This seems an opportune time to review the difference between Strategy and Tactics.

Strategy and tactics are how we achieve our goals and objectives. In our specific case, the goals and objectives are financial in nature. Strategy is the path we will take to get from where we are today to where we want to be tomorrow; it is the big picture plan. In investing strategy is your asset allocation target, how you will allocate your resources across various asset classes to achieve the returns you need to meet your goals. Tactics are specifically and tangibly how we implement the strategy.

Strategy and tactics are often described and differentiated as long term and short term but that isn’t really accurate. The choices we must make on how to fulfill our strategic asset allocation – which investments we choose for each asset class – are tactical and long term. For instance, our strategic allocation – the Fortress portfolio – uses the S&P 500 for large company stock exposure. That is a tactical decision that is long term. We make similar choices when constructing international or global versions of the Fortress.

The other kind of tactical change, which is short term by nature, is one that changes the investments within the strategic allocation. These are the types of changes we make to our Citadel portfolios. We might observe conditions that are favorable to non-US stocks and decide to shift some of our large company stock exposure to Europe or Japan. Those types of tactical changes will last as long as the conditions that precipitated them persist which could be months or years.

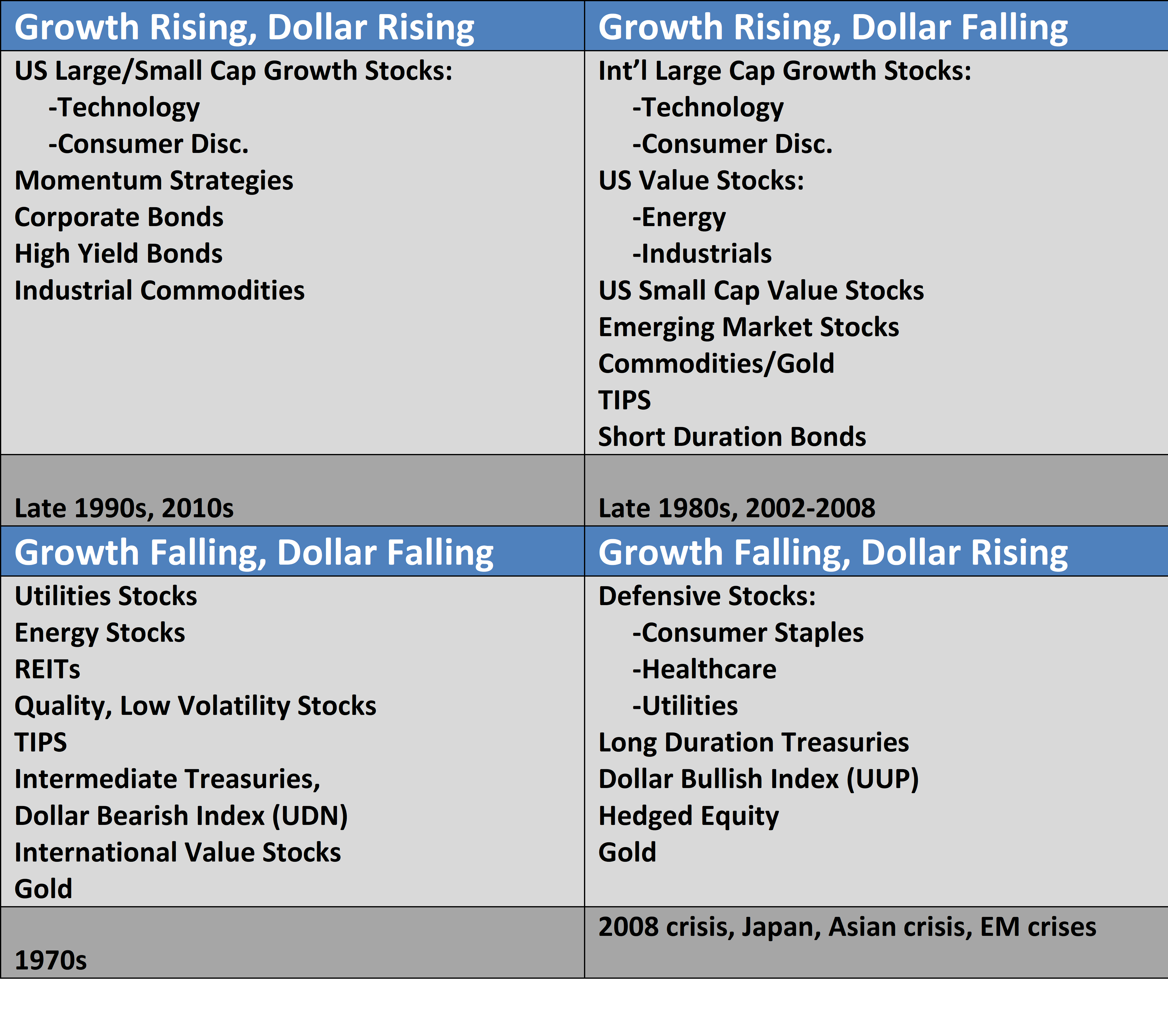

Our tactical changes start with identifying the investing environment. We do this by classifying economic growth as positive or negative (we also consider the rate of change as best it can be determined) and the US dollar as rising or falling. We have identified investments that tend to perform well in each of four distinct environments (emphasis on tend).

US Dollar

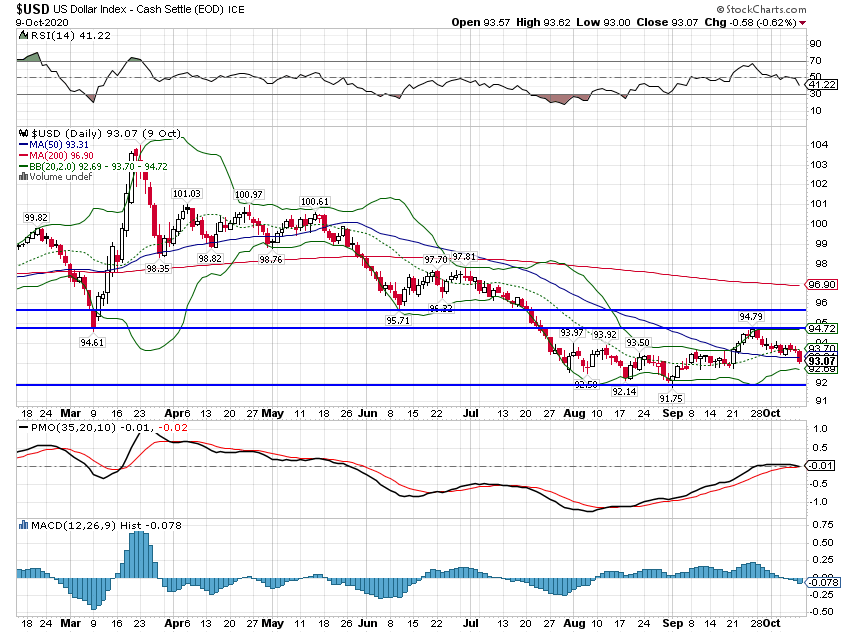

The US dollar remains in a short term downtrend however the rate of change has stalled over the last two months. There was a brief rally in September but it didn’t carry far and the index has recently pulled back.

