like recovery was at least possible if unusually weak.

Economists, incapable of appreciating the global monetary system for their modern practice of neglect, mistook 2011 for a lack of sufficient time; they crafted monetary policies (with no money in them) so as to buy the financial system enough of it thinking that would be the magic elixir.

Instead, time has proven beyond all doubt that 2011 was the last stand for recovery. It just isn’t possible so long as the global reserve currency, the eurodollar not dollar, remains dysfunctional. There can never be enough momentum to escape, opportunity surrendered by this neglect.

The more Chinese statistics in particular show this to be true the more it will spread and eventually become self-reinforcing (again). In certain places, it may have already.

The rest of the data follows along this way; not crashing but what may be worse as the end of any upside.

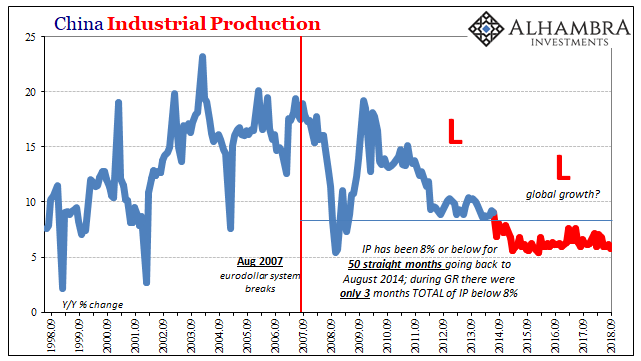

Chinese Industrial Production rose just 5.8% year-over-year in September, the first month below 6% in two and a half years going all the way back to the trough of the last downturn in February 2016. As noted at the outset, there can be an inclination to make more out of that comparison when, for now, it simply confirms there just isn’t any recovery.

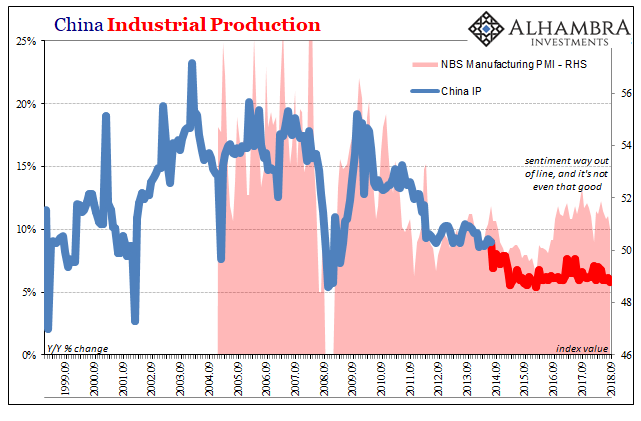

Along those lines, it stands in sharp contrast to sentiment which even in China had gotten way ahead of economic reality. It’s another element of 2017 and globally synchronized growth that is being slowly, steadily undone in 2018. Sentiment has proved a worthless indicator, and well beyond the other side of the Pacific Ocean.

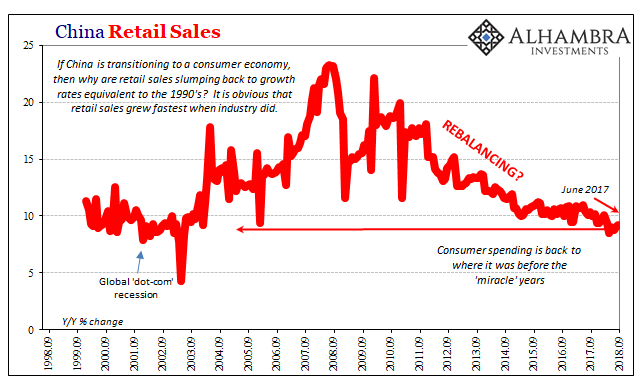

Retail sales was practically the lone bright spot, which merely means there wasn’t as much slowing as there had been. Rising 9.2% in September, it was the fastest pace in five months, but still materially less than the 10%+ rate that prevailed 2015 forward.

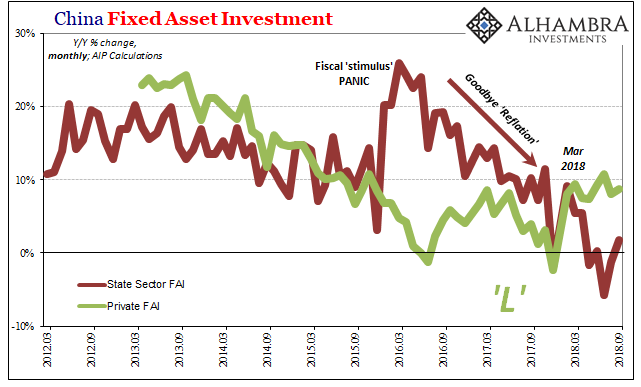

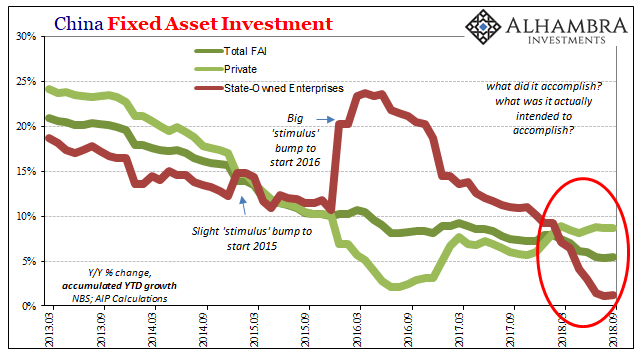

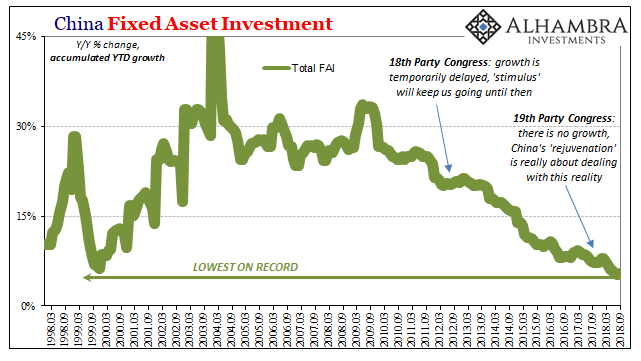

Fixed asset investment managed to tick a little higher last month as private capex remained steady while government investment rebounded slightly. Overall, FAI was up 5.4% on an accumulated basis (YTD) compared to August’s record low 5.3%. Private FAI also on an accumulated basis stayed at 8.7%. State-owned FAI gained 1.2% last month compared to 1.1% the month before.

China’s economy is not crashing. However, it is slowing and from an already weakened level. The Chinese system did not actually recover from the last downturn despite now three years distance. What these numbers show is that, like the eurodollar system, there is now very little chance that it ever will. It may not seem like much compared to a full-blown breakdown, but pretty conclusive evidence for a worldwide, multi-year (decade?) “L” should be terrifying.

A world without opportunity is a far more dangerous one than a world only temporarily stripped of it. The V can be scary but only on the way down. The L is, well, I think we’re going to find out.

Stay In Touch