I thought of Gilda Radner this past week. Actually, I thought of a character she created on the original Saturday Night Live, Emily Litella, who was a regular on the Weekend Update segment. She’d start to rant about something topical, getting it completely wrong at which point Jane Curtin or Chevy Chase would explain it to her and she’d respond. “Oh. Well. That’s completely different. Never mind.” (For those of you too young to remember Gilda, here’s a link. Radner was a rare talent taken from us too soon by ovarian cancer.) There is no better description of the market moves that happen in the week of a Fed meeting. There’s almost always an initial market move based on a knee-jerk interpretation (or misunderstanding) of the Fed’s statement or Jerome Powell’s press conference performance. And then after a little bit of reflection, the market seems to say, like Emily Litella, well that’s completely different, never mind. At which point all the previous movements get reversed and we’re back where we started, as if the Fed didn’t really do or say anything of substance at all. Which is, of course, usually accurate and should have been obvious from the beginning. But the Fed has to talk and traders gotta trade so after every meeting we get the Emily Litella memorial market dance. You’d be better off taking Fed meeting week off and watching reruns of the first few seasons of SNL.

And so, last week the Fed met and for a few hours everyone thought it meant one thing but by the next day, everyone had decided that it didn’t mean that at all. In the end, bond yields barely moved and the outlook for the economy only changed mildly and I would say positively. The 10-year Treasury note yield was 1.46% on Monday and 1.45% on Friday. The yield rose from Monday to Wednesday and fell Thursday and Friday. The 10-year TIPS started the week yielding -0.85% and ended the week at -0.79%. If you take real yields as a proxy for real growth – and directionally that’s a good way to think of things – then real growth expectations rose on the week while inflation expectations fell slightly. And since that is what the Fed is trying to do – as if they had any control over such things – I’d say that was a pretty good week for the home team. But c’mon. We’re talking about 7 basis points here. It means as close to nothing as you can get without it actually being nothing. In other words…never mind.

I know what you’re thinking right now. If the Fed meeting was a big nothing, why did we see such big moves in other markets? Large-cap stocks were down 2% on the week and small-cap double that. The dollar was up 1.8%, gold was down 6%, copper down 8%. Crude oil was actually up slightly on the week but energy stocks were down over 5%. Platinum was down 9% and Palladium nearly 11%. Agricultural commodities all took a big hit. Large-cap value stocks were down but growth stocks managed a small gain. It was almost as if the Fed actually did something. Well, actually, amid all the discussion of dot plots and timelines it was almost missed but the Fed did actually hike rates last week. They raised the rate they pay on excess reserves and the reverse repo facility by 5 basis points each. That of course means….well, not much actually. Never mind.

One thing I think most investors don’t appreciate is how much of what goes on day to day in markets is just noise. Markets don’t always move on fundamentals. In fact, I’d say they rarely move on fundamentals because most investors – and I use that term very loosely these days – have no idea what the fundamentals are. Markets are nothing more than groups of people acting on imperfect information in less than ideal circumstances with their – or someone else’s – life savings on the line. If you think people are making intelligent, rational decisions in that environment I’d suggest you spend some time in the bowels of Reddit or Twitter or even, God help you, TikTok. That will certainly cure you of that particular delusion.

All that happened last week is that markets that had moved too far in one direction moved back in the other direction. Commodities had made a big run higher, fueling the inflation fears everyone has been talking about. Part of that was fueled by the widespread expectation of a weak dollar that I warned just last week was looking less and less likely, at least right now. The dollar bears had every opportunity to push the dollar lower, out of the bottom of the range it’s been in for six years and they just couldn’t get it done. And the longer it sat just above that level the less likely it was to fall through it. It was just a matter of time before the bears threw in the towel or the bulls got the upper hand. I’d also add that last week’s dollar move higher wasn’t any more significant than the previous move down. We’re still stuck in the same range as before and I think there is way too much uncertainty right now for a big move in either direction.

The same is true of the value versus growth debate. I heard multiple market commentators last week say that the change in the Fed’s dot plot pushed investors to sell value and buy growth on reduced growth expectations. I say hogwash. The Fed has no idea when they are going to hike rates because they have no idea what the economy will do between now and 2023. Hell, they have no idea what the economy will do between now and the end of the year. Nothing changed last week. The economy is still on the same track it was before the Fed meeting. It continues to recover at a pretty steady pace. And until something real changes, that’s exactly what we should expect for the immediate future.

