We have reached the point of absurdity in the crypto markets. There were people buying Dogecoin last week in anticipation of Elon Musk’s appearance on Saturday Night Live, with the expectation, presumably, that he would say something bullish and they’d be able to ring the cash register. Easy, peasy, cha-ching. Except, well, at last check it didn’t work out that way. Musk at some point in the telecast called Dogecoin a “hustle”, which is derogatory to dances from the disco era but otherwise pretty accurate. Doge promptly did a header over the weekend, although as crazy as that market is I wouldn’t be surprised at all if it was higher by the time you read this. By the way, if, according to Musk, Dogecoin is a hustle, what does that make Musk? Hustler-in-chief? What about Mark Cuban? Both of these celebrity businessmen (and make no mistake, celebrity is the important word in that phrase) have been promoting Dogecoin on social media. Or maybe they’ve just been joking but only people with a net worth that looks like a phone number are in on the joke. My question is this: where are the regulators? Yes, Dogecoin is a joke and Musk may well have been joking all along but real people are going to lose money. Preventing fraudulent investment schemes – and promoting a joke cryptocurrency on social media when you are a major holder goes well beyond “talking your book” in my mind – would seem to be something regulators might find of interest. Alas, the SEC is busy at the moment investigating whether Volkswagen’s April fool’s joke about changing their name to Voltswagen caused any investor harm. As I seem to say every day, you have got to be kidding me. Talk about missing the forest for the trees…..

I happen to believe that crypto/blockchain/DeFi has a bright future. I also happen to believe that bright future is probably much further away than today’s boosters believe. I also believe that the blockchain applications that change the world will likely concern mundane things with the potential to finally move the needle on productivity growth. But I’ve been around the block more than once with “bubbles” or whatever you want to call the thing that happens to new, exciting, and previously unknown assets. I saw it with biotech in the early 90s when anything with bio in the name went up. I saw it in the late 90s when anything with dot com in the name went up. And I saw it again in the mid-00s when real estate in places where no human should want or need to live went up. And we’re seeing it again today when anything that can be vaguely identified with crypto goes up. My approach to all those manias or whatever you want to call them was the same. I waited for the crash and picked through the debris to see what was worth salvaging and took my time buying it. I plan to do exactly the same thing again when all the crypto assets crash. They will and when they do, the good ones will go down with the Doges. And my guess is that the big one hasn’t been created yet, that it will come after the crash. I could be wrong but I’d just remind you that Facebook and a whole bunch of other big winners weren’t around when dot com went splat.

It is also the case that US stocks generally are fairly dear today, if history is any guide. Of course, history might not be a good guide since we really haven’t been here before, in a post-virus recovery with the fiscal and monetary dials turned up to eleventy five. In the latter case, of course, it is just the illusion of easy money or easy money that only ends up in markets or easy money for everyone but me or just the talk of easy money, but in an age when the only thing that matters is the narrative – the meme – monetary policy at least has that lever pushed over to Spinal Tap. The Fed may actually be irrelevant from a practical standpoint but Jerome Powell has the bully pulpit and he’s about as bully as you can get without telling the NY Fed to hire Dave Portnoy and let him buy stonks.

What is interesting about the new age of big government is that so far it has only succeeded in getting the economy on a track that takes it back to where it was, a place of 2% growth in which the many weren’t nearly as happy as the few. And there is a pretty good argument that where we’re headed isn’t as good as the place we left a year ago. The bond market is not, as Ben Bernanke might say, a conundrum. The economy is certainly re-opening and the recovery continues apace despite the big miss in payrolls last week – more on that later – but long term bonds, nominal and real, are telling us that the long term outlook is not that great. The difference in the yield on the 10-year Treasury note today versus where it was just prior to the shutdowns last year is negligible and 10-year TIPS yields are quite a bit lower. I wouldn’t be surprised if yields go higher in the coming months but I also expect yields to peak at a rate less than the last peak of 3.25%. How much less will probably depend on how long this expansion lasts. By the way, the debate I’ve been hearing about whether last year’s downdraft was a bear market or whether this is just an extension of the previous bull is, well bull. We had a recession, people. And I’m pretty damn sure we would have had one without a pandemic. Everyone seems to forget that we had already had an inverted yield curve and the economy was already slowing before our politicians decided to shut everything down and remove any doubt about whether a recession was coming. So, bull market, bear market, who cares? It’s a new economic cycle and we’re on the way up. The only question that really matters is how high will the peak be and how long will it last?

