It’s a pretty simple question, at least when asked by a member of the American citizenry not already compelled by one bias or another. Did the 2009 “stimulus” bill (American Recovery and Reinvestment Act; or ARRA) work? The answer depends upon who you ask, including breaking down along partisan lines. To Democrat Economists, it absolutely did. For their Republican counterparts, snicker snicker shovel-ready.

What anyone really wants to know is did all that government activity, and there was a lot, did it add something substantial to the positive forces which led to a real economic recovery? That is the question. It’s even in the name.

And nobody wants to tackle it head on. Instead, even getting away from the partisan bickering you end up in the land of obfuscations anyway; the realm of econometrics. Ask a non-political Economist about the ARRA and you won’t get a straight answer, either; your first clue.

You can go out there and find any number of post hoc analysis of every variety and category. What unites them all is their conclusion, phrased a little differently each time and worded carefully, but all end up sounding pretty much like this one written by the Philly Fed’s staff in 2017:

Did the Recovery Act work? The evidence suggests the economy did indeed grow more than it would have without the stimulus but likely not as much as it might have with a different type of stimulus.

That’s about as honest an answer as you’ll find and it still avoids the main question. “Grow more than it would have” isn’t what’s been asked; the entire issue is recovery, not this idiotic blend of “jobs saved.”

When we use the word “recovery” we mean for it to be literal; as in, get back to where we were before. That’s how the economy has performed in each and every post-war business cycle. It’s exactly what the ARRA planners had told the politicians to promise, too. Make no mistake about this; again, it’s in the name itself.

And referring to each “different type of stimulus”, the Philly research authors (who really are trying to find meaningful evidence) suggest exactly that, though not that it makes any profound difference in economic contribution. This is what I, and they, mean:

They found that for the 20 months between February 2009 and October 2010, about $100,000 in stimulus spending was needed to create one additional job. They also found that the impact on employment differs by type of program. Spending supporting low-income households created 2.5 jobs per $100,000 spent, a cost per job of $40,000.

Dan Wilson also found moderate effects associated with Recovery Act spending at the state level. Because the stimulus funding a state received may depend on its economic conditions, Wilson looked at stimulus spending in 2009 that was allocated to states according to statutory formulas such as the miles of federal highway lanes in a state or the proportion of young people in a state’s population. His estimates indicated that an additional $1 million in stimulus funds to a state led to only about eight new jobs a year. The implied cost was about $125,000 per job. Put another way: Because the median family income in the U.S. was just under $50,000 in 2010, the federal government presumably paid more than twice the typical wage for each job it created.

Because of this, Economists have been left to argue over ghostly spillovers, the contentious idea that the ARRA spending in one state led to the expensive creation of minimal jobs within that state, but also perhaps another or even several in a nearby state which wouldn’t have been officially attributed to it. The numbers, therefore, slightly less pitiful than stated above.

The American people don’t care how many angels can stand on the point of a pin.

Interesting scholarship, perhaps. Useful? Not remotely. Especially considering the actual question everyone is really asking. How many spillover jobs were there? Who cares!!!

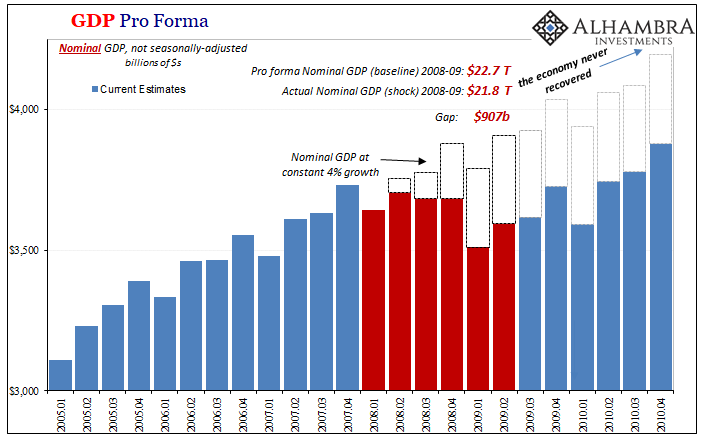

To get at this another way, let’s pick up where I left off yesterday examining the size of the hole produced by what’s been called the Great “Recession.”

To begin with, my 4% assumption was being entirely too kind to the economy, the government, and the Federal Reserve – all the major players involved in the downturn and its purported “rescue.”

