On June 15, 2007, not even two months before worldwide panic would break out, Federal Reserve Chairman Ben Bernanke was in Atlanta, Georgia, speaking at a monetary policy conference. Sponsored by the Atlanta branch of his organization, as fate would have it Bernanke’s chosen topic was the credit channel for monetary policy.

This is something the scholar Bernanke supposedly knew well. He had made his early reputation writing in 1983 about how the Great Depression was made “great” through the two propagations of financial dysfunction. In one sense, the future policymaker wrote, the closure of so many banks reduced the fundamental capacity of the banking system to develop intermediation, or what he called information capital.

The other was how a banking crisis and the economic disruption which follows might impact the creditworthiness of borrowers. Whether we think about it or not, almost all lending takes place on the basis of collateral. When you buy your home, you put up that very structure as collateral securing the loan.

What Bernanke noticed was how in the 1930’s after the collapse Americans’ collective inability to free up collateral for borrowing hampered what he called the efficient allocation of credit. It played hell on monetary policy as one result; or what in the 21st century they would call a clogged transmission mechanism.

Just as a healthy financial system promotes growth, adverse financial conditions may prevent an economy from reaching its potential. A weak banking system grappling with nonperforming loans and insufficient capital or firms whose creditworthiness has eroded because of high leverage or declining asset values are examples of financial conditions that could undermine growth. Japan faced just this kind of challenge when the financial problems of banks and corporations contributed substantially to sub-par growth during the so-called “lost decade.”

It is interesting that he would say this in June of 2007. A banking system might be weakened for reasons other than capital or NPL’s, too. One that is perpetually distracted by a high degree of liquidity risk, for example, would act in the same way as Japan’s did during its lost decade(s).

Combine that with Bernanke’s proposed collateral creditworthiness problem, and it makes for all the ingredients of at best less effective monetary policies. The results, Bernanke warned, might be a prolonged period of aftermath.

The inverse relationship of the external finance premium and the financial condition of borrowers creates a channel through which otherwise short-lived economic shocks may have long-lasting effects…This “financial accelerator” effect applies in principle to any shock that affects borrower balance sheets or cash flows. The concept is useful in that it can help to explain the persistence and amplitude of cyclical fluctuations in a modern economy.

There is, as always with Dr. Bernanke, a lot of econometric gobbledygook but what he is saying is that there is always the potential for financial conditions (i.e., a credit crash) to play a role in suppressing, or accelerating if it’s a positive shock, longer run economic results as they relate to economic potential.

As the decade of the 1930’s demonstrated, there may not be time limit on these effects, making them hard to distinguish from the things we all know create that potential (productivity, demographics, creativity and freedom of entrepreneurs, etc.). In short, there are a number of ways a monetary problem can string out economic problems for a very long time.

Again, Bernanke said this in June 2007.

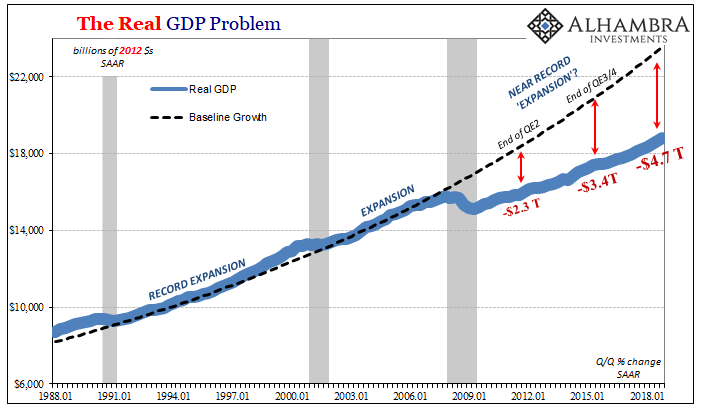

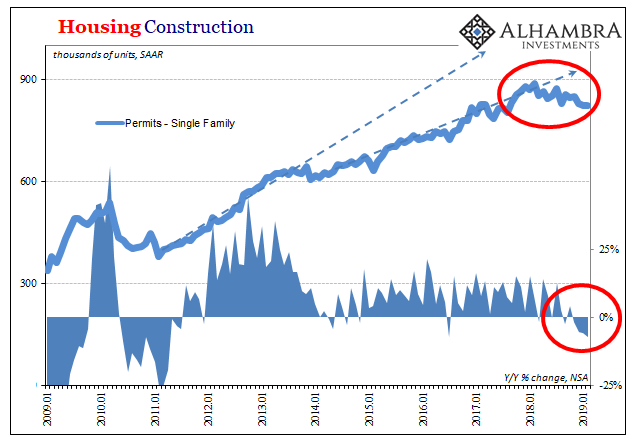

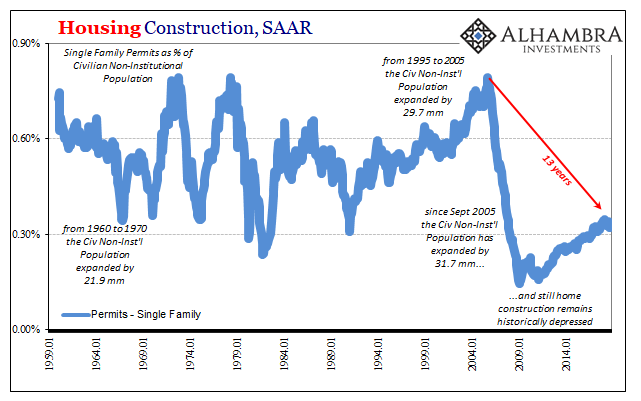

It doesn’t take a trained Economist (you are better off if you’re not one, actually) to see at least part of the good doctor’s thesis coming to fruition in the housing market these last twelve, thirteen years. As it relates to the creation of collateral, the real estate system just isn’t producing. The Kansas City Fed was stunned last year to find out the housing market across the US hadn’t recovered, and then, consistent with the times, the Wall Street Journal attempted to make this out to be a good thing.

It’s one big reason to doubt persistent claims that monetary policy has been “accommodative” for a very long time. Perhaps in theory it has (though I constantly argue otherwise), but not so much in practice. Even those QE’s which were purposefully directed toward housing finance, distorting TBA’s and dollar rolls for MBS, what did they really accomplish?

Any honest review of the housing sector has to question the results, as KC did last year. As one Economist noted last April during those last gasps of inflation hysteria:

“Americans are essentially staying put in their homes for the foreseeable future, either by choice, or by necessity or some combination,” said Bankrate.com senior economic analyst Mark Hamrick in a press release.

Rather than drug addicts and retiring Baby Boomers, none other than Ben Bernanke gives us one possible legitimate answer as to why long run the economy remains so depressed. We know for a fact the housing market is; and now it, too, has found a renewed slump, the most profound since the last big bust.

As Bernanke concluded back then:

The critical idea is that the cost of funds to borrowers depends inversely on their creditworthiness, as measured by indicators such as net worth and liquidity.

No wonder everyone keeps buying up UST’s no matter how many times they’re told not to (the whole bond bull thing). If only there had been an effective, capable government-sponsored institution in place to keep something like that from happening, chaired, of course, by someone who wrote the book on the first time the country was forced to live with the long run consequences.

Stay In Touch