There is always a lot we don’t know. We don’t know what kind of negative shock might come along and push this fragile economy right back into recession. We don’t know what innovation might come along that raises productivity growth back to where it was in the late 90s and GDP growth well above the plodding of the last cycle. All we can do is take things as they come, make sure we are well informed, especially about technology, and respond to what the market tells us. Right now we seem to be getting mixed signals with stocks and commodities throwing a block party and bonds shouting at all the bulls to get off his lawn. I’m not so sure the message is that mixed though. Stocks are responding to expectations about corporate earnings and those are only correlated with economic growth over the very long term. What’s happening with commodities is the intersection of two cycles. We’ve just come through a decade of low and continuously falling commodity prices, not an environment that encourages investment in new capacity. We are also opening a global economy when many of the commodity countries are still struggling with the virus. Lack of supply meets infinite demand and voila, commodity bull market. In other words, bonds may still be right about the long-term picture even if they seem out of step today.

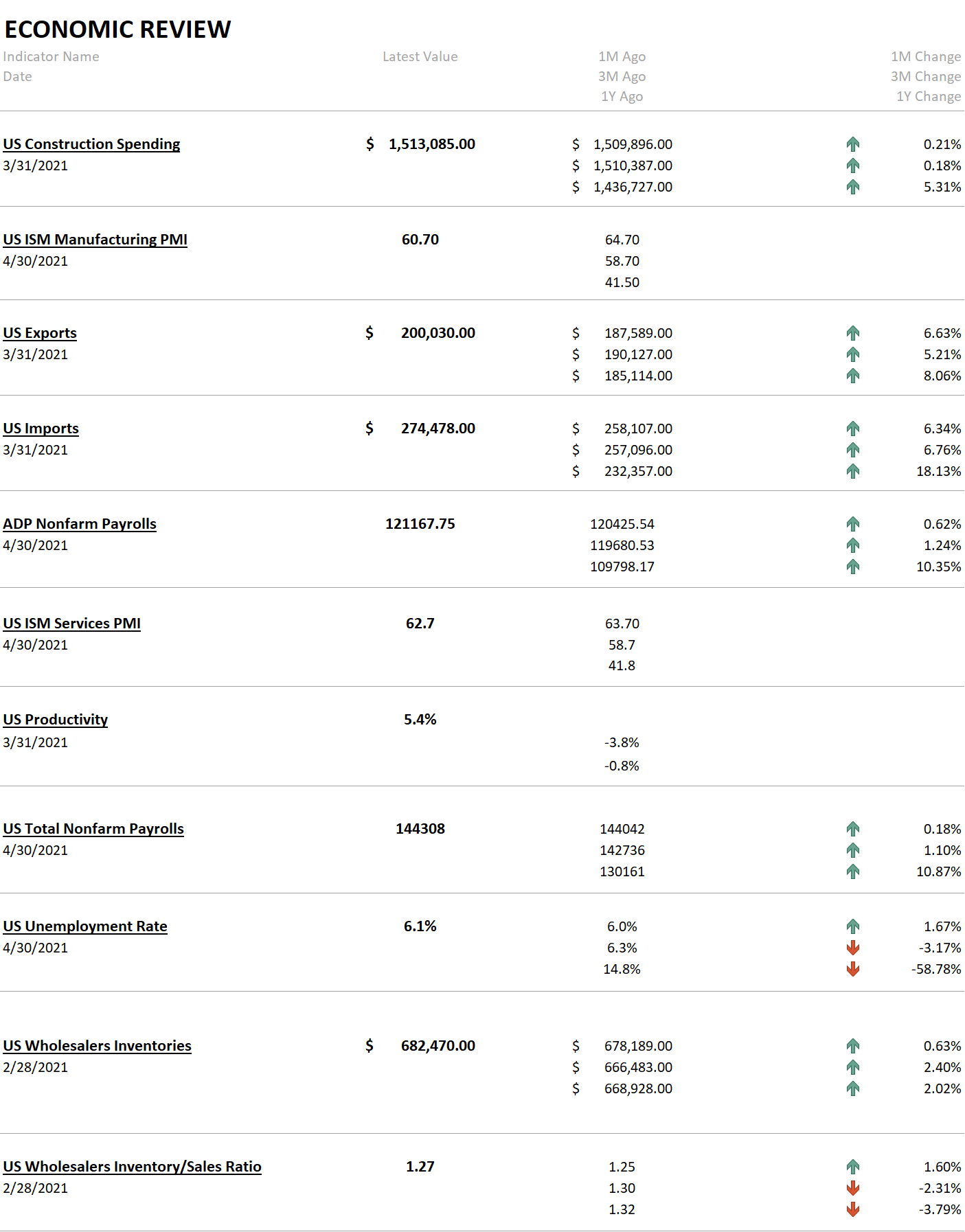

Last week’s big payrolls miss was not the biggest economic news of the week. Yes, it was a lot less than expected but these monthly reports are little more than guesses and not very educated ones at that. By the time the final revision of this number is made no one will care. It may turn out to have been 2 million jobs or it might be a loss but it will be irrelevant by then. Frankly, all that really matters is the sign and they don’t even get that right all the time. But I digress. The most important economic report last week was that US births last year fell 4% to the lowest level since 1979. The birth rate, measured as the number of babies