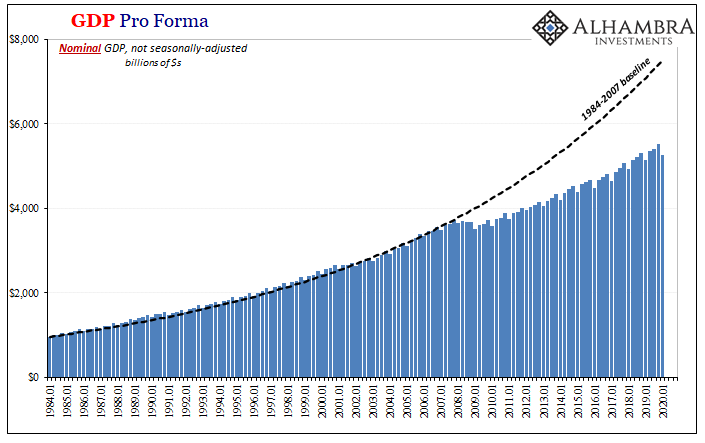

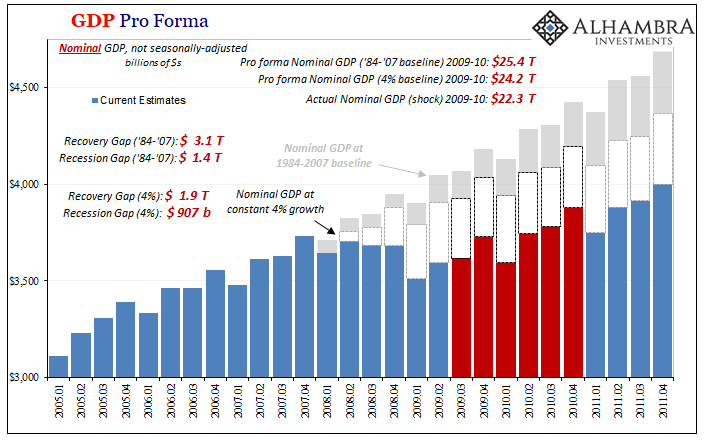

Going back historically, and I’ll use 1984 as a starting point (far enough after the Great Inflation so as to be free from those impacts in nominal output), the baseline growth rate works out to nearly 6%. Huge difference, as you’ll see.

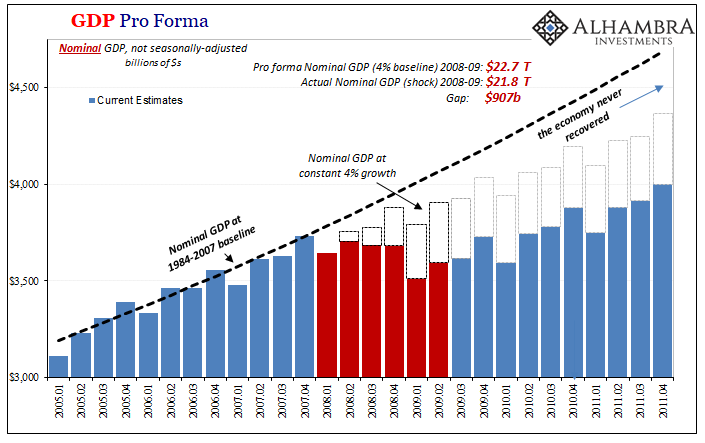

Recalculating the recession gap (defined as the 6 quarters contained within the NBER’s official declaration), it was probably more realistic at the $1.4 trillion shown above rather than the $900 billion I came up with at that 4% nominal baseline growth.

But what we want to know is whether or not the ARRA plus QE and ZIRP (and all the other Fed “liquidity” programs) helped establish and maintain a recovery. To do that, we’ve got to calculate the economy’s overall performance during the next phase.

Moving 6 quarters further ahead, the results work out this way:

Whether you think the 4% baseline appropriate or the existing historical growth rate, it doesn’t actually matter. In both cases, the gap widens during the first part of the recovery; in fact, it more than doubles for each!

Think about what that means; the US economy lost somewhere between ~$900 billion and ~$1.4 trillion in output during the biggest contraction since the Great Depression. And then, over the next year and a half when growth was supposed to be at its absolute peak, rip roaring ahead because of both “V” shape mechanics of the business cycle as well as claims made on behalf of the ARRA and Ben Bernanke, the size of the economic hole doubled.

We fell farther behind over the first six quarters of what was called recovery than we had during the contraction itself.

