The Salvadoran colón is still technically legal tender in El Salvador. The country’s government under President Francisco Flores had passed the Law of Monetary Integration in 2000, taking effect on January 1, 2001. This legalization of the US dollar for domestic circulation didn’t specifically remove the colón from common purchases or prohibit its use; the country’s Central Reserve Bank just stopped printing any more denominated paper notes and ceased minting any more of its coins.

Why not switch to the dollar? During the decade of the nineties, in particular, dollarization in one form or another was all the rage across emerging and hopeful market economies like El Salvador’s. After all, there were plenty of them (eurodollars, but still). Unlike many of these local currencies, it wasn’t about the exchange value, instead the more succinct functions of any global reserve currency meaning “liquidity” and reach.

The entire point of a global reserve currency is to be a medium, an intermediary by which different and often very disparate nations spread all over the world (in an increasingly globalized economic system) can effectively, efficiently, and fluidly transact with one another. For this to happen, that medium or middle currency must be widely available to everyone and in dependable open supply.

That was eurodollar, not dollar.

In early June 2021, El Salvador pledged to switch up its monetary arrangement all over again. The dollar’s not being replaced like the colón once was, at least not intentionally. The foreign currency is now planned to be supplemented by Bitcoin. El Salvador aims, later in the fall, to become the world’s first sovereign entity to embrace this form of cryptocurrency as equally legal tender.

This has many officials and “experts” stumped. Why? Why now?

Even hardcore Bitcoin maximalists are at somewhat of a loss to explain it. On the one hand, this is exactly what they’ve been preaching ever since the pseudonymous Satoshi Nakamoto laid down the currency’s genesis block way back on January 3, 2009. Bitcoin, they say, is an actual and useful currency so here’s a country willing to put their form of modern money where its confusing mouth is.

But – and here’s the hang up – Bitcoin is supposed to supplant the dollar because the latter has been judged by its most hardcore proponents as worthless; the Fed and its obscene levels of “money printing” and all that. Not, in other words, what El Salvador is up to.

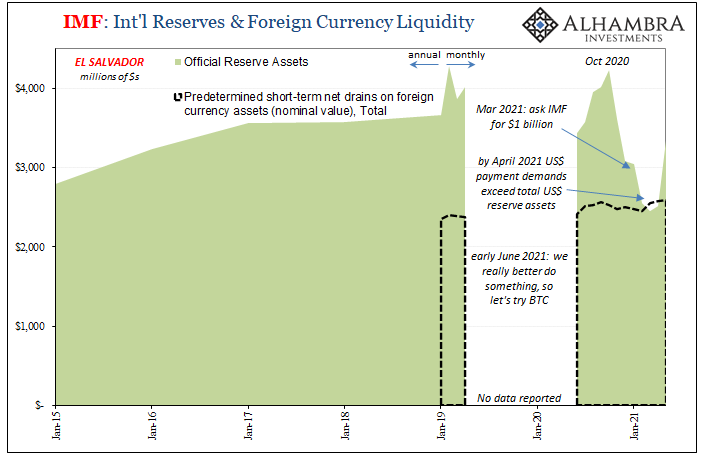

The country isn’t attempting to defend itself from the eurodollar system’s imminent demise. On the contrary, officials from El Salvador had previously, in early March 2021, just three months before this Bitcoin gambit, opened discussions with the IMF for a further $1 billion infusion – our first clue about what’s actually happening here.

