Look around the poker table. If you can’t see the sucker, you’re it.

Warren Buffett

I actually don’t know if Warren Buffett was the first to say that and I’m not sure that’s exactly the right phrasing. When I sat down to write this I thought it was from Amarillo Slim, a professional gambler from Arkansas. Or maybe that other Arkansas gambler named Titanic Thompson who was allegedly the one who fixed the poker game that got Arnold Rothstein killed. Rothstein was, of course, the guy who famously fixed the 1919 World Series. I’ve also seen the quote attributed to Paul Newman but I think that is just because he was in The Sting. I’ve also seen it as “If you’ve been playing poker for half an hour and you still don’t know who the patsy is, it’s you.” But whatever the source or the exact phrasing or the reputation of the guy who coined it, it’s a great line.

Of course, none of that is important in the least, in the context of a weekly commentary about financial markets. That first paragraph is a distraction. I’d bet that there are more than a few of you who have already googled Titanic Thompson (who was indeed a notorious gambler from Arkansas) because you’ve never heard of him. A few of you have googled Amarillo Slim but as our demographic runs older, many of you have at least heard of him. And a few of you have gotten so distracted that you have just come back to read the rest of this after a half-hour detour into the Black Sox scandal (Shoeless Joe was the patsy). The internet may be a lot of things but a boon to productivity probably isn’t one of them.

One of the main themes of this weekly letter is to block out the noise of the financial press (professional and amateur). Most of what passes for economic or market news is just noise, distractions that take your focus off what is really important. The noise can be deafening and can prevent you from taking necessary actions or convince you to take unnecessary ones. And you certainly don’t need to waste any time listening to or taking seriously those market commentators who claim some clairvoyant ability. The future, today as always, remains unknowable and a large number of Twitter followers or podcast viewers doesn’t change that.

I have said repeatedly in these weekly missives that it is not our job as investors to predict the future and we don’t have to. It is our job to interpret the present and most of that boils down to observing what people are doing rather than what they are saying. And what they are almost always doing is acting very human, making the same mistakes their forebears did, being greedy when they should be fearful, and being fearful when they should be greedy. And reacting – overreacting – to the news of the day; listening to the noise and missing the market signals. Today is certainly no exception and in fact, may well be the most vivid demonstration of greed winning out over prudence in modern history. Or maybe just history.

I saw an article recently about how fund managers who are avoiding Tesla stock are being punished through withdrawals. They can’t keep up with the S&P 500 without owning Tesla but they don’t feel they can justify owning the stock from a fundamental standpoint and investors are cashing out. My first thought was that I would probably eliminate from consideration any actively managed fund that owned Tesla. Why? Because what Tesla would have to accomplish over the next decade to justify today’s stock price borders on the ludicrous. Tesla would have to dominate the global automobile industry to such a degree that most, if not all, of the rest of the industry would be bankrupt. No fund manager should own this stock voluntarily. To quote GHW Bush (and Dana Carvey and my wife), it wouldn’t be prudent.

Tesla is but one example of the degree of speculation in today’s markets. How about Rivian that recently went public and now has a market capitalization of $115 billion despite not having sold a single car? Or Lucid with a market cap of $90 billion and the same sales record as Rivian. Or QuantumScape, a research stage battery company with a $15 billion market cap and no revenue while Panasonic* has sales of $67 billion (including the batteries that move most of Tesla’s cars) and a market cap of less than $30 billion? NFTs? What about this “art” that recently sold for $3.4 million? Cryptocurrencies? Dogecoin, meant as a joke, has a market cap of $40 billion. Or Shiba Inu, a spinoff of the joke, has a market cap of $29 billion. No one is buying these things because they have some intrinsic value. They are only buying them because they think someone will come along and pay them more than they paid. The supply of greater fools is finite or at least I think so, but we obviously haven’t found the limit yet.

The problem with all this speculation is that it starts to tempt the prudent investor into reckless behavior. A recent tweet from David Andolfatto, an economist at the St. Louis Fed, helps explain how we got here. Calpers, the big California pension plan, recently voted on a plan to add leverage to its portfolio to meet its already reduced return target:

The board of the nation’s largest pension fund voted Monday to use borrowed money and alternative assets to meet its investment-return target, even after lowering that target just a few months ago.