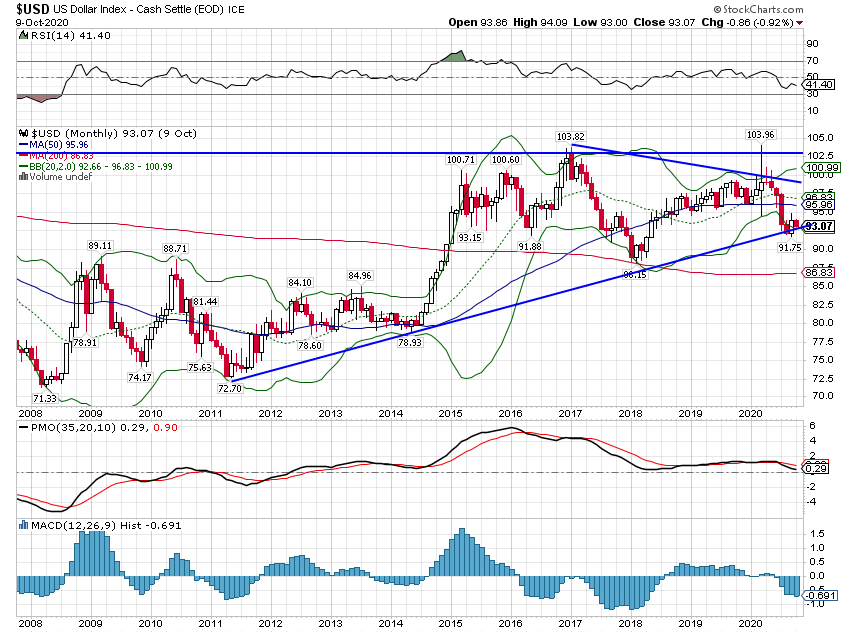

The longer term picture shows the dollar still in the range of the last five years. It now sits on the uptrend line that starts way back in 2011. While I don’t put a lot of emphasis on technical analysis, a lot of currency traders do, so if we break that trend decisively, expect more selling.

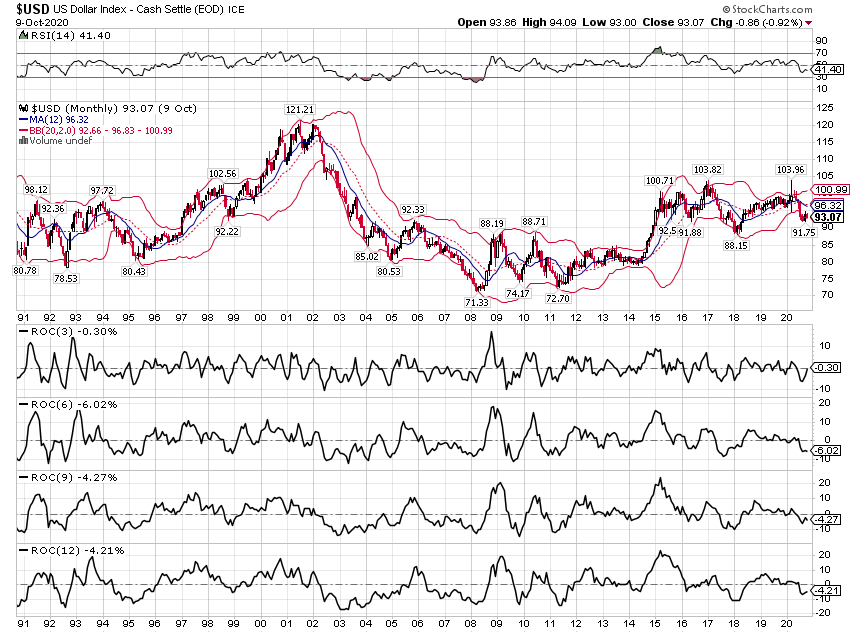

The rate of change on the Dollar index is negative over 3,6,9 and 12 months. For that matter, the change over 1,2,3,4 and 5 years is negative, if only slightly. The short term trend is obviously down.

What does all this add up to for the dollar direction? Not much in my opinion. For now, I’d still call the short term direction down but the downtrend has certainly moderated. If you take intermediate to be 5 years then the trend is neither up nor down. Long term? Well, let’s just say it is stronger than it was around the crisis in 2008.

