The economic slowdown we’ve been writing about for months officially arrived last Friday in the form of a particularly weak employment report. The number of new jobs created last month – or at least the WAG the BLS makes at such things on a monthly basis – was a mere 235,000 or roughly a cool half-million less than expected by economists who insist on trying to guess this random number on a monthly basis. There was hand wringing and pearl clutching all over the financial media as economic gurus tried to figure out what it all meant. Is the recovery over? Is this as good as it gets? Will this affect the timetable for the Fed’s tapering of QE? Will this affect the spending and taxing bill the current administration is trying to push through Congress? Oh, whatever does it all mean????

The first thing you need to know about last Friday’s employment report is that it was for August, the month that seems to always get revised a lot because, after all these years, the BLS still has trouble figuring out how many teachers went back to work when. I remember an August employment report way back in the early part of the last decade (2011) that showed zero jobs created when expectations had been for over 100k. Stocks sold off hard, down 2.5% on the day as fears about the recovery spread:

August brought no increase in the number of jobs in the United States, a signal that the economy has stalled and that inaction by policy makers carries substantial risk.

The government report on hiring, released on Friday, prompted another round in a relentless diminution of economic expectations. The unemployment rate, at 9.1 percent, did not change last month, and the White House said it was expected to stay that high through at least 2012.

New York Times, 9/2/2011

Bonds rallied big that day, the yield on the 10-year Treasury falling 15 basis points to 1.99%. The dollar also rose on what was termed “safe haven” demand and continued to rally for the next month by almost 7%. These moves peaked after about a month before starting to reverse and by the end of October, bond yields were higher than they were before the report and the dollar was back where it started. Stocks fell a bit more, down about 6.6% at the nadir, but by the end of October were nearly 7% higher than they were before that lousy employment report. Even more interesting is that after numerous revisions the original 0 jobs reported turned out to actually be a positive 126k. All that market movement over a number that turned out to be utterly wrong. And that, my friends, is why I don’t pay a lot of attention to employment reports.

I think it got lost in the shuffle but it should be noted that if last week’s report was accurate – a mighty big if considering the previous paragraph – the US economy did still add 235,000 jobs in August. The economic recovery is still intact even if at a reduced rate of change. Again, we have been talking about a slowdown in the rate of improvement since the spring when bond yields peaked and turned lower. If you remember, there was a lot of confusion back then as people couldn’t figure out why bond yields were falling when the economic data was so strong. A plethora of explanations were offered, mostly technical ones having to do with Treasury issuance and QE. Our explanation was the simplest, the Occam’s Razor explanation – growth expectations were being scaled back. We didn’t know anything about the Delta variant or anything else; we just took the bond market at its word. It isn’t always right in the short-term – all markets overshoot – but bond markets, like all markets, look ahead. And when it comes to the economic health of the nation, bonds seem to autocorrect a lot quicker than other markets. There is a good reason we spend so much time thinking and writing about bonds.