Mr. Andolfatto responded with this tweet:

…this is a consequence of irresponsible behavior on the part of fund managers. Will they be held responsible should their levered bets fail to pay off?

No, it can’t be the fault of the Fed or other economic policymakers for pushing interest rates down to zero. It is the fault of investors, fund managers, and investment advisers who have to try and produce a reasonable return taking reasonable risks in this ZIRP environment. What exactly are investors supposed to do? If they avoid risk, they will get negative real returns, their purchasing power eroding by the day. What if a portfolio that produces an expected real return is beyond its risk tolerance or capacity? Does Mr. Andolfatto really think they’re going to just go broke slowly so the Fed can continue to execute a failed policy?

What about the fund managers and investment advisers? What are they to do? If they act prudently for their clients, the clients (some of them) will leave for an adviser willing to take more risk, chase more return. If they make “irresponsible” investments, which will likely be anything that went down in hindsight, they’ll get sued out of business. With all due respect Mr. Andolfatto, it is the Fed that has led us to this place, not “irresponsible” investors. They are merely responding to the incentives placed before them. When will the Fed be held responsible for its irresponsible monetary policies?

And that is why I’m on a bit of rant today about speculation and what is prudent. I said above that I wouldn’t own an actively managed fund that owns Tesla because it shows a disregard for the well-being of its shareholders. But what about an index fund that owns Tesla? What has always been prudent – owning a low-cost index fund – has now become a more speculative investment because of the degree of speculation in the market. How speculative? Well, I’m glad you asked.

The S&P 500 has become the default stock market investment for an entire generation of investors. It has become so embedded in our investment culture that few even bother to find out what they own; they just want to own “the market”. But is that what you get when you buy SPY? Consider these stats:

- The top 10 stocks in the S&P 500 make up 30.1% of the fund. Is this the diversification you expected when you bought an index with 500 stocks (actually 507)?

- These top 10 stocks have an average P/E of 43.7. Yes, that includes Tesla at 137 times earnings (based on data from Morningstar) so if we take that out the average drops to…33.3.

- The top 20 stocks in the index make up 38.9% of the fund with an average P/E of 38.3

- The top 25 stocks make up 42.2% of the fund with a P/E of 34.6

- Two of the stocks in the top 10 are different share classes of Alphabet (Google). So you really have 30% of the fund is just 9 stocks. Furthermore, if you exclude JP Morgan and Berkshire Hathaway, you have 27.6% of the fund invested in 7 companies: Microsoft, Apple, Amazon, Tesla, Alphabet, Meta Platforms (Facebook), Nvidia (chip maker for crypto mining). Do you think those companies will be in the top 10 a decade from now? Only 4 of the top 10 from 2011 are still in there. Only one stock from the 2000 top 10 remains (Microsoft).

The current concentration of the fund is unprecedented. Its long-term average is about 18% in the top 10. It reached 26 during the dot com mania. Is it still prudent to use this fund as your main equity exposure?

My job is not to just buy stuff that I hope will go up. It is not to buy stuff that has gone up already in the hopes that it will continue to do so. It is not to buy the stuff that is most popular on Twitter. My job is to act as your agent, as your fiduciary and follow the prudent (wo)man rule that requires us to “to observe how men of prudence, discretion, and intelligence manage their own affairs, not in regard to speculation, but in regard to the permanent disposition of their funds, considering the probable income, as well as the probable safety of the capital to be invested.” A lot has changed since the prudent man rule was first introduced in 1830. We can buy risky or speculative investments in the context of a diversified portfolio as long as the portfolio as a whole conforms to our understanding of the risk tolerance and capacity of the client. But what must a fiduciary do if an investment previously identified as prudent no longer fits the bill? The answer to that question is not simple but the short one is that that investment can no longer occupy the same percentage of the portfolio as previously. If the client’s risk tolerance hasn’t changed, the investment must. And by the way, that has nothing to do with whether it rises another 10, 20, or 100% from here.

There are ways to invest these days while sticking to a prudent person mandate. But it is a dwindling list of investments that fit that bill and we are at such extremes now that I think a cash reserve (or very low duration bond portfolio) is a requirement. Yes, there is the risk that you may lose some purchasing power but that risk pales in comparison to the risks of owning the most popular stocks. Doing what is prudent is not easy and it is harder when meme stocks, ridiculous NFTs, and joke cryptocurrencies are making some people rich or richer. It isn’t easy being the party pooper. But someone has to do it. The Fed sure isn’t interested in the job.