per thousand women ages 15 to 44, is down 19% since peaking in 2007. If you want to know the real impact of the great financial crisis and the ensuing slow growth, that is it in a nutshell. Combine a low birth rate with slower immigration and rising deaths (not just from the pandemic but because we’re getting older) and you get a demographic tsunami that makes more rapid economic growth difficult, to say the least.

The other reports last week were pretty good, although the ISMs seem to point to a peak in the growth rate of the re-opening phase. That is not, I think, due to a lack of demand but rather a lack of supply. There are shortages across the global economy that don’t look likely to be resolved quickly. The semiconductor shortage is particularly vexing and affects a wide range of industries. Light vehicle sales ran at an 18.5 million annual rate in April but I doubt that can be maintained. Ford, just as one example, said in their quarterly call that production would be cut in half in the next quarter due to chip shortages. We are seeing layoffs from multiple auto companies that are shutting down production lines because they can’t get parts. Most observers are blaming this on COVID, but I suspect more than a little of our current problem with chips is a result of our turn toward protectionism and nationalism. I’ll write more on that in the future but I will say here that the most distressing part of the new administration’s approach to the economy is not their penchant for taxing and spending but rather their embrace of the Trump administration’s trade policies. In short, the Chinese have us by our supply lines and I suspect they are yanking pretty hard right now.

I hope I’m wrong about that but regardless, the economy is continuing its recovery if at a more subdued, supply-limited pace. That could, I suppose, be a good thing if it prolongs the recovery and expansion. I’d rather have 4 quarters of 3 or 4% growth than one of 12% and then a rapid fall back to trend growth.