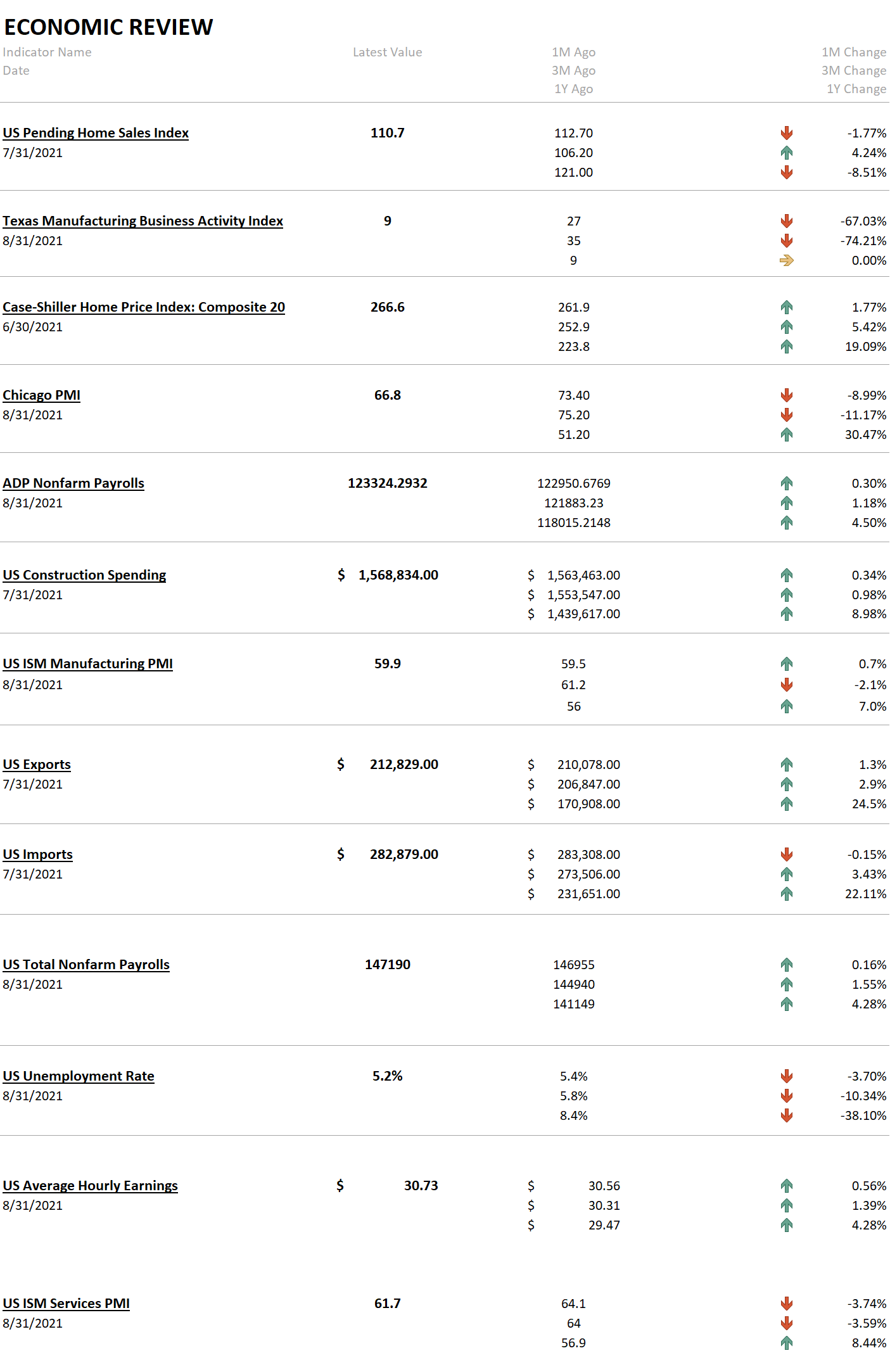

And so, as is often the case, the market reaction to last week’s employment report was a lot more interesting than the report itself. In fact, there were several reports prior to Friday’s official employment report that further enhanced the case for a more substantial slowdown. Pending home sales fell, which shouldn’t be that surprising given that home prices were reported to be up nearly 20% year-over-year. Supply/demand explanations are often pooh-poohed by economists as overly simplistic – more math is always preferable to an economist – but sometimes, simple works just fine. The Dallas Fed business activity index fell from 27 to 9, US imports fell, and the ADP report foreshadowed the BLS report on Wednesday with a less than expected gain of 374k jobs. And through all the weak reports, bonds traded in a narrow range and the 10-year Treasury yield finished the week higher than it started. The economic weakness in the current data was already priced into the bond market over the last few months.