The correction of overextended markets is just technical, an adjustment of an extreme. It’s what happens in systems like markets. It doesn’t have to “mean” anything other than, in this case, some people felt some urgency to take profits on some assets that had run up in price. And it probably isn’t over by the way so if like us you’ve raised some cash recently, you probably want to be patient. That’s the kind of virtue signaling every investor should practice.

———————————————————————————————————————————————————————————————————————————————————————————————————————-

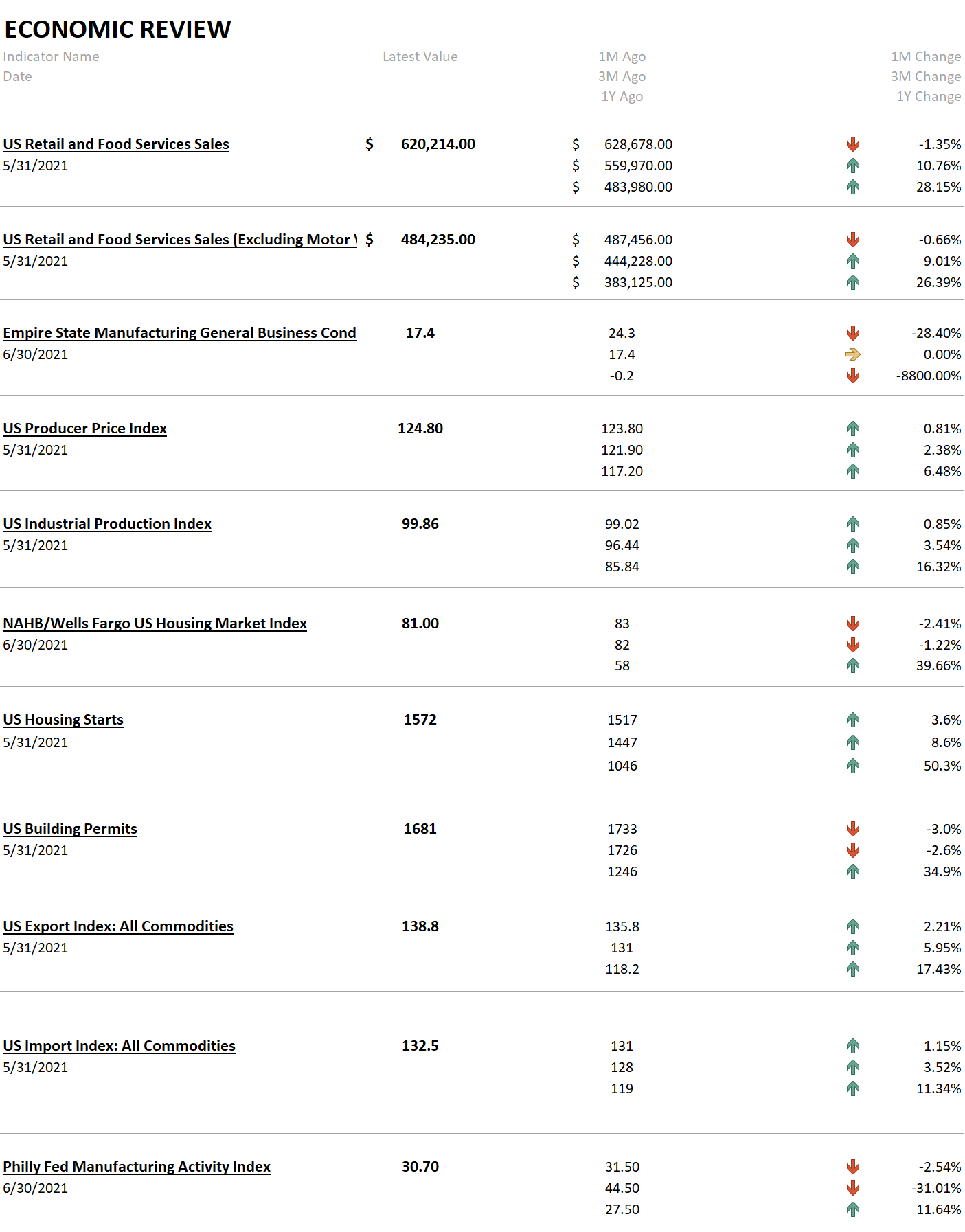

The economic data last week was pretty much as expected. Retail sales were down but from a very high level. Anyone expecting that pace to continue was asking for too much. The inflation reports were all “hot” and absolutely no one was surprised by that. Industrial production was up but remains well below pre-COVID levels which is still a concern but not a new one. IP is just 7% above where it was in 2000 and below where it was in 2007. Housing starts were up in May and while choppy I expect that trend to continue. We underinvested in housing for a decade so there’s still plenty of room for catchup.