Now it is true that the dollar is quite a bit stronger against some of the emerging market currencies. And while some of those have recovered most or all of their losses from last spring, some have not. Although most have rallied since their nadir in March, every currency in Latin America is down significantly against the dollar over the last five years. Some Asian currencies have acted similarly although it isn’t nearly as uniform. Countries like Singapore, Taiwan, Korea, Malaysia and Thailand have done a good job of managing their currencies. India, Indonesia and the Philippines have not.

It is tempting to dismiss the weak currencies as outliers that don’t matter much but anyone who’s been doing this as long as I have (that would be measured in decades) knows that EM currency crises are rarely confined to emerging markets. Not every emerging market currency devaluation sets off a global crisis but it happens way too frequently to ignore. So, we will remain vigilant about the places we see weakness while being thankful the list is fairly short at present.

Economic Growth

I wrote a Macro update a few weeks ago and not a lot has changed in that time. The economy continues to recover from the COVID shutdowns but the rate of change is slowing. It is, however, still a positive trend and so the economic growth aspect of our environment is positive.

The slowing of the recovery is neatly captured by the Chicago Fed National Activity index which fell back to just 0.79 in August. That is still above 0 which represents trend growth but not by much.

Chicago Fed National Activity Index data by YCharts

Overall, I continue to classify the current environment as falling dollar, rising growth. It is important to note though that I don’t have a lot of conviction about either of those. The dollar bear camp isn’t exactly a lonely place and we have an election coming up that could have a pretty big impact on future economic growth. The situation is so confused right now that even if I knew the outcome of the election in advance, I’m not sure I could say how markets would react.

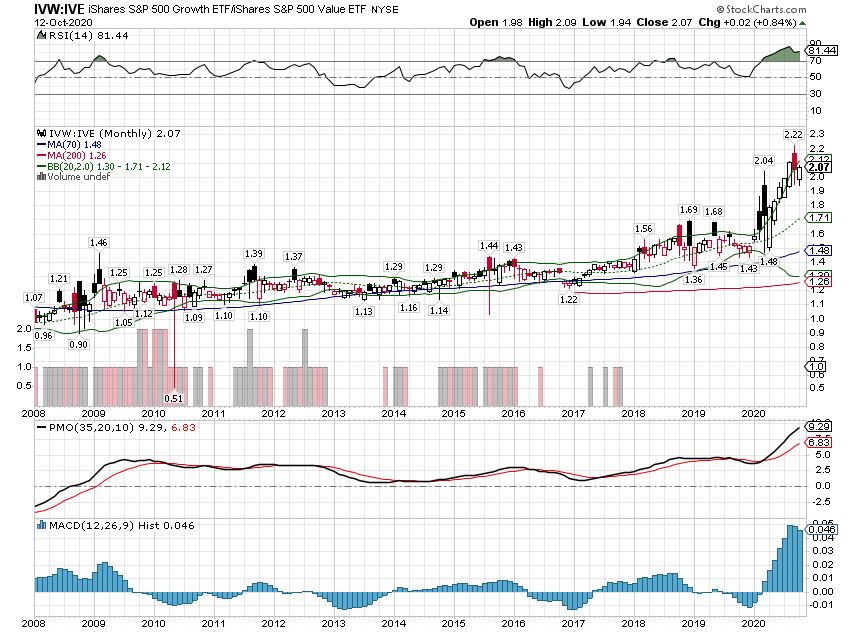

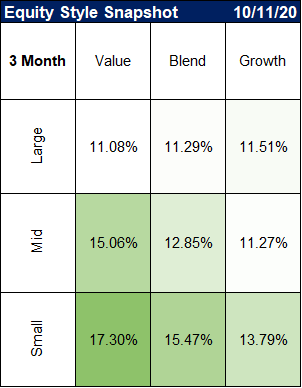

Style Trends

Growth continues to outperform but the tide may be turning. Growth’s outperformance reached such an extreme recently that a bounce back by value is almost inevitable. The last three months shows the beginning of the shift but mostly in the small and mid cap areas. But large value holding its own against large growth over the last quarter is news all by itself.