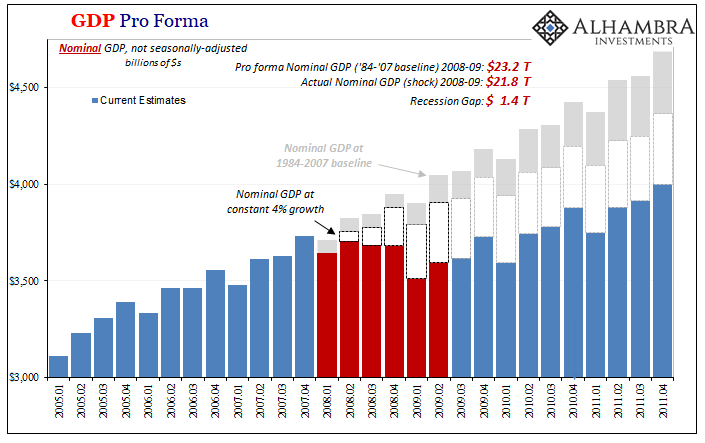

Worse, these things are cumulative; the economy “lost” $900 billion (4% scenario) during the Great “Recession” and then another $1.9 trillion during the first year and a half of its rebound – for a total accumulated deficit of nearly $3 trillion ($4.5 trillion by the ’84-’07 baseline) in economic activity that “would” have happened but never did because of whatever it was that caused this thing.

I care not one bit about cross-state spillovers and/or the number of jobs saved. No one has ever accounted for this, not even the R* idiots (they pick up their story a little bit later in the “recovery”). This is all about the 2008-09 contraction which was…something about a few billion in subprime mortgages?

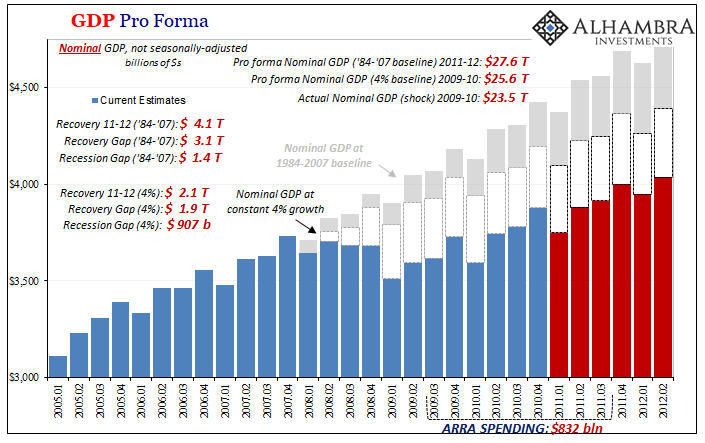

To further establish this point, we’ll move forward another 6 quarters into the second phase of the “recovery” – which ends up at the doorstep of a near recession associated with Euro$ #2, a second monetary crisis (global dollar shortage) which “unexpectedly” materialized in 2011.

As before, the size of the economic hole only widens further, even though by the end of fiscal 2011 the overwhelming majority of the ARRA spending had taken place (as well as two full QE’s and by then several years of ZIRP). The more time, the bigger the hole! That’s the opposite of how the business cycle is supposed to play out. Even weak recoveries narrow the gap at some point.

They’ve never put forward an explanation for why this time was, in fact, very, very different. And why that difference in economy began during 2008-09.

The plain and exposed simple truth is that there never was any recovery – not even minimal. It didn’t matter how much the government wasted in spending or how much arrogance Ben Bernanke put into his magic tricks. What was left for the US economy, like the rest of the world (huge clue #2), was this massive economic deficit which has only grown larger with time. Economic activity that cumulatively didn’t happen no matter what authorities tried on an absolutely epic scale.

And that was before COVID-19.

It doesn’t bode well for all those in 2020 anticipating a “V”, especially with a GFC2 having already broken out recently.

Now, the Republican Economists who derided the ARRA will today claim the CARES Act is different (and they mean other than the much larger numbers). At the same time, the Democrat Economists who heralded Obama’s stimulus will completely trash Trump’s.

Neither of them ever account for the hole itself. And you can’t spell HOLE without the “L” which just so happened to first show up during what more than coincidently happened to be a global monetary crisis. Maybe that part comes first before evaluating cross-border spillovers and jobs saved?

In the context of both today’s and yesterday’s analysis, the CARES Act is already very likely insufficient compared to the economic hole in 2020 even giving it a dollar for dollar credit. But then historical experience proves, as we’ve seen today, that’s way, way too charitable an interpretation; leaving us way short in both dimensions.

What we might better expect by some point next year is yet more debate among Economists about more angels and more pins. The fact that they won’t answer the simple question is already your answer.

Stay In Touch