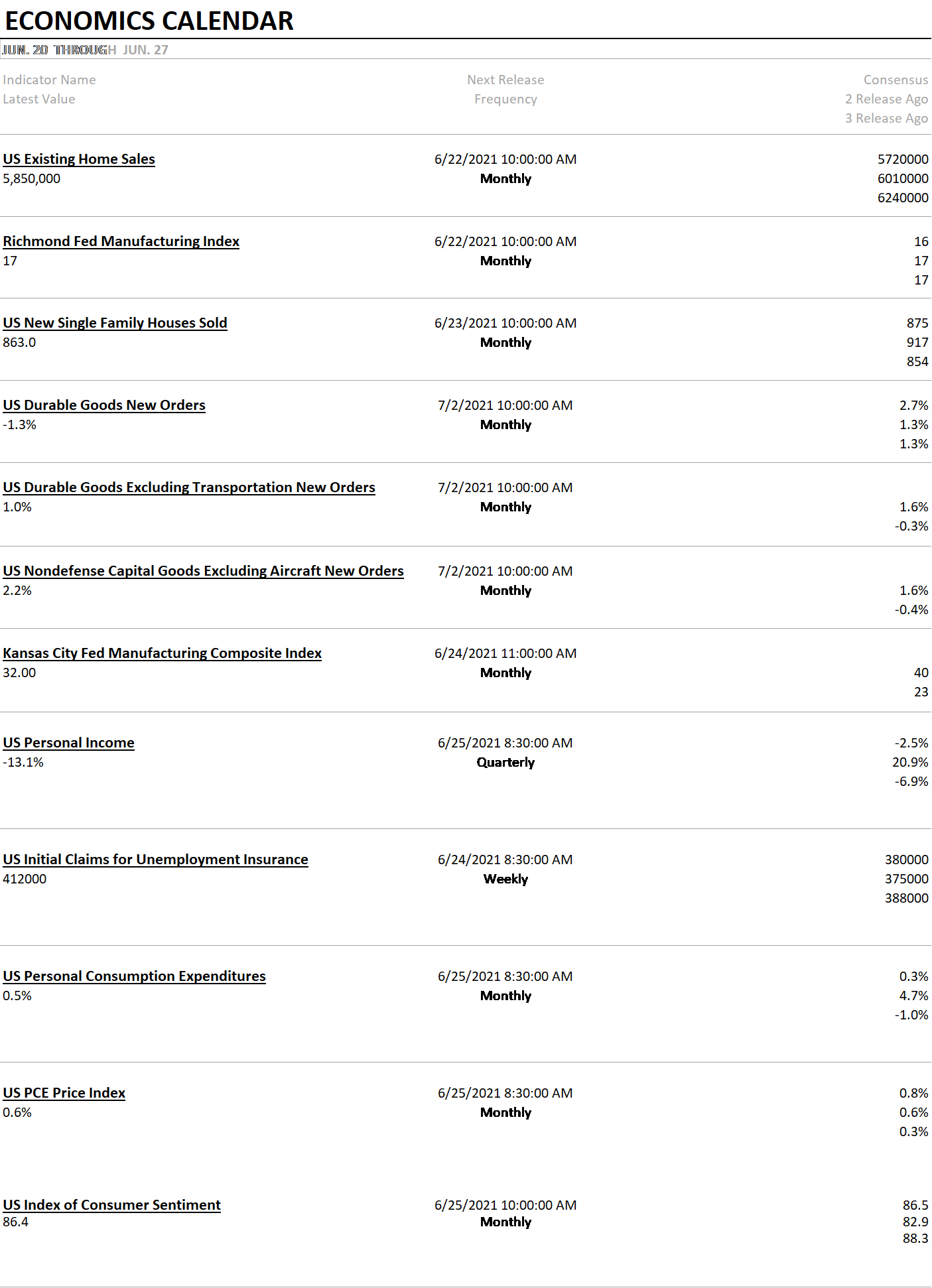

We’ll get some more data on housing next week with existing and new home sales. Durable goods orders are expected to be and I’d like to see core capital goods continue to trend higher. Personal income will likely be down but there are expectations for a rise in consumption. That likely hinges on services spending as goods spending starts to come in.

