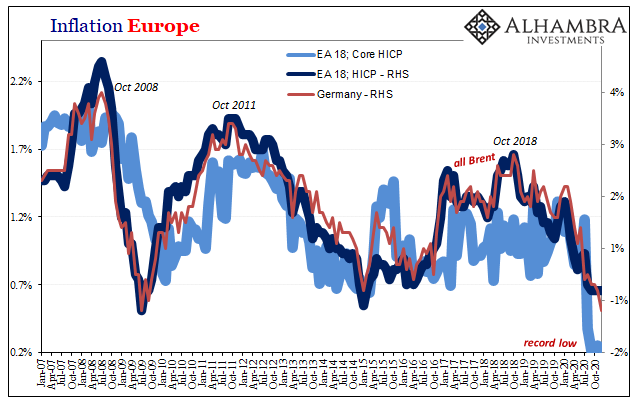

Sticking with Europe, central bankers want and expect higher inflation because that would confirm an economy strong enough – and monetarily sufficed – to sustain success. It’s the sustainability which has been lacking; the global economy since the first global (euro)dollar shortage never able to do more than lurch between downturns and the absence of downturns (reflation).

Without enough monetary oxygen flowing around the world, the global economy just could never get going enough to hit liftoff velocity, producing the inflationary pressures as the factor byproduct of having achieved this. That’s why central bankers around the world have been lustily waiting for consumer prices, as well as why they’ve been so overeager to declare success, in order to signal back to them how monetary policies must have finally worked.

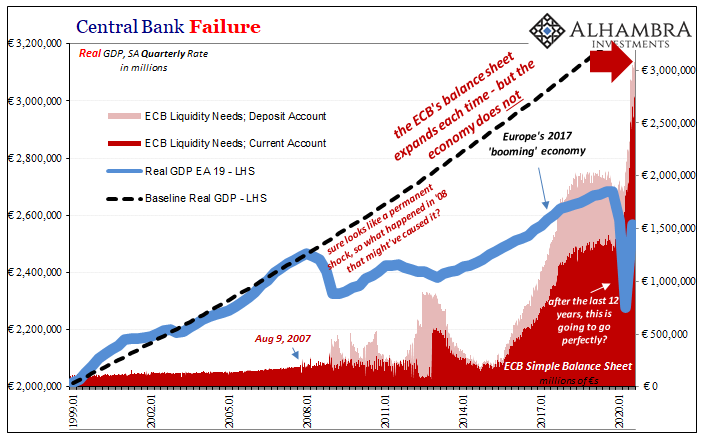

They never have, therefore only disinflation punctuated by bond yields moved lower and lower with no need for the several types of QE’s. In fact, lower yields demonstrate QE’s irrelevance, at best, and more often than not the market’s total disbelief in the theory as well as its execution.

Despite this, faith in central banks remains unflinchingly strong in many sectors of the real economy. Maybe the bond market isn’t buying the effectiveness of the bond buying, in places like Germany, but corporate managers – leaning hard on their Economists for guidance – steadfastly hold out hope.

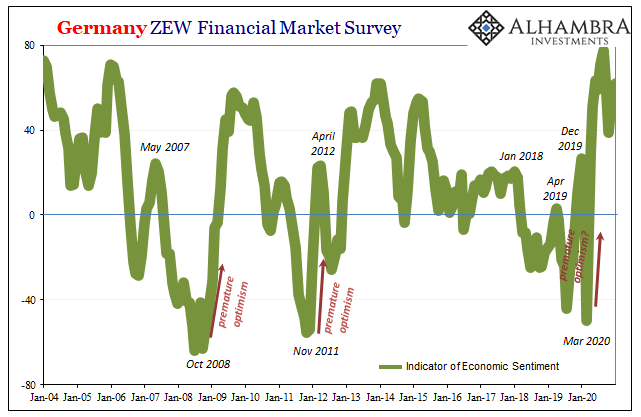

We’ve chronicled the German ZEW for this reason, a pretty conclusive demonstration between “stimulus” as a belief and the lack of stimulation as our reality anyway. Going back to last year, the sentiment portion of this dataset skyrocketed just as it has during similar periods the last dozen years: bad economy producing overactive central banks.