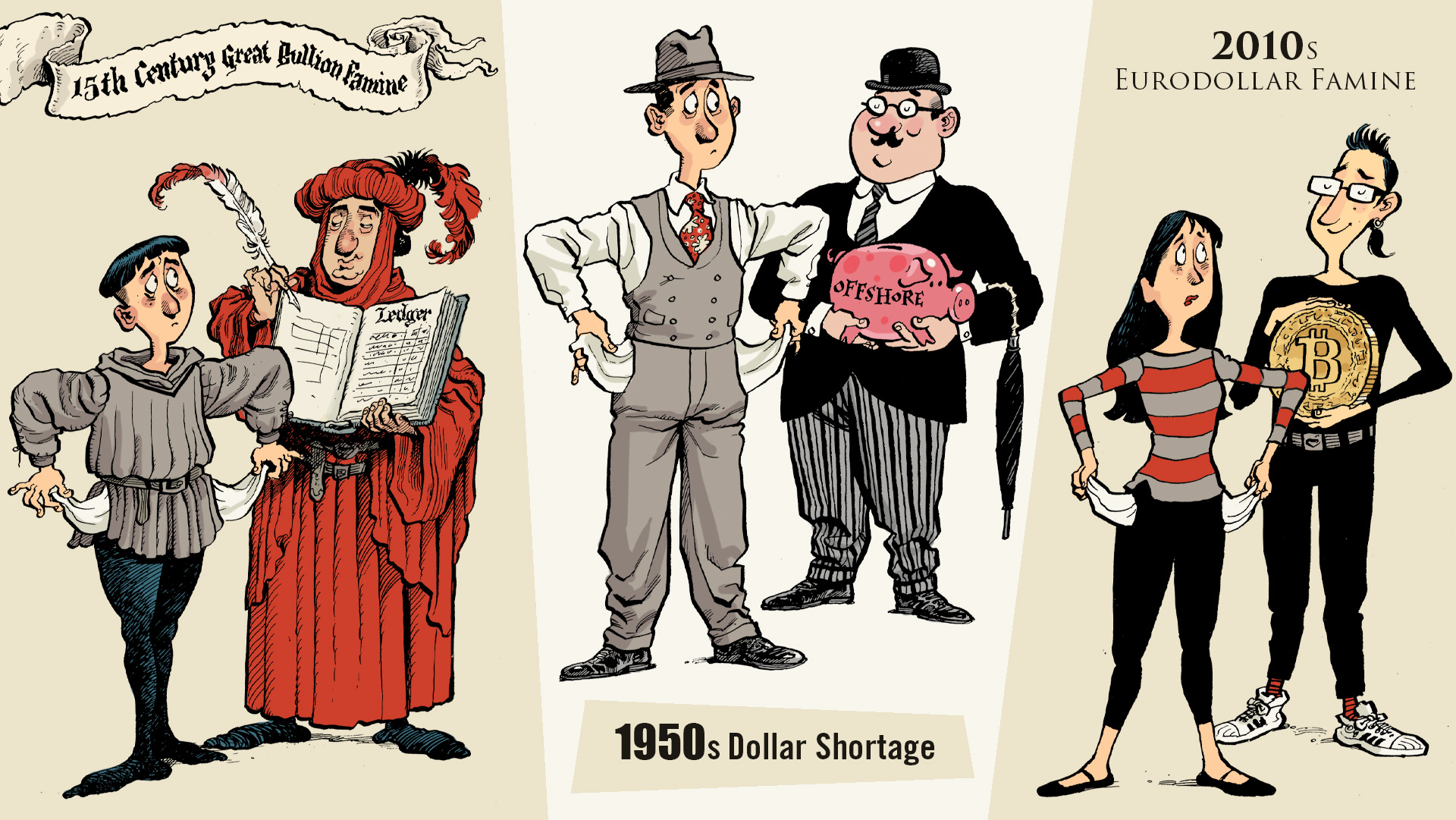

In a very important sense, digital currencies like Bitcoin aren’t anything new. The technology, nomenclature, and the way it works certainly are, but the concept is centuries old. Ledger money.

Ghost money, in fact.

The reason this ghostly ledger form of money arose in the first place all the way back in the 14th and 15th centuries was a familiar (to those who understand the eurodollar and the reserve currency regime of the last half of the 20th century spanning to the present day) problem to the current age: inelasticity. Lack of money supply, not too much.

Money isn’t the wheel, it’s the grease that keeps the wheel of economy and commerce rolling in its most effective method. Rising living standards and social progress are likewise successful monetary endpoints.

In the absence of sufficient access to acceptable money, clever private participants will do whatever they have to in order to continue conducting commerce as best they might. That’s really the point for money; it is not itself wealth, rather a tool that a free market, capitalist system might better create true wealth in the form of sustainable commerce.

This is where ghost money, or money of account, came into things during a time today called the Great Bullion Famine (I wrote about it in greater detail here, I think it worth your time):

Money-of-account was one such alternative which also blurred the lines between money and credit; in one sense, using ledgers to settle transactions even between merchants was under the strictest definition credit rather than a monetary substitute. But that was the case only insofar as eventually this paper IOU would have to be disposed of by bullion or specie.