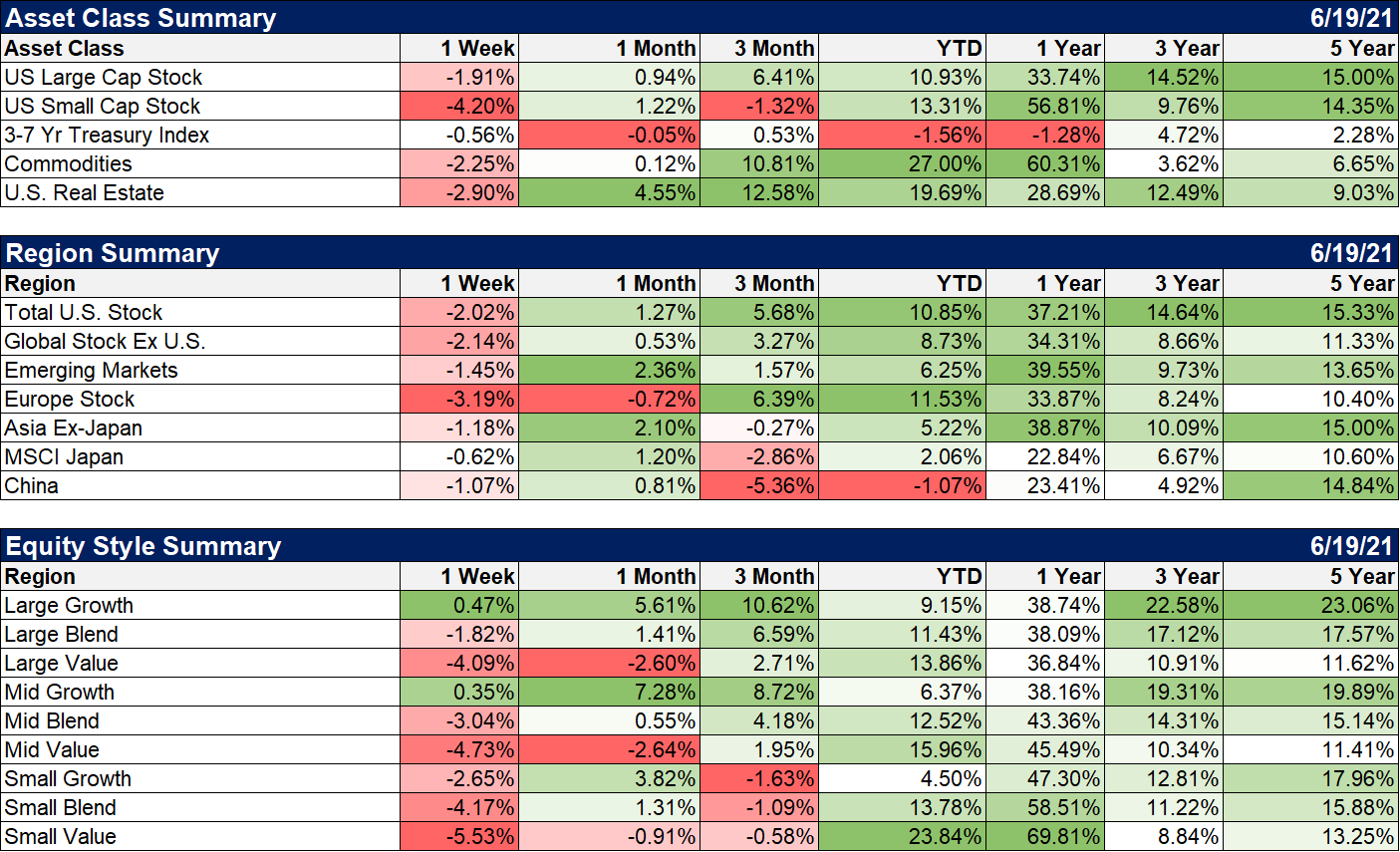

Basically, all asset classes got hit last week and value did take the biggest hit. But value is still the overwhelming winner YTD and over the last year for mid and small caps. Global stocks pretty much moved in line with the US although Japan did a little better. But of course, it had already corrected more and is barely up on the year. Emerging markets were down last week too but considering the move higher in the dollar I’m surprised they weren’t down a lot more. Outperformance with a rising dollar is unexpected and warrants extra attention.