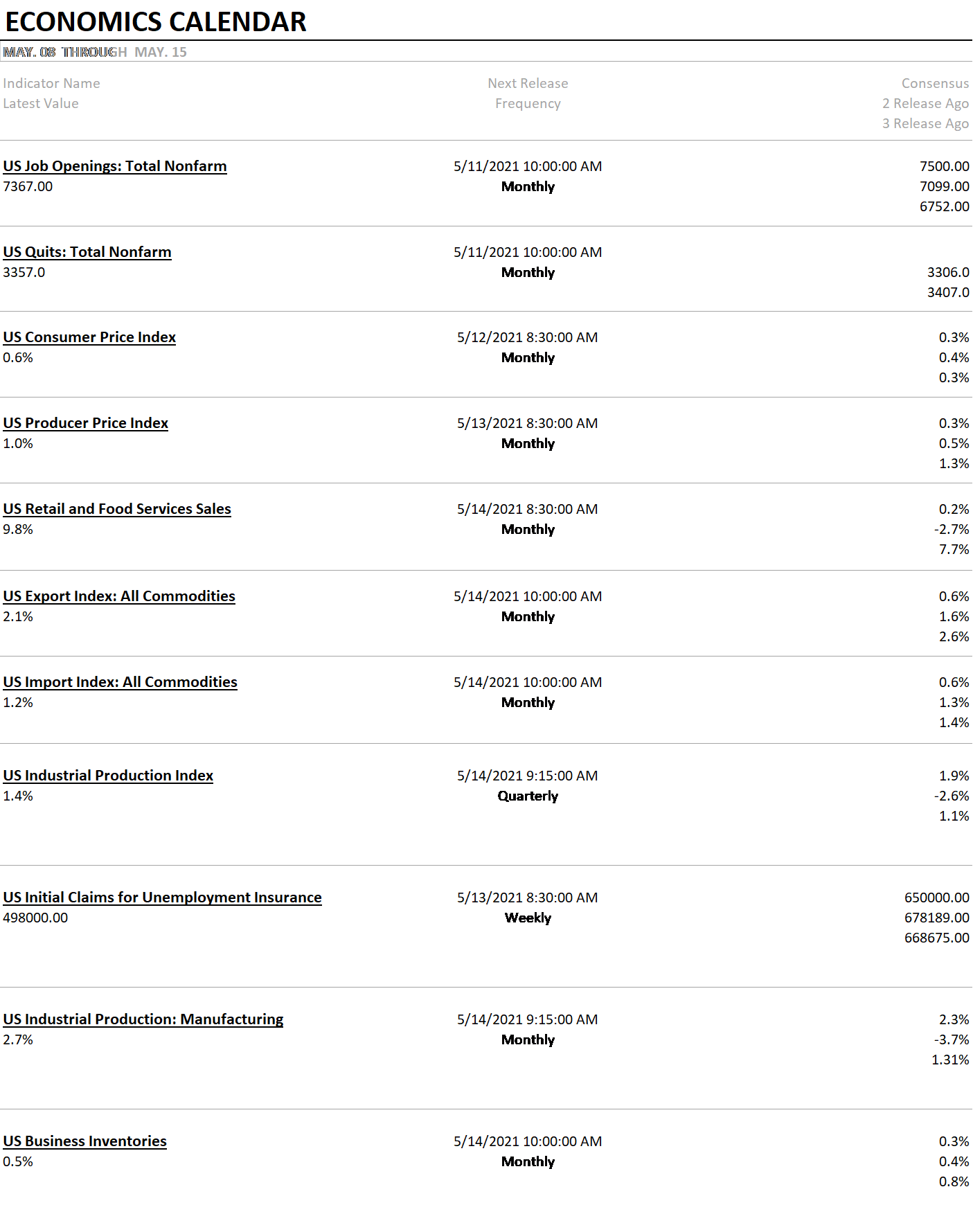

Next week we get the JOLTS report, which will give us more insight on the jobs market, and a whole bunch of inflation reports. The inflation numbers seem likely to stay hot on the headline compared to last year but everyone knows that so I wouldn’t expect any big market reaction.