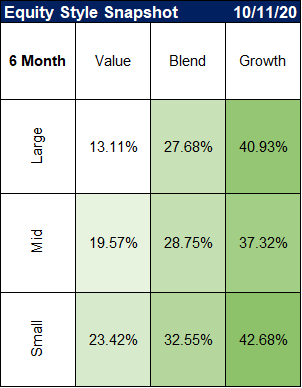

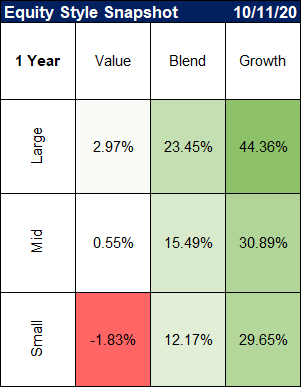

The long term trends are still dominated by growth by a degree not seen since the dot com bubble of the late 90s. Value tends to outperform in weak dollar environments but the crowd isn’t going to switch to value until staying with growth becomes painful. For a full shift, we probably need to see a more defined downtrend in the dollar. In the meantime, a rebound in value to the downtrend line seems likely and that is a reversion worth trying to capture.

Tactical positioning: We are overweight value vs growth in an attempt to capture the reversion to the old trend.

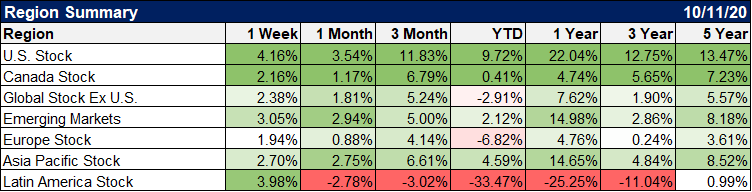

Regional Summary

A weak dollar environment should, theoretically, favor international over US stocks. While European and EM stocks have outperformed slightly since the bottom in late March, the trend still favors US stocks over most time frames. EM stocks have performed well over the last year but are still lagging US stocks by over 7%. The only way this is going to change for anything other than a brief time is if the dollar gets in a more sustained downtrend. For now that just isn’t happening and most investors are sticking with what has worked for so long – US.

Tactical Positioning: We have added European and EM stocks to the portfolio. In addition, we hold a long term investment in a concentrated Japan fund.