What if a merchant system merely traded the paper IOU’s, and did so on a form of widely shared ledger?

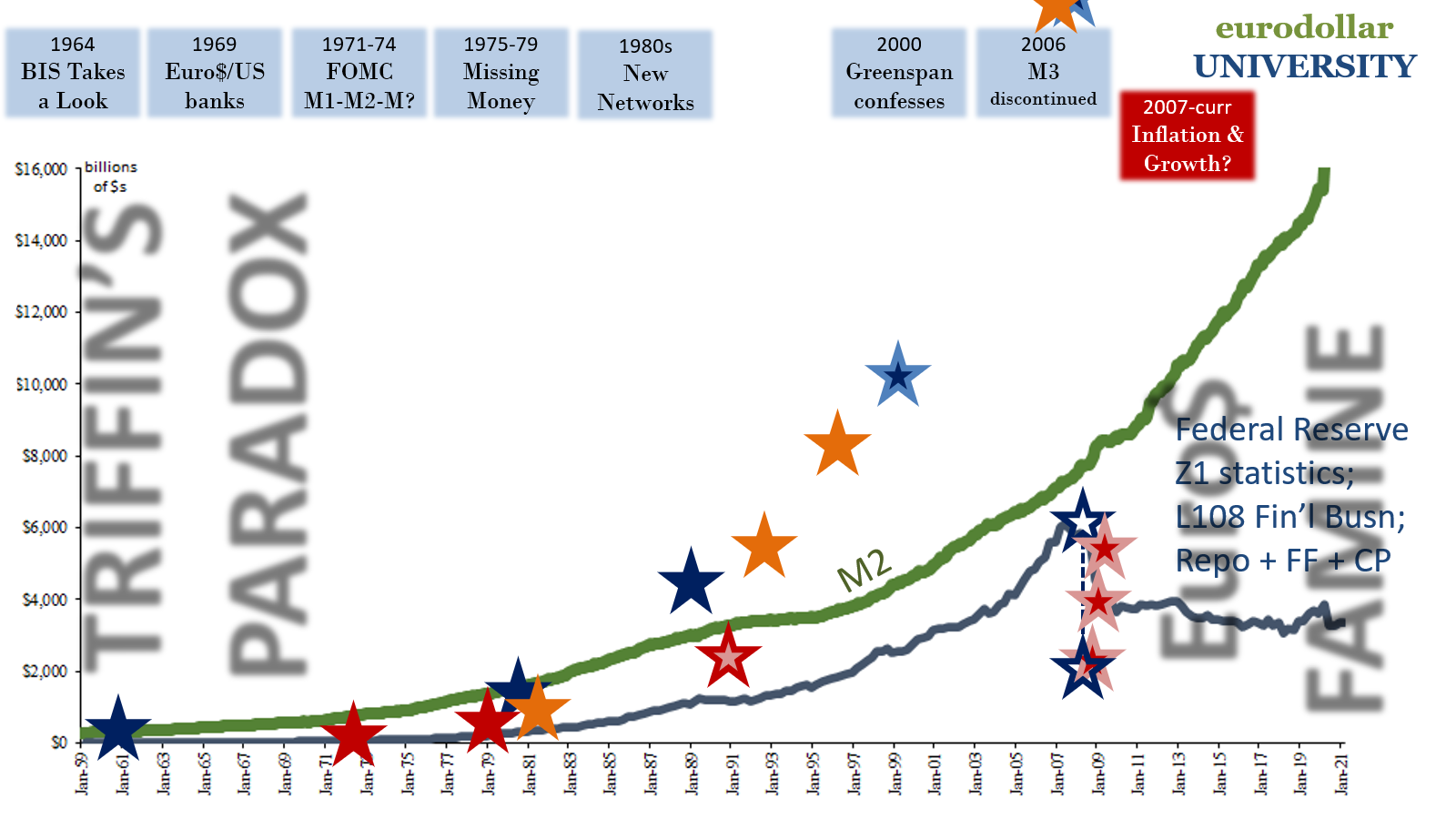

As I described in that essay, what was the eurodollar itself other than still another form of money of account, this ghostly ledger money? And it came about in response to the same conditions as the early 14th century; inelasticity in its case the way of Triffin’s Paradox.