*Alhambra clients and employees own Panasonic stock.

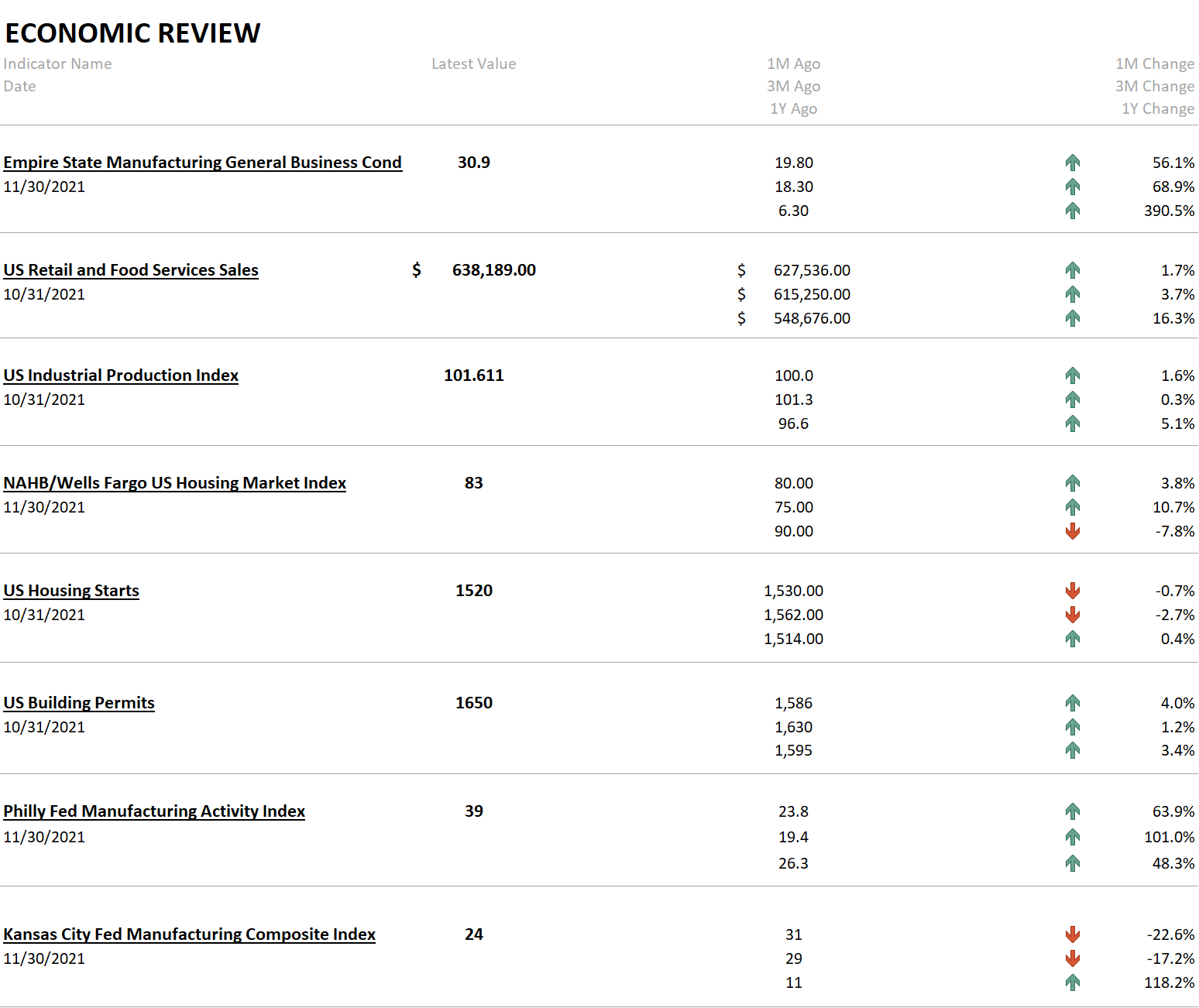

The economic news last week was pretty uniformly good with retail sales, industrial production, and the housing market index all better than expected. The Empire State and Philly Fed surveys were also quite a bit better than expected. Housing is still a weak link but the rising HMI and permits allow some optimism.