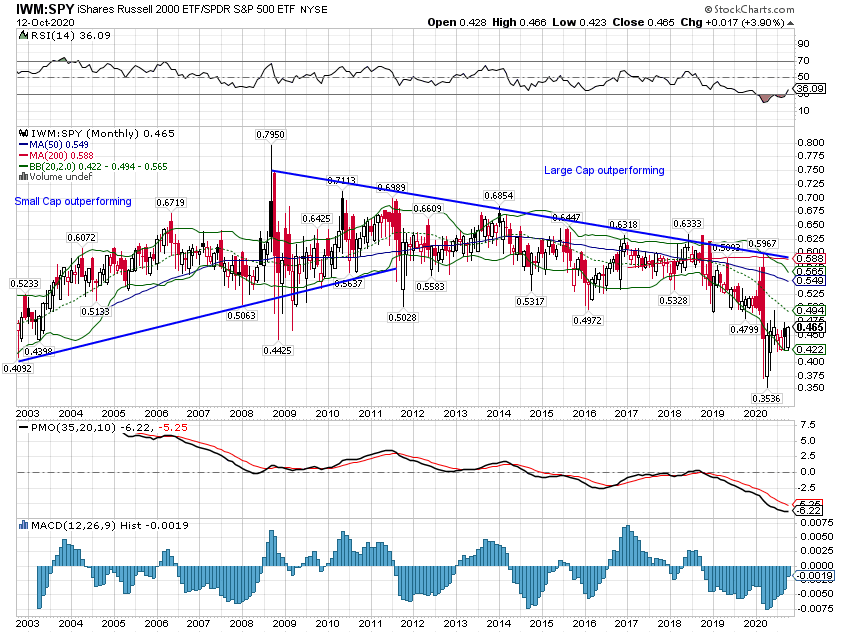

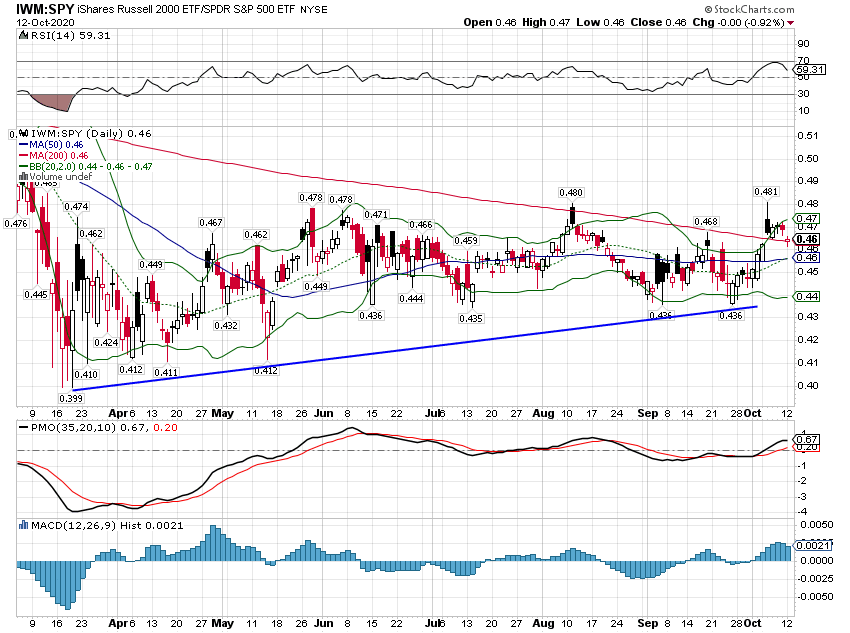

Large Company vs Small Company

Small company stocks are one of the few areas where we see some of the recent extreme being corrected. Small stocks are in an uptrend vs large company stocks since the March lows and the recent outperformance is pretty strong.

Tactical Positioning: We are overweight small company stocks versus our strategic allocation.

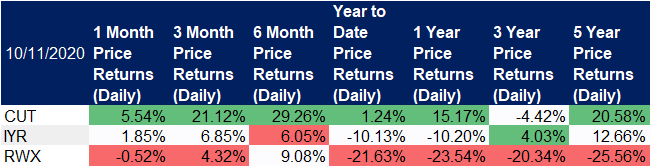

Real Estate

Timber REITs have been outperforming for quite some time. We sold our timber position a few months ago when lumber prices moved over $550. Unfortunately for us, that turned out to be a mere pause before moving to $800. Now prices are back to $400, an incredible round trip that took a mere 4 months. Unfortunately, the timber REITs did not fall along with the price of lumber so we are out of the strongest sector of the REIT market and reluctant to get back in. This happens at times and a choice must be made to either get back in or move on to another theme. We have chosen the latter as lumber supply appears to have caught up with housing demand.

International real estate has been the big underperformer but with the dollar turning down we think the recent outperformance will continue. We continue to hold the DJ REIT index ETF as a core position.

Tactical Positioning

We are overweight REITs vs our strategic allocation and have initiated a position in international real estate.

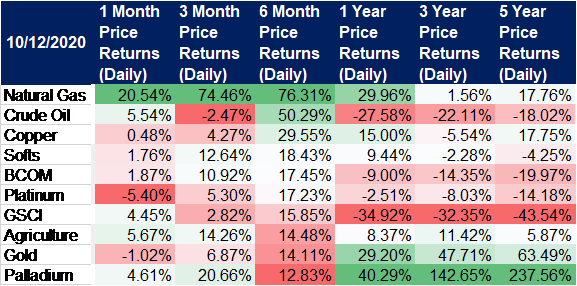

Commodities

Gold returns are fading as the economic recovery continues. Gold’s performance versus stocks peaked with the bottom in stocks in late March. The general commodity indexes are going in the opposite direction with the BCOM recently outperforming. Crude oil and copper are also improving but the big surprise is natural gas which has risen strongly off multi-year lows.