There is a lot of data in the economic indicators but usually not a lot of new information. There are certainly long-term trends we track that inform our view of the economy (see here) but those are trends that play out over a very long period of time. And in truth, we can’t even say for sure whether some of these long-term trends are negative or positive. Whether a labor force participation rate of 67% (2000) or 63% (2016-2020) or 61.7% (now) is ideal is a question I can’t answer. It seems obvious that a lower number is bad but what do we mean by bad? If our only concern is maximizing near-term output then certainly lower is worse. But could a lower rate be better from a long-term, societal standpoint? Could having a parent home more often, not participating in the formal economy, create better conditions for economic growth in the future? I think it might but I don’t know for sure; I can’t quantify it and we won’t know the answer for years, maybe decades. It’s interesting but not particularly useful for investing today.

A lot of the market moves last week actually seemed to point more to the end of this slowdown rather than a continuation. It looks more and more to me that bond yields made a bottom in July and are starting to anticipate the end of the Delta variant that is the most popular explanation for the slowdown. The weakest parts of the employment report were in the service sector such as retail trade and restaurants and bars, which aligns with Delta as the cause. As Delta fades, those areas of the economy will be expected to pick up. The dollar was also down last week (which everyone should have expected since I declared it to be in a short-term uptrend the previous week), so there doesn’t appear to be any big fear out there about the global economy. And even with all the bad news coming out of China, emerging markets managed to have a good week. EM stocks were up nearly 3% and currencies were up too but less. That is not what we would expect from a market where a US-led economic slowdown is still on the horizon.

The employment report in August 2011 was released in the midst of a debate about the need for more stimulus for the economy. It was 2 years after the end of the recession, weekly jobless claims were still in the 400s but had stalled after falling steadily in 2010. The unemployment rate had been stuck around 9% since early in the year. Bond yields peaked in March at about 3.4% and had fallen to around 2.2% by the end of August (before that employment report was released). In short, things didn’t look very good in late 2011 and they would get worse in 2012. Bond yields continued to fall until July of 2012 and credit spreads didn’t peak until October. And I can tell you we were on recession watch at the time because that’s where markets seemed to be pointing. But even markets aren’t always right and there was no recession of 2012. Or 2013 or 2014 or 2015 or 2016 or 2017 or 2018 or 2019. During the course of an economic cycle, the economy will slow and reaccelerate numerous times. It is during the slowdowns that we are most vulnerable to recession (obviously) and stock market corrections which is why we react to them in our portfolios but most of them are just slowdowns that soon pass. I think it might be wise to remember 2011 and realize that today’s conditions are, in many ways, better than back then.

Markets are always forward-looking. The drop in bond yields that started back in March anticipated the slowdown we’re in right now. Millions of people making independent judgments changed markets to reflect a more accurate view of the future than any Wall Street analyst or economist. Investors who analyze today’s economic data to determine how markets will move in the future are driving by looking in the rearview mirror. The better method is to watch markets today to determine how the economy will change in the future. Markets are not perfect but they provide a truer picture of the economic future than any crystal ball. The markets are the windshield of the economy, providing a glimpse of the future to those who face forward.