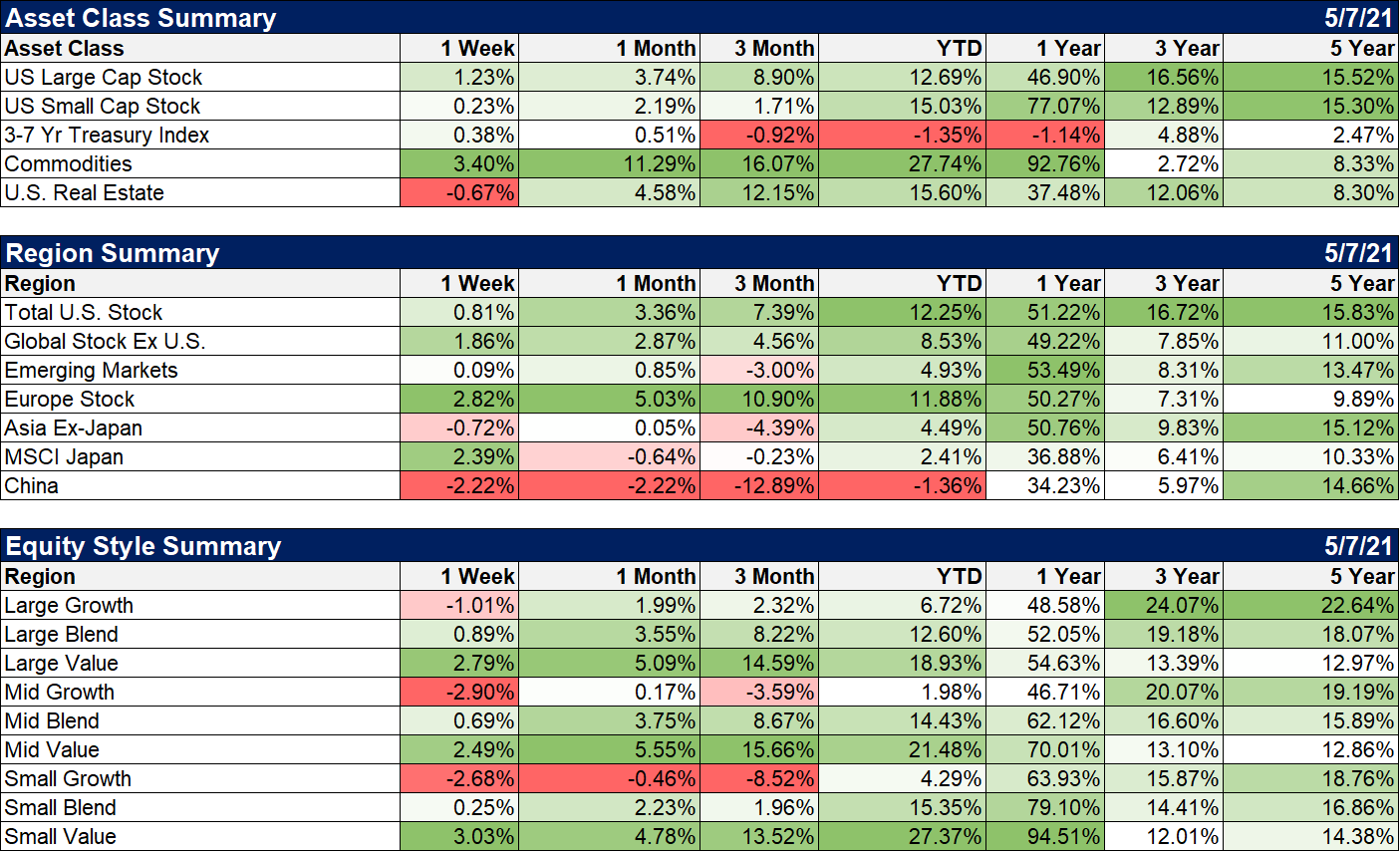

Stocks were higher last week with international ahead of the US and value outpacing growth. Real estate finally took a breather but commodities stayed hot and led the way again. The value trade still looks like it has more to go and we remain overweight.