The eurodollar arose to global supremacy because of its ceded ability to privately create ledger money which not quite seamlessly “solved” (depending upon your point of view) the monetary restrictions of the hapless Bretton Woods arrangement. The world needed dollars to globalize, the US couldn’t supply them officially given its gold reserves. The global banking system created this eurodollar ledger to circumvent and supplant (long before August 1971) its reserve functions.

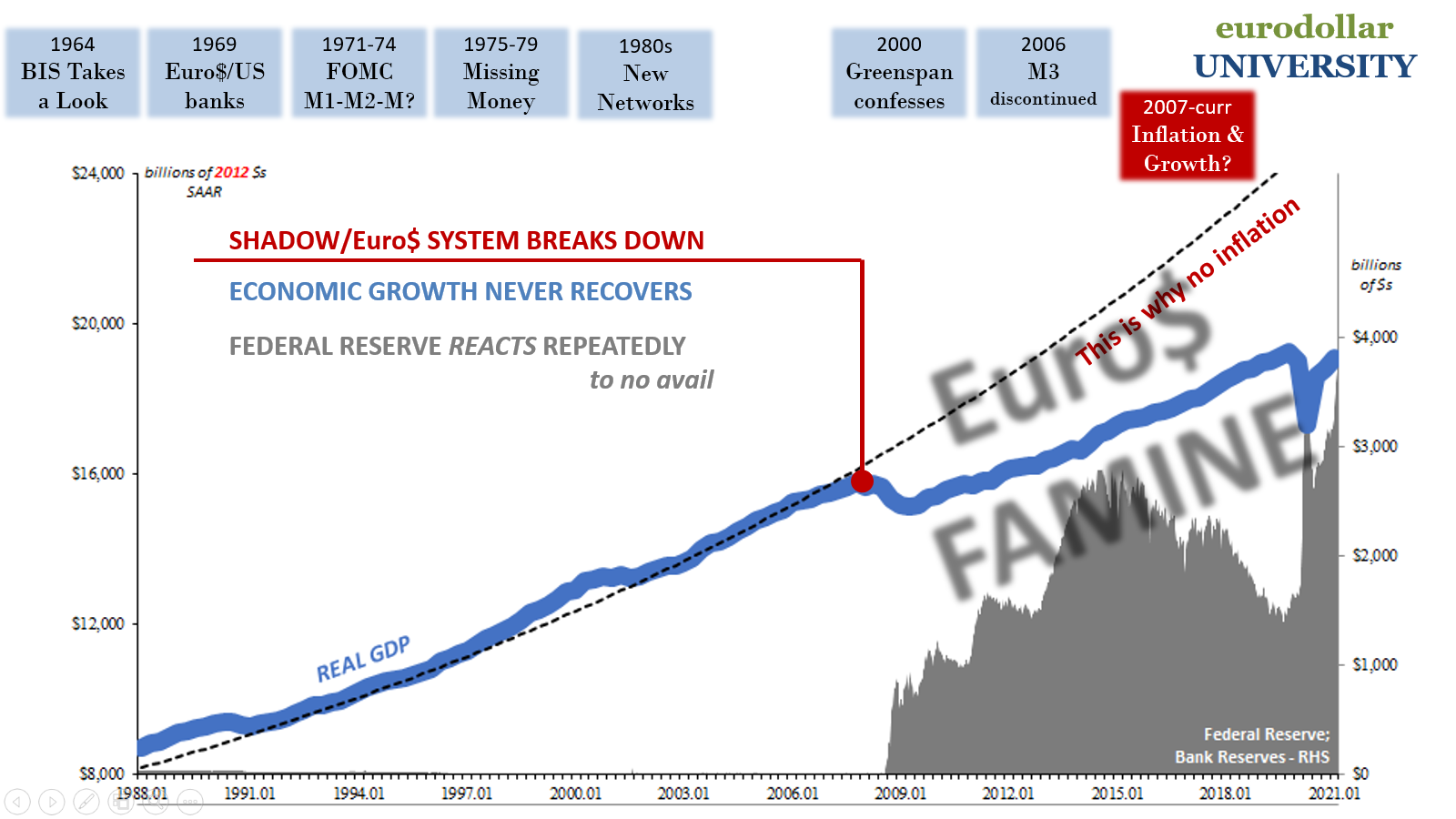

Ever since August 9, 2007, however, we’ve entered a new age, the age of the Eurodollar Famine. Once again, in response to increasingly irresponsive global money, the ledger solution has proliferated.