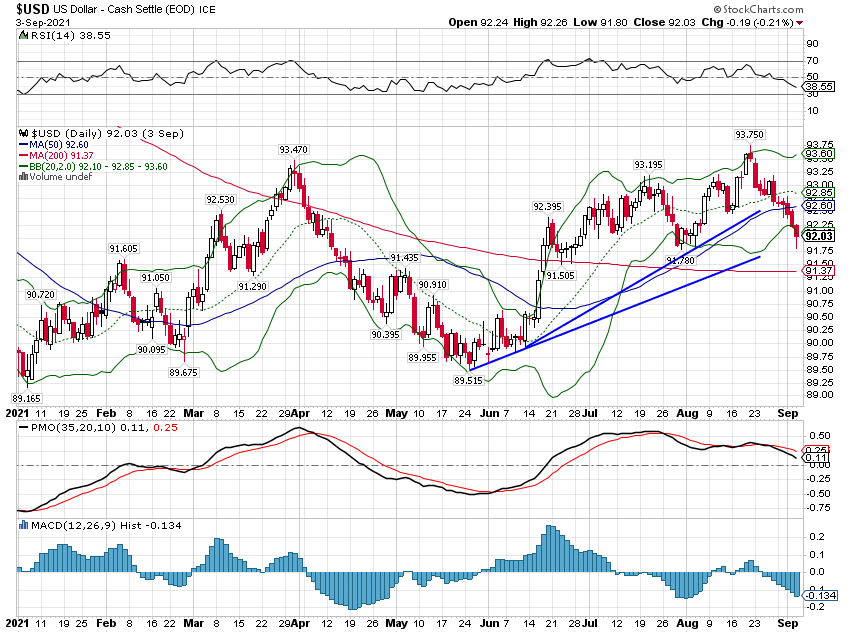

The economic environment, for now, remains the same but if bond yields keep rising and the dollar keeps falling, I’ll have to make another change. But for now, the economy is still slowing and the dollar is still fairly firm. The 10-year yield is 19 basis points off the lows of July but I don’t see a clear trend yet except to say that yields have stopped falling for now. As for the dollar, it is around 92 now, down from 93.5 but still well above the 89.2 low set in January and the 89.5 levels seen in May. What’s required now is patience until new trends emerge. I never said the windshield was always clear.

There was some pretty good data released last week too. The Chicago PMI was a little less than expected but at 66.8 remains high by historical standards. Construction spending was higher, exports rose and the ISM reports were better than expected.

One last note on the employment report. Average hourly wages were up 4.3% year-over-year which sounds pretty good – until you realize CPI was up 5.3%. There seems to be a collective loss of memory in Congress and at the Fed in that they seem to think that inflation can somehow improve the lot of the working middle class or poor. Nothing, and I mean absolutely nothing, could be further from the truth. Inflation is a pernicious, regressive tax and is ultimately destructive of the growth it is meant to engender. I thought we learned that in the 60s and 70s but apparently not. Jerome Powell is pretty awful but the apparent alternative (Lael Brainard) may be worse. Better the devil you know, I guess, but monetary policy isn’t about to improve.

