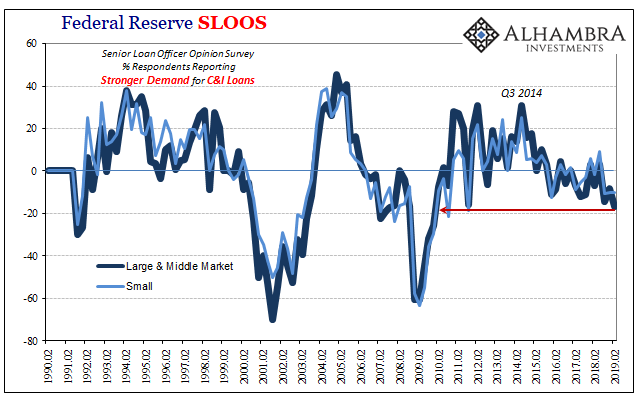

More US bank respondents reported to the Federal Reserve that they are seeing weaker demand for Commercial & Industrial Loans than at any time since the end of the Great “Recession.” The Senior Loan Officer Opinion Survey on Bank Lending Practices (SLOOS) asks respondents to gauge certain factors with regard to various forms of lending.

In terms of new debt to commercial and industrial customers for commercial and industrial purposes, the survey conducted last month reports the net percentage of domestic financial firms indicating strong demand for these kinds of loans was -16.9%. Nearly seventeen percentage points more on the weak side than stronger. That’s more downside skew than in Q4 2011, the most since the first quarter of 2010.

It isn’t a huge change, the downward bias mostly intact since the eruption of Euro$ #3 (“overseas turmoil”, to Yellen’s Fed) in Q3 2014. However, there is a notable shift toward reporting weaker demand starting in Q4 2018 – the same October to December window suggested by both market conditions as well as global economic evidence.

This hasn’t yet translated into lower lending volumes and outstanding debt. Yet. Typically, banks have reported reduced demand while still booking more loans. There is a definite lag to C&I lending.

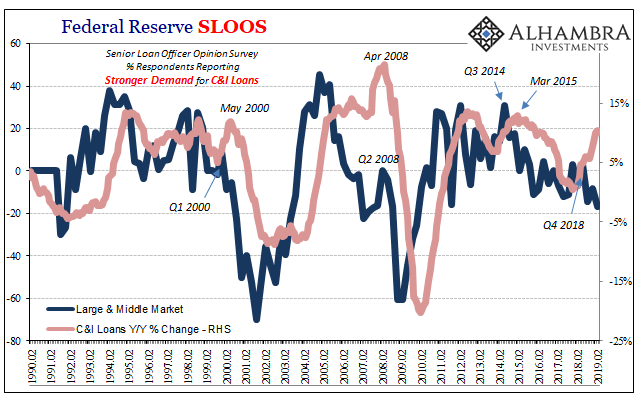

In the dot-com recession of 2001, C&I loan assets didn’t actually decline until the month before the official (NBER) start date of that particular business cycle trough. The SLOOS survey, on the other hand, had suggested seriously slowing demand right after Q1 2000 (dot-com peak).

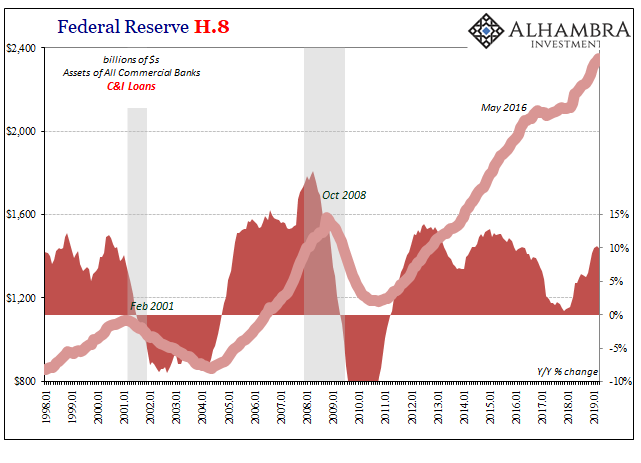

During the Great “Recession”, banks continued lending heavily in commercial and industrial purposes all the way until the very heart of the global panic itself. It wasn’t until October 2008 that loan assets in the space peaked, though SLOOS indicated a turn toward weaker demand seven months earlier around Bear Stearns.

Even during Euro$ #3, as noted above senior loan officers reported a downward change in perceived demand for C&I loans starting in the fourth quarter of 2014. Loan assets would continue to increase until the middle of 2016 (balances never did contract, though they came close as a result of 2015-16’s near recession).

In some ways, recent data poses a unique challenge; SLOOS says demand never really rebounded after Euro$ #3 but C&I lending growth picked up starting early last year. Tax reform difference? Most likely.

Either way, at some point these two series are almost certain to converge. Bank managers are going to start reporting stronger demand for Commercial and Industrial Loans, or businesses are going to finish up whatever debt is in the financial pipeline and then hold steady – if not curtail their debt risks in the face of uncertain global economic circumstances.

The historical correlation is pretty clear on this one. Factoring these lags, far more likely the latter therefore another piece of evidence pointing to further serious economic risks still ahead in 2019. The survey, remember, was conducted last month. Several months into global central bank “dovishness.”

Stay In Touch