In other words, crypto currencies like Bitcoin have flourished not because of excessive “money printing” and the ultimate danger to the dollar, rather consistent with a very long history and deeply-seated human desire to use successful money as an economic tool. They are a familiar answer to the inelasticity (too little money) of the current eurodollar era.

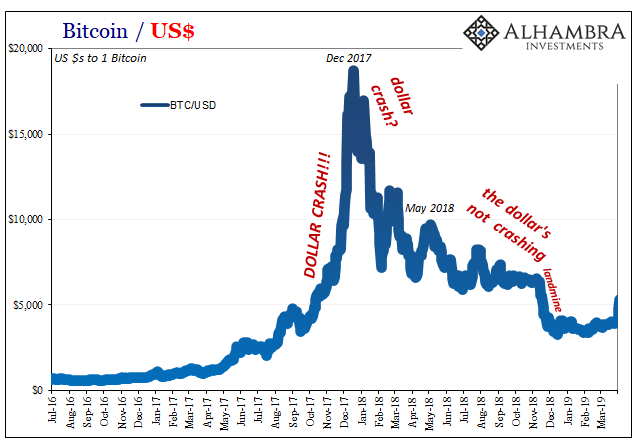

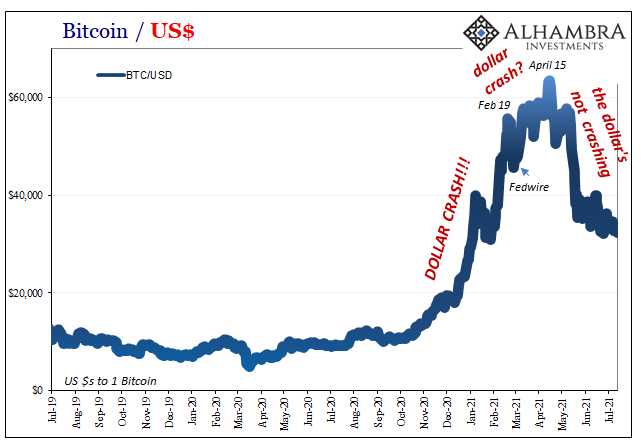

What’s makes this especially confusing is the price behavior of these digital offsprings, with most still believing the reckless Fed narrative and its related money-printer-go-brrrrr meme. While this may be the reason speculators and even regular (seeming) investors pile into these things, twice now (2017 crypto bubble was first), it’s also the reason they then pile right out of them.

They’ve got it all wrong.

The public hears from the media, egged on by more irresponsible voices, that the US dollar is toast. They heard this in 2017, and it reared its head even more forcefully, exuding more certitude, once more in October 2020. The dollar was dead. Done. Gone. Mere matter of months.

From there, it became another self-fulfilling, circular reference prophecy; crypto is up because the dollar is dead, and because the dollar is dead that’s why everyone is piling into crypto. Until the herd realizes(d) the “money printing” stuff wasn’t real, and that the dollar seemed(s) more than capable of retaining at least its exchange value as well as stubbornly persistent common use (despite so many problems).

Then they all pile out. From yesterday:

Trading volumes at the largest exchanges, including Coinbase, Kraken, Binance and Bitstamp, fell more than 40% in June, according to data from crypto market data provider CryptoCompare, which cited lower prices and lower volatility as the reason for the drop.

In June the price of bitcoin hit a monthly low of $28,908, according to the report, and ended the month down 6%. A daily volume maximum of $138.2 billion on June 22 was down 42.3% from the intra-month high in May.

There are, therefore, two simultaneous processes going on in the digital currency space, each one incompatible with the other because of so many mistaken mainstream assumptions. The price action is divorced in every possible way from the true underpinning fundamentals. The crypto bubble(s) proceeds from this false assumption all the while, underneath all along, the digital revolution makes stunning progress because it has nothing to do with the excesses of “money printing.”

The real purpose behind crypto is the same as the original eurodollar and the ghost money of long ago – inelasticity leading to ledger money innovation, private forms of money of account of which digital currencies are just the latest. It needs to be said – over and over – that governments have never had a monopoly on currency.