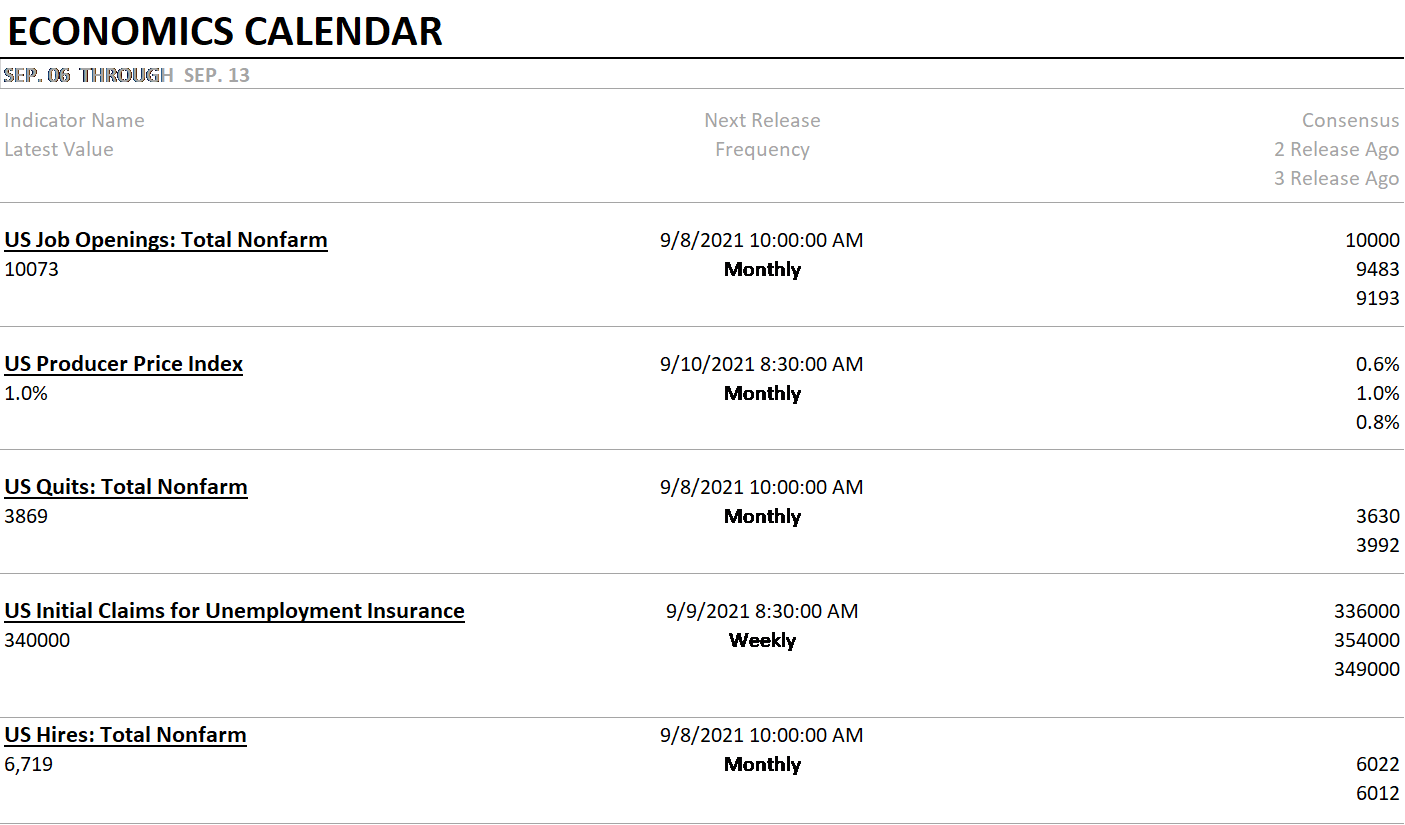

Not a lot of data in this holiday-shortened week. The JOLTS report should be interesting but the labor market is a long way from normal. There are job openings and more than enough unemployed to fill them but they aren’t being filled for some reason. More accurately probably several reasons but we’ll eliminate one soon as the Federal unemployment benefits enhancements end.

Stocks were higher last week with the larger gains in foreign markets. That was probably helped a bit by the weaker dollar but not much has changed on that front. The dollar index is still stuck in the same range it has been in since 2016.

The biggest winner of the week was Japan which seems a bit odd with their current COVID difficulties. But they are also about to get a change in government and there is rarely a more optimistic time than right before a country gets a new leader. It takes time before the inevitable letdown sets in. I have been a long-term investor in Japan since just before Abe was elected the first time and the story remains the same. Japan is an attractive investment because of corporate restructuring and in spite of the macroeconomic environment. And even after a 250% gain since 2012, stocks there are still cheap.