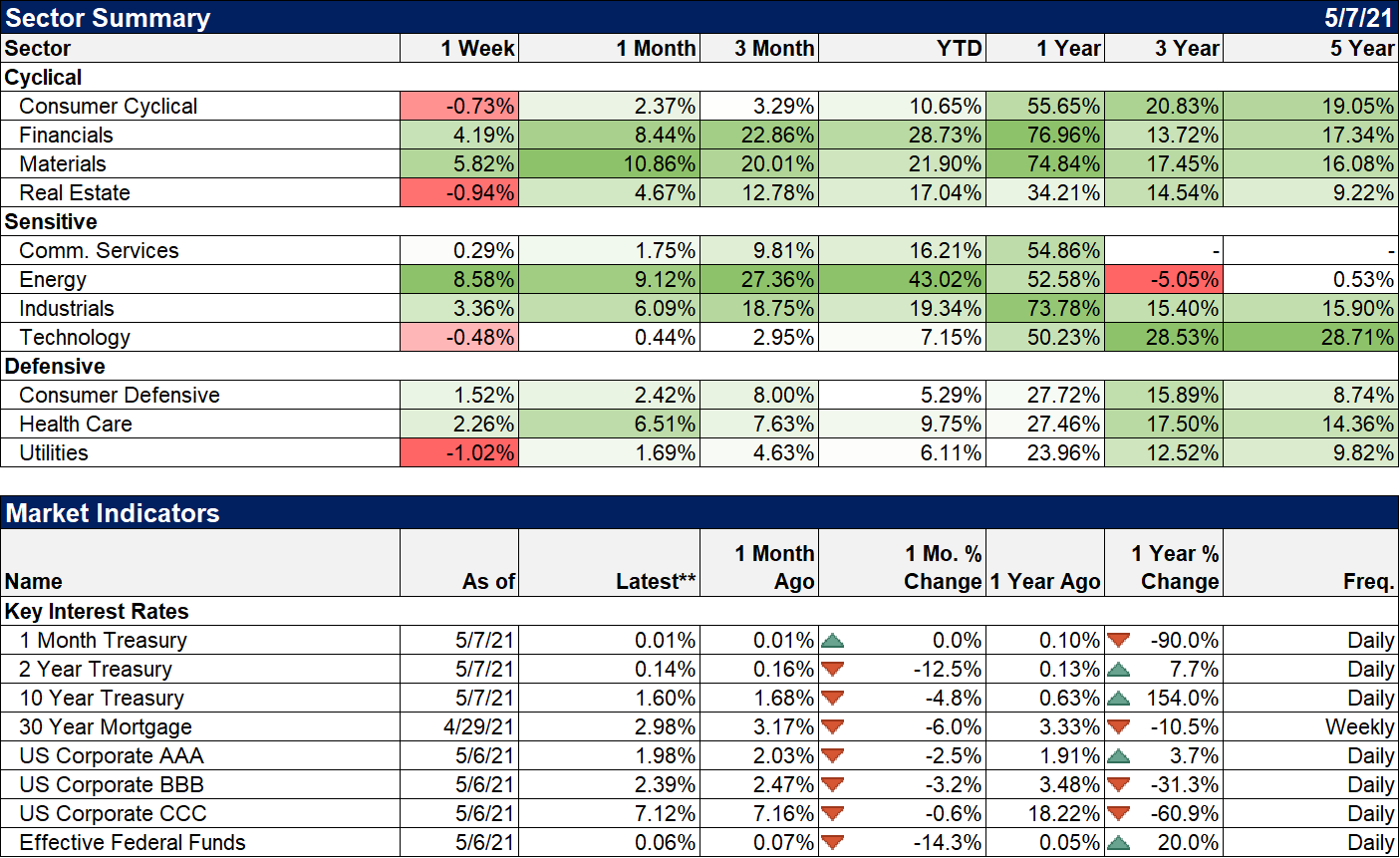

Financial, materials, and energy were the drivers of that value outperformance.

I don’t know when the crypto mania will subside but I’m confident that it will. I’m also confident that it won’t do so in an orderly fashion. What worries me is how it might impact other markets and the economy. We don’t know the linkages between crypto and the real world but they are there, if only psychologically. Would a meltdown in crypto lead to a reduction of risk-taking in other markets? Could it force liquidations we don’t expect? There’s an old saying on Wall Street that when you get a margin call, you sell what you can, not what you want to. The big swings you see in crypto prices are a result of limited liquidity. If we get a rush for the exits it may be that the easiest thing to sell is something else, like stocks. As you might guess from these commentaries over the last few weeks, we are starting to pull back a bit on risk. We’ve all made a lot over the last year and sticking around with a full risk allocation right now is starting to feel a little porcine. I don’t want to be around when this market decides to make pork chops.

Joe Calhoun

Stay In Touch