The Bureau of Labor Statistics (BLS) estimates that in the month of March 2021 somewhere around 916,000 payrolls were added back to the economy. I have to disclaim the figure simply because the statistics used to create it aren’t really all that precise; piecing together data from a survey of 145,000 business establishments, a fraction of the economy’s total, the government comes up with a 90% (only 90%) confidence interval that’s a few hundred thousand in breadth.

In other words, what the BLS is actually saying about last month is that if it was to resample the same survey respondents 100 times, in 90 of them the agency expects the monthly change for March would come out to somewhere between 803,700 and 1,028,300. It’s hardly the definitive economic accounting thrown around haphazardly each monthly Payroll Friday.

Whether 800k or a million, or anywhere in between, there’s really not much difference since any number within that range is gigantic; the last few months have seen, in every likelihood, a sizable pickup in the labor market rebound.

But while we can be reasonably confident in the BLS’s statistical processing to reach such a conclusion, questions remain about just how much. Very simply, jobless claims.

Back above 700,000 in the latest weekly data, the Department of Labor (DOL) tallied an astounding 2.876 million initial jobless claims filed collectively in March with all the state unemployment insurance agencies. Before last year, those four weeks together would have easily added up to a record amount.

It might seem improbable, then, how March could on the one hand end up so awesome yet on the other so continually terrible; that nearly a million net jobs were added when for the same month this number of unemployment claims (remember, these are “initial” meaning an entirely new layoff, furlough, or some other involuntary separation with each one) could have still been so ungodly huge.

Is it plausible to believe that almost 3 million jobs were destroyed or somehow disappeared but then nearly 4 million others must have been either created or, more likely, taken out of mothballs from their previous COVID hibernation?

Yes. Sort of.

To see what I mean, let’s check some other numbers. We’ll try to repurpose similar data in order to verify the BLS findings – beginning with other BLS data. In this case, JOLTS (estimates for February 2021 released today, one month behind CES).

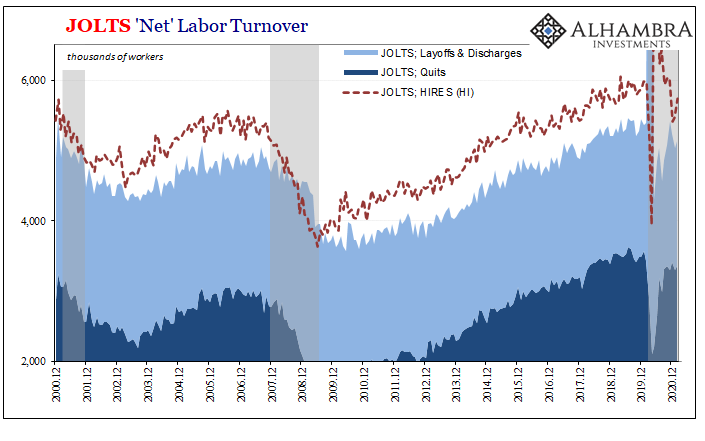

As the name indicates, Jobs Openings Labor Turnover Survey, the BLS here comes at the labor market from a different perspective. There’s an enormous and perhaps unappreciated level of turnover or churn in any given month; sizable gray area for all sorts of statistical complications and trip-ups in analysis. Our difficulties, like in jobless claims, are in how to measure it such that we can interpret meaningful changes or conditions.

For example, before March 2020 the JOLTS figures showed that last February just less than 6 million workers had been hired (HI) by employers across the economy. In that same month, the DOL puts initial jobless claims (jobs destroyed) at just over a million. Meanwhile, the CES data said net payroll expansion was (revised) +289,000.

That’s a lot of churn.

If we start with JOLTS HI – raw or gross jobs gained – then subtract JOLTS figures on layoffs and discharges as well as voluntary quits (separations), we come up with a plausible net change in the labor market’s scale. It stands to reason that if there ends up being more hired than laid off, discharged, or resigned, the overall employment condition likely had at least improved.

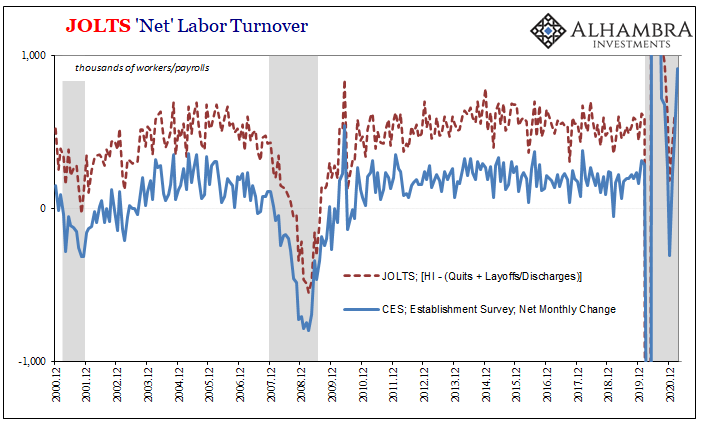

And when you take that net from JOLTS and measure it against the payroll figures it becomes clear they are very similar. In one sense, that’s expected given how JOLTS itself is benchmarked against CES numbers (and remember, CES estimates are benchmarked every year against, believe it or not, unemployment insurance payment data!), but still the consistency is compelling.