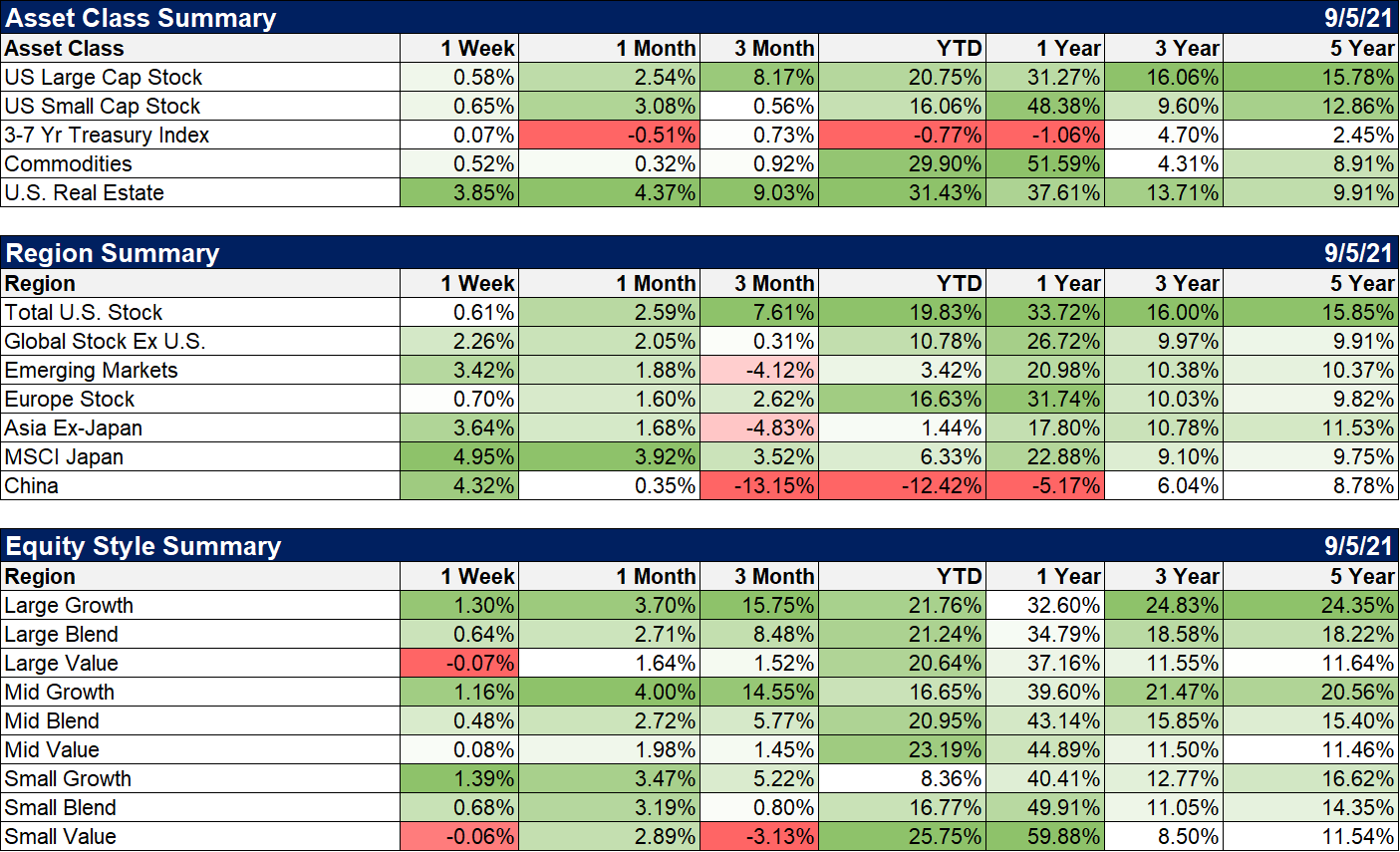

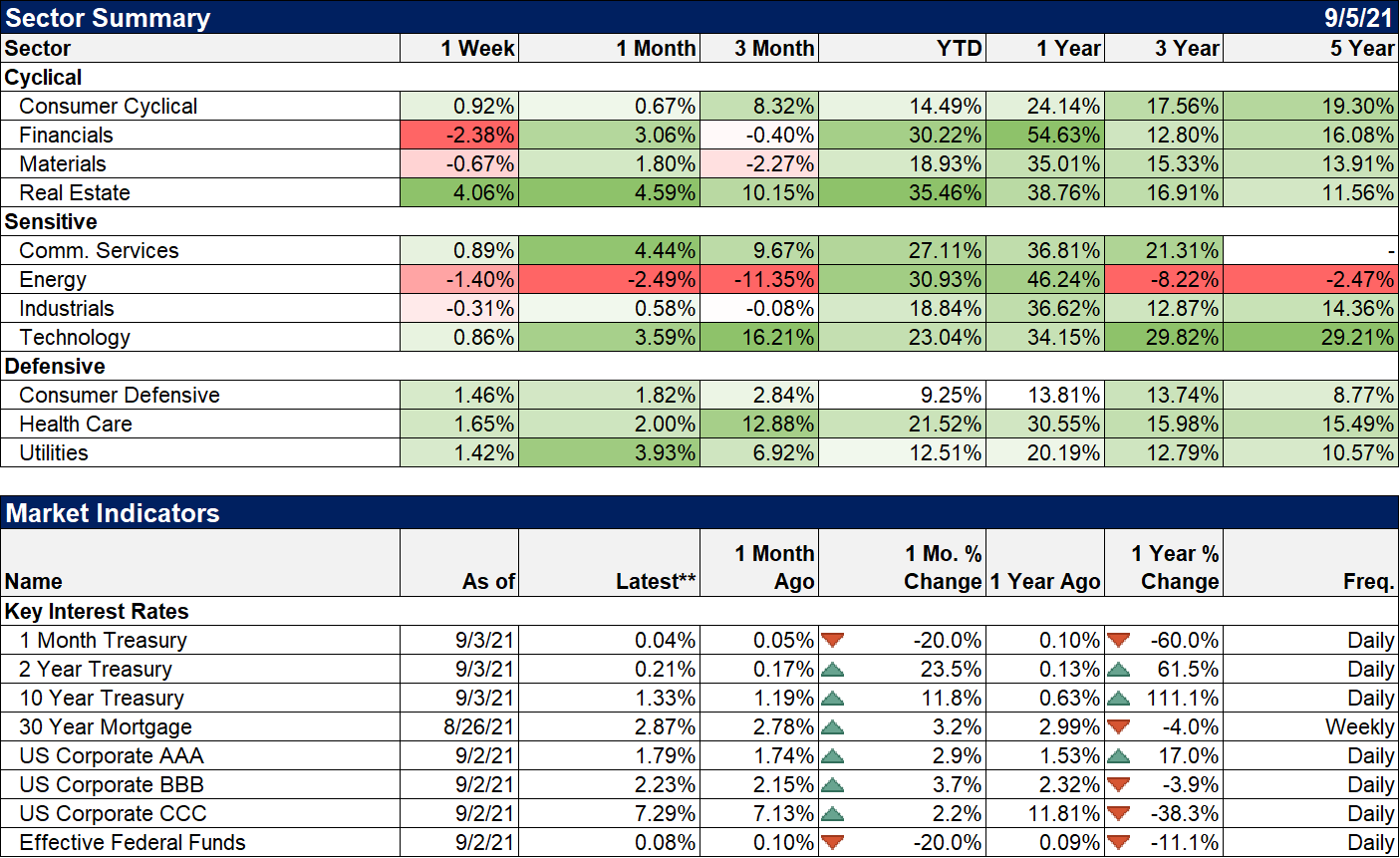

Large-cap growth is now ahead of large-cap value for the YTD but value is still leading in smaller stocks. I am still overweight value and don’t feel any urgency to change. The valuation difference has become too great to ignore and the gap will close eventually.

Financials had a tough week but if yields keep rising, that will probably change. Defensive sectors had a good week but continuation depends on the economy continuing to weaken.

There’s a lot of noise in the high-frequency economic data. Most of it is subject to large revisions that won’t be known for months or even years. It is not useful for investors except to confirm information the market has already provided. Bonds told us months ago that the economy was going to slow. Now it has but markets are already anticipating the next change in the economy. And so should you.

Joe Calhoun

Stay In Touch