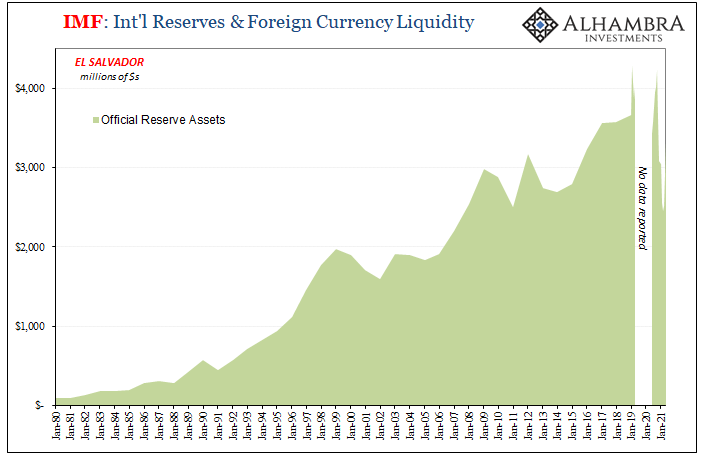

This is where El Salvador’s adoption comes into it. They don’t want to replace the dollar, but at the same time the government absolutely recognizes the nation has a huge dollar problem that’s pretty bad already yet has the disastrous potential (see: below) to get even worse (thus the IMF) – they certainly aren’t acting in fear of Fed money printing. They don’t have nearly enough (again, eurodollars).

According to their filings with the IMF, El Salvador has run into the same global money issues as many emerging countries big and small (just ask China). Over the past half decade, in particular, the eurodollar has turned against them in the respect of making eurodollars harder to come by and therefore making the reserve system more and more difficult for El Salvador (especially as this country depends upon foreign remittances from expats for much of its dollar supply).

Their Bitcoin gamble is, essentially, an attempt to deliver money elasticity the eurodollar system no longer seems able (and hasn’t for years) to provide. This monetary deficiency has become much worse and more immediate in El Salvador since last October (ironically the same timeframe as the latest Bitcoin bubble) as already-too-low official reserve balances have absolutely plunged below bare minimums.

In the end, in terms of our analysis here, what El Salvador has proposed isn’t confusing at all. It is, on the contrary, perfectly consistent with what’s actually happening across the money world, the real (and still failing) eurodollar reserve currency regime.

Ghost money is a historically effective stab at elasticity, but it takes time. Cryptos are (long run, not short run) ghost money. The eurodollar, the true reserve, isn’t going anywhere for quite a long time. Therefore, all these things together.

I’ll begin to finish up with what I wrote at the tail end of the last bubble, this from December 8, 2017, not even two weeks before its top:

From China to Europe there are official and unofficial voices expressing grave doubts and discomfort over Bitcoin without really considering blockchain. It may end up where Bitcoin sinks the blockchain given that its greatest risks are all political (an outright ban).

The only way to thwart those intentions is for enough people to take a determined interest in cryptos as a class rather that solely as speculation in the one; to see the great potential in the real stuff of its evolution, and not get hung up on something like price. We have to step ourselves outside of currency and appreciate the currency system, and do it with enough of a broad basis of appreciation that it overcomes and survives what will surely be an effort to kill it.

This is where you can be positive despite the inappropriate price behavior; even after that last bubble, and with the current one looking pretty shaky, digital currencies (real ones, not stupid CBDC fakes) have only proliferated and further evolved. Even central banks are conspiring more to compete with them than outright ban private digital. That’s their long run potential regardless of short-term price idiocy brought about by an understandably huge mistake (thanks to central bankers and their puppet shows) about real money.

The real, effective money system is nothing like which drives this misunderstanding. Too little money. Not nearly enough redistribution. Cyclically not dependable. Nothing has changed since August 2007 no matter how many QE’s and how many trillions in bank reserves. This includes, thank you El Salvador at least for this one small silver lining, the latest ill-conceived inflationary presumptions of 2021.

Price bubbles in digitals have come and gone, and may continue to come and go, so long as the inelastic eurodollar remains the spooky, upsetting always-unseen spectral monetary noises are only going to get louder anyway. Just watch out their prices as they do.

Stay In Touch