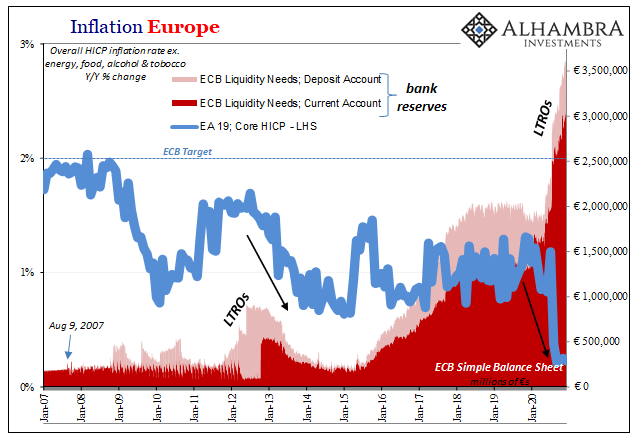

Taking account of the former, it’s simply that we are all taught how monetary policy can overcome any deficit. So powerful according to the textbook, particularly these QE’s, all it takes is mere action. In the ECB’s case, among the largest LSAP’s (or LTRO’s).

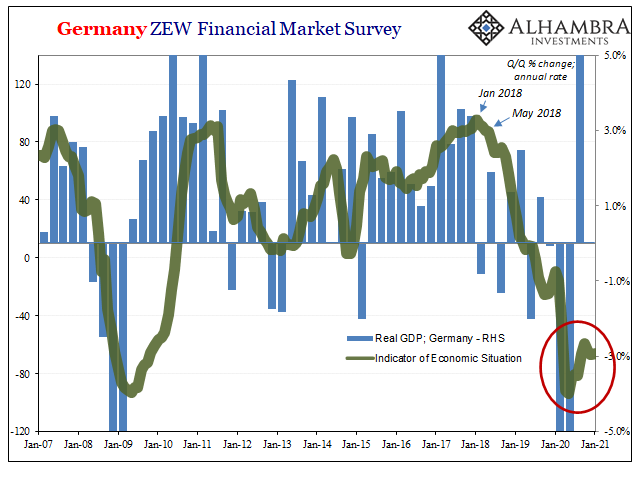

While Europe’s economy is going to stumble and maybe even contract in Q1 2021, ZEW German business sentiment continues to be hugely optimistic regardless. Today is bad, sure, but the future is very bright – at least according to these survey respondents working throughout the outward-facing German economic machine.

That’s why we pay attention to Germany and this ZEW; it’s not really about either, rather both as a close proxy for the global economy as a whole.

These ZEW-ers been optimistic, and at times last year hugely optimistic, from the QE get-go. From a low of -49.5 mid-March, sentiment leapt ahead by 100 pts in a matter of just two months. By September, the reaction had reached a high not seen since the early years of this century. As if 2020 might ever be comparable to the era of global credit bubbles.

But if businesspeople in Germany keep expecting this future so dependably robust, when does it finally matter that it’s not? After all, March is now a long time ago. And while sentiment remains high in the latest estimates for January 2021, again looking out to the future, these same respondents admit today is still atrocious.

Last year, 2020, did not, in fact, reach comparable levels of the pre-crisis age.

That’s ten months of waiting for it – and it’s promised inflationary confirmation. Instead, no signs of either. The ZEW’s current situation index has barely budged from its lowest point. These hugely optimistic Germans must at least appreciate just how misplaced that optimism has been for this long already.

At what point do people, any people, stop looking ahead or at least stop painting whatever optimism they want for tomorrow, realizing how we’re already there. The end of 2020 was first believed to be the promised land, and here we are. At least when looking forward from that initial burst of positivity, the “V” feeling which took over much of the world and not just in Germany, the world begins 2021 with too much that still looks, feels, and is 2020.

So, instead, more the same “stimulus” but this time it’ll work? Just give it enough time?

It’s not YCC which has kept yields relatively low, and the economy locked into the shape of another “L.” It’s the bond market looking back on Japan’s experience and shaking its collective head over how ill-advised it has been to follow it. These Japanese pioneers were a warning, a straight-forward cautionary tale for what not to do.

That mountain of evidence has never been entered into the court of public opinion.

So, tomorrow is always the best of times even when it becomes today and it never is. Like the inflation always promised, the growth it’s supposed to come from is always future tense even when the future is already today.

Stay In Touch