Tactical Positioning: We have equal weight positions in gold and general commodities but that may change soon. If the economic recovery continues and real rates rise, gold will continue to underperform both stocks and general commodities. We are also overweight BCOM vs our strategic allocation.

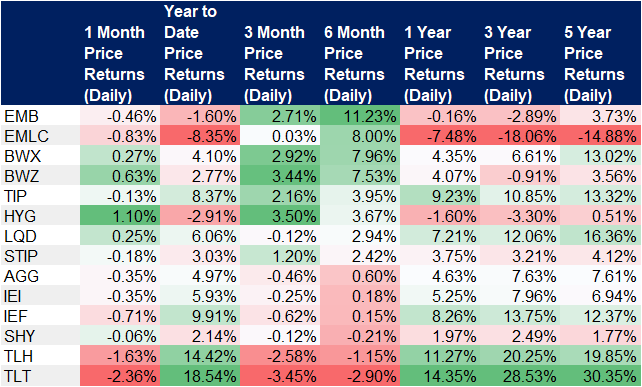

Bonds

Bonds have been going nowhere fast for the last 6 ½ months with the 10 year Treasury yield stuck between about 50 and 80 basis points. Since the beginning of August nominal and real rates have both trended higher. The move in the 10 year yield is roughly 50% in that time which seems significant but when your starting point is 50 basis points, it really doesn’t mean a whole lot. Nevertheless, the move is higher which supports the view that the economy is improving however slowly.

In fixed income one generally has to choose what kind of risk to take – duration or credit. In the current environment where the economy is improving, credit risk seems the logical choice. I would caution however that the current environment is quite uncertain and while some credit risk is warranted it should be high quality and limited. Our default fixed income investment is the 3-7 year Treasury index and in an uncertain growth environment that seems a fairly comfortable place to be – some duration risk but not a big bet on a double dip and deflation.

Tactical Positioning

We still have the majority of our fixed income portfolio in the Fortress allocation to the 3-7 year Treasury index. We also have had an allocation to TIPS for several years and that hasn’t changed. We have recently added some short term investment grade corporate bonds. It isn’t a big risk in our opinion and provides a little better yield than Treasuries.

Conclusion

There is an extreme amount of uncertainty right now. Part of that is due to the upcoming election although I would argue that isn’t as important for the economy as most people think. If Biden wins the White House and the Republicans retain the Senate – which seems to be the emerging consensus – we shouldn’t see much change in economy policy. A Biden administration would certainly change the conversation but getting a tax hike through a Republican Senate seems unlikely. There would be changes in the administrative/regulatory framework and that could affect certain industries but lobbyists are not going to abandon DC anytime soon so the damage would likely be mitigated. Even if there is a Democratic sweep – which was the consensus until a few days ago – policy changes are still likely to be fairly small if in the “wrong” direction.

But the uncertainty extends further than just the election. We still don’t know the long term implications of COVID-19. Will there be a winter surge? Will we get a vaccine any time soon? What about treatments? Will the virus eventually die out? How will the virus interact with the normal flu season? How long until we can go back to our normal activities, if ever? What industries will be permanently changed by the virus and how will they adapt? How will the economy evolve and adapt to the virus? What new opportunities and businesses – maybe whole industries – will emerge in the wake of the virus?

A friend who lives in China recently told me that life there is essentially back to normal. Movie theatres and restaurants are full and people are going about their lives as they did before. There is no guarantee that it stays that way of course but it does give me hope that we’ll be back to normal soon too.

Joe Calhoun

Stay In Touch