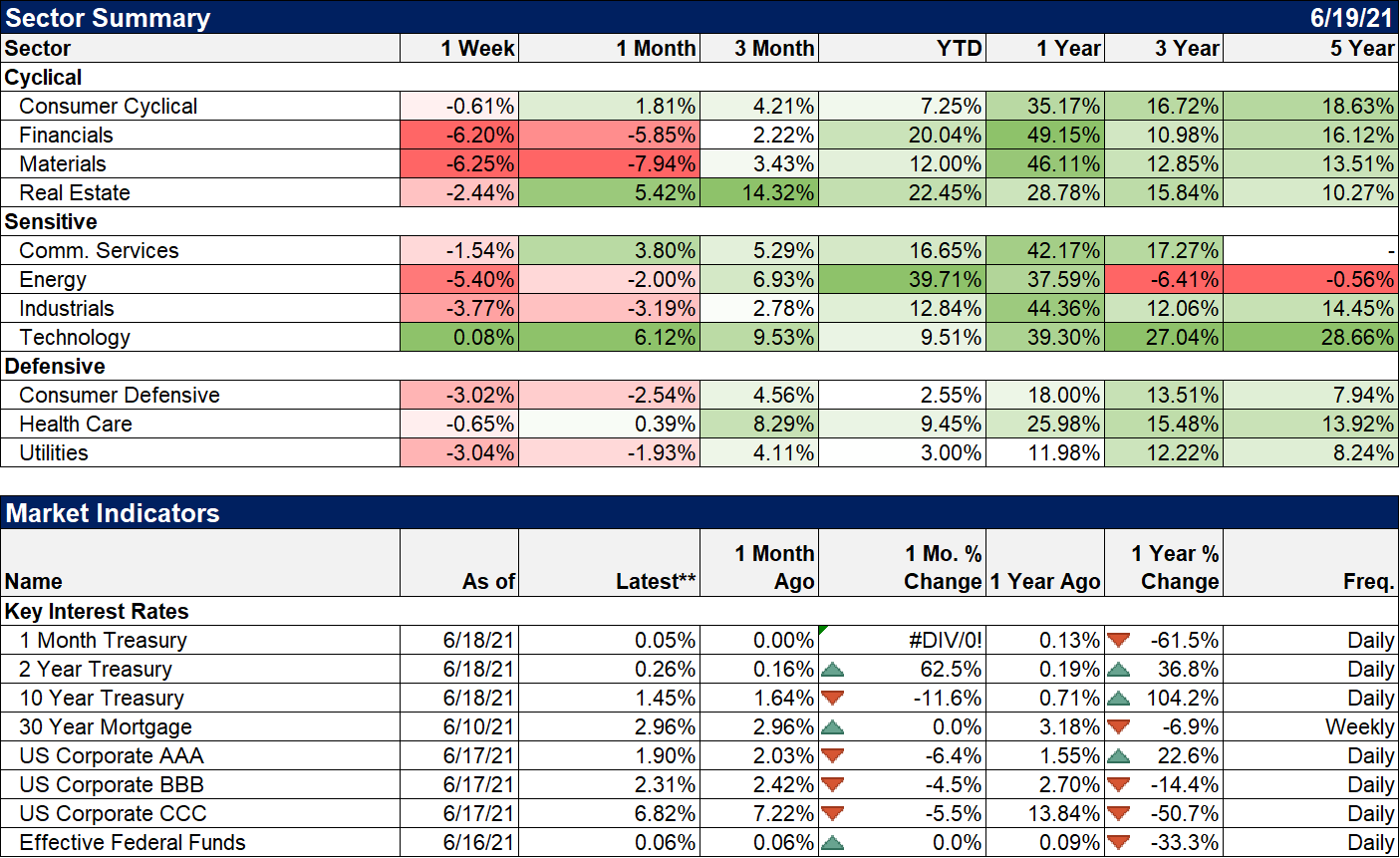

The most cyclical sectors took the biggest hits last week but why wouldn’t they? They are also the sectors up the most this year and over the last year. Some of these are still overbought though and probably have more correcting to do. But if the economy continues to improve they are probably the places you want to look to put money to work. Financials took a big hit last week but that was probably mostly about the yield curve which continues to flatten. The big question is whether we’ve seen the peak of the yield curve and I still think the answer is no. If that is right, financials are probably a place to look for buys as well.

It is human to want to make sense of every market move. We want to believe that there are always rational, logical reasons why things move the way they do. But there aren’t always obvious reasons or any reason beyond the old more sellers than buyers or vice versa. Accept it and don’t try to explain everything. Any explanation we come up with is just as likely to be wrong as right anyway. Learn to say never mind and concentrate on things you can control.

Joe Calhoun

Stay In Touch