However, as you can see, generally speaking there’s quite a lot more net hiring going on in any (every) month than payrolls gained. It amounts to an unfilled statistical gap, an indetermined amount of monthly turnover.

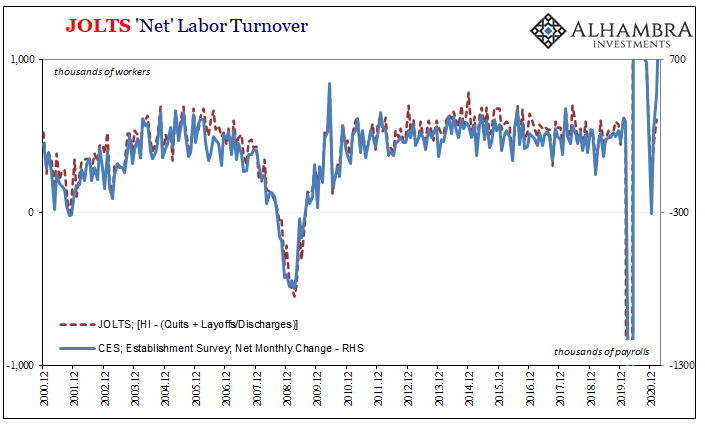

When accounting for it in raw numbers, JOLTS and CES (+300k) come out very close:

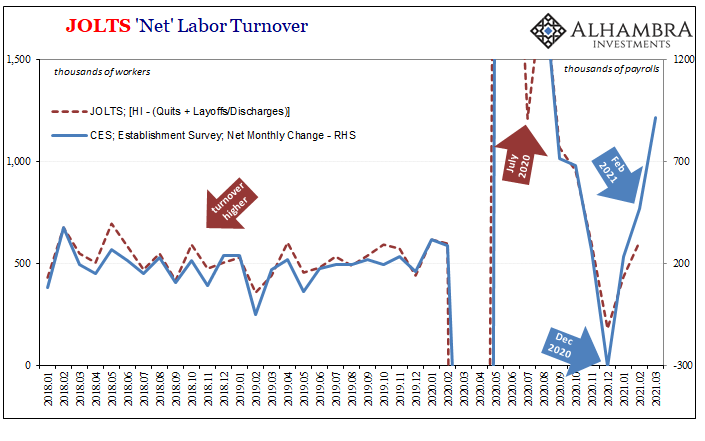

More recently, there have been a few more significant discrepancies. In both charts above, you see how the red dashed line (JOLTS net) typically remains slightly elevated when compared to the blue (CES) even after our 300k plug. But in February 2021, the CES jumped much higher than supported by the latest JOLTS (and then went higher still in March, up near 1mm; we’ll have to wait until next month to see if JOLTS moved in the same way).

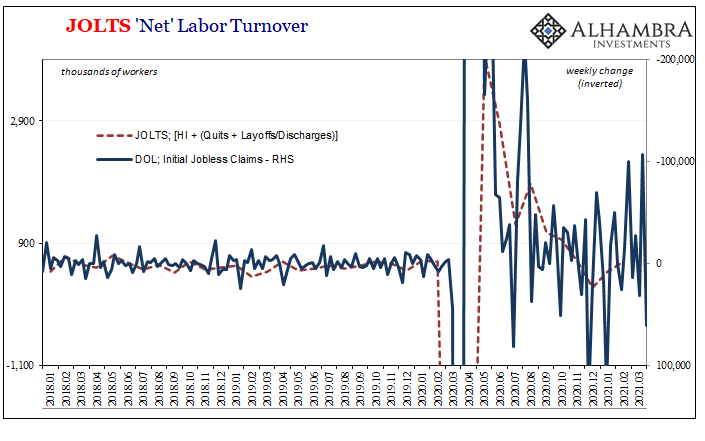

Next, let’s take a look at where (and how) jobless claims fit:

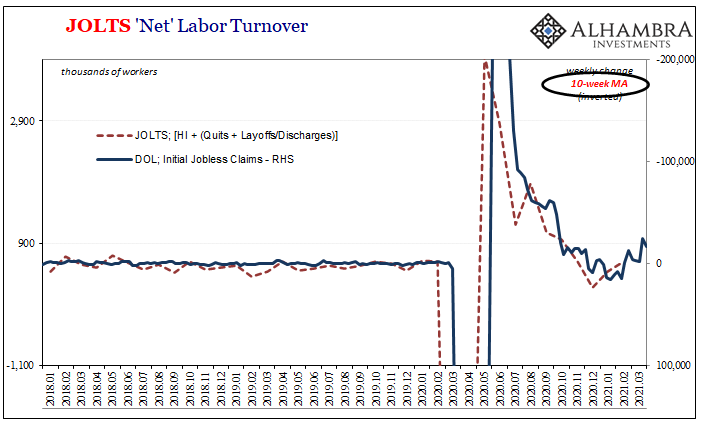

Since unemployment claims only deal with direct job destruction, it isn’t immediately clear why initial claims estimates (weekly changes) would fit so well with the JOLTS calculations for total net turnover which takes into account jobs gained – but they do, which becomes clear once you convert the raw weekly changes into a moving average (above).

In very broad terms, this close correlation indicates generally similar factors underlying each set of data. For jobless claims, the higher the negative number, meaning greater declines in the weekly totals, we’d expect the labor market overall to be improving which is consistent with higher net JOLTS turnover (more hiring than firing and quitting).

It may be, during these times, that a job loser who might otherwise have gone on unemployment during bad or worsening environments instead straightaway gets hired for a new position at a different company without ever having to file for benefits. Thus, lower claims, higher hiring.

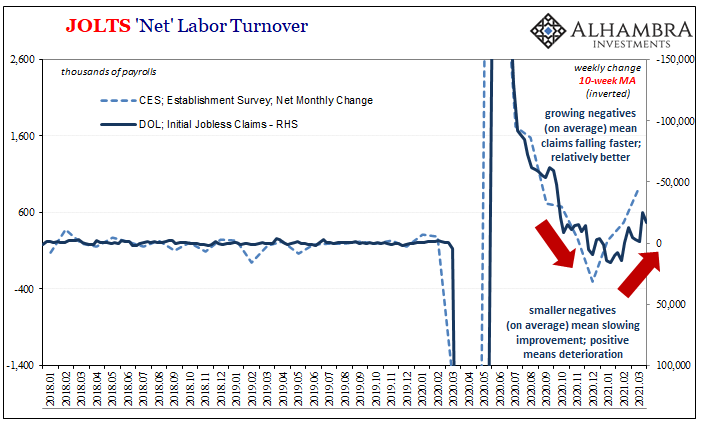

What seems to matter most when comparing jobless claims to JOLTS (or the CES; below) is the relative changes in each set. Given the close relationship between net JOLTS and changes in CES, therefore if average differences in weekly jobless claims correlate with net JOLTS (above) they’ll also correlate broadly with monthly payrolls (below):

Here again, though, it seems as if the payroll data is outpacing corroboration from either JOLTS (one month further behind) or, in this case, jobless claims (regardless of absolute record weekly numbers).

But that’s an issue of precision which, as noted at the outset, these kinds of high frequency figures (CES) are not truly meant to feature. In other words, altogether from each of the three data sets we’re reasonably sure that the labor market slowed down considerably (perhaps dangerously) to end last year; then at some point this year, it began picking up again.

Just how much, that is the real question.

Not just in terms of numbers, estimates, and statistical series, in the very real sense of what this whole thing is supposed to be about; what we are really trying to divine or tease out from all this overflow of numbers is, 1. Whether the economy is rebounding; 2. If so, is it rebounding enough?

While on the surface it may seem as if jobless claims and the Establishment Survey are looking at completely different economies, they aren’t actually as far off as maybe first pictured given their respective results and how those results are changing over time. However, there does remain some level of disagreement as to the degree which imprecise estimates cannot directly solve.

In the end, since we are well aware of the lack of accuracy with any of these series, like when analyzing the unemployment rate (given its misleading recent history) it comes down to appealing to an even broader survey of data and figures to gain a reasonable sense of how it’s all unfolding. The payroll data may be the gold standard for mainstream “analysis”, yet not even the BLS would recommend relying on it over short periods, definitely not month to month.

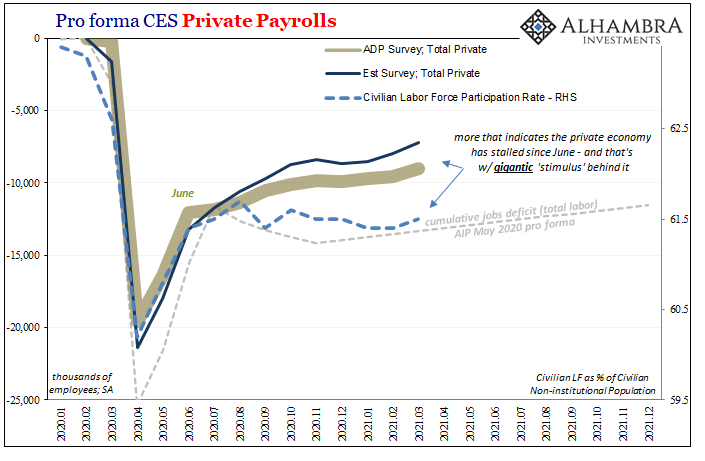

All three of these employment estimates show that the labor market in 2021 is absolutely improving. Two of them (JOLTS, jobless claims) pose serious questions as to whether it is enough. The other (CES) is becoming more of an outlier (at least in February-March 2021), particularly for any sense beyond simple non-economic reopening.

While this doesn’t definitively answer any questions, it does allow us to frame or reframe them in a very helpful way (which may be what’s going on in certain markets of late).

Stay In Touch