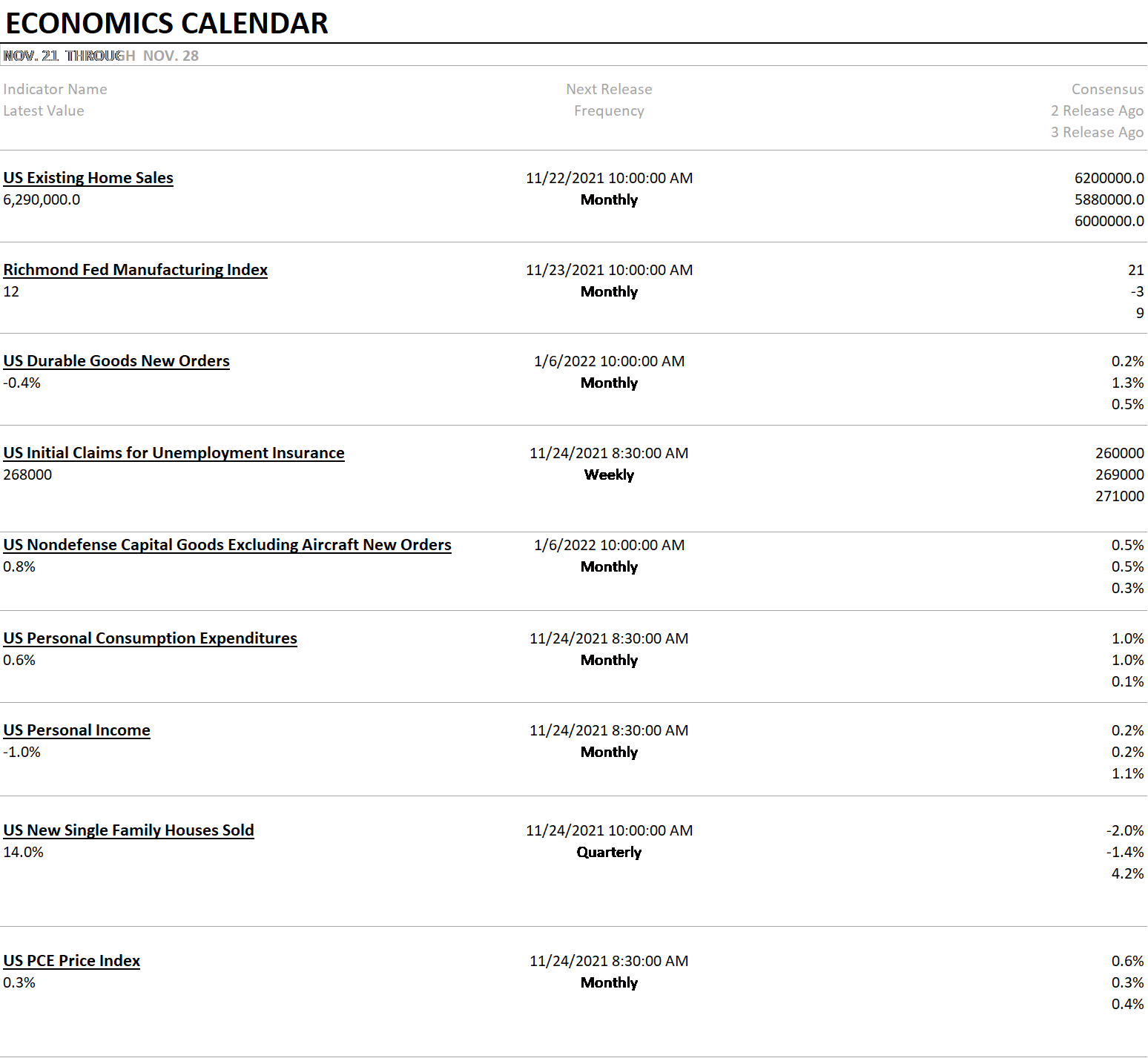

It’s Thanksgiving week so there are no economic releases on Thursday or Friday. All markets are closed Thursday and stocks trade a half-day on Friday. The important reports next week are probably durable goods, non-defense capital goods, PCE and personal income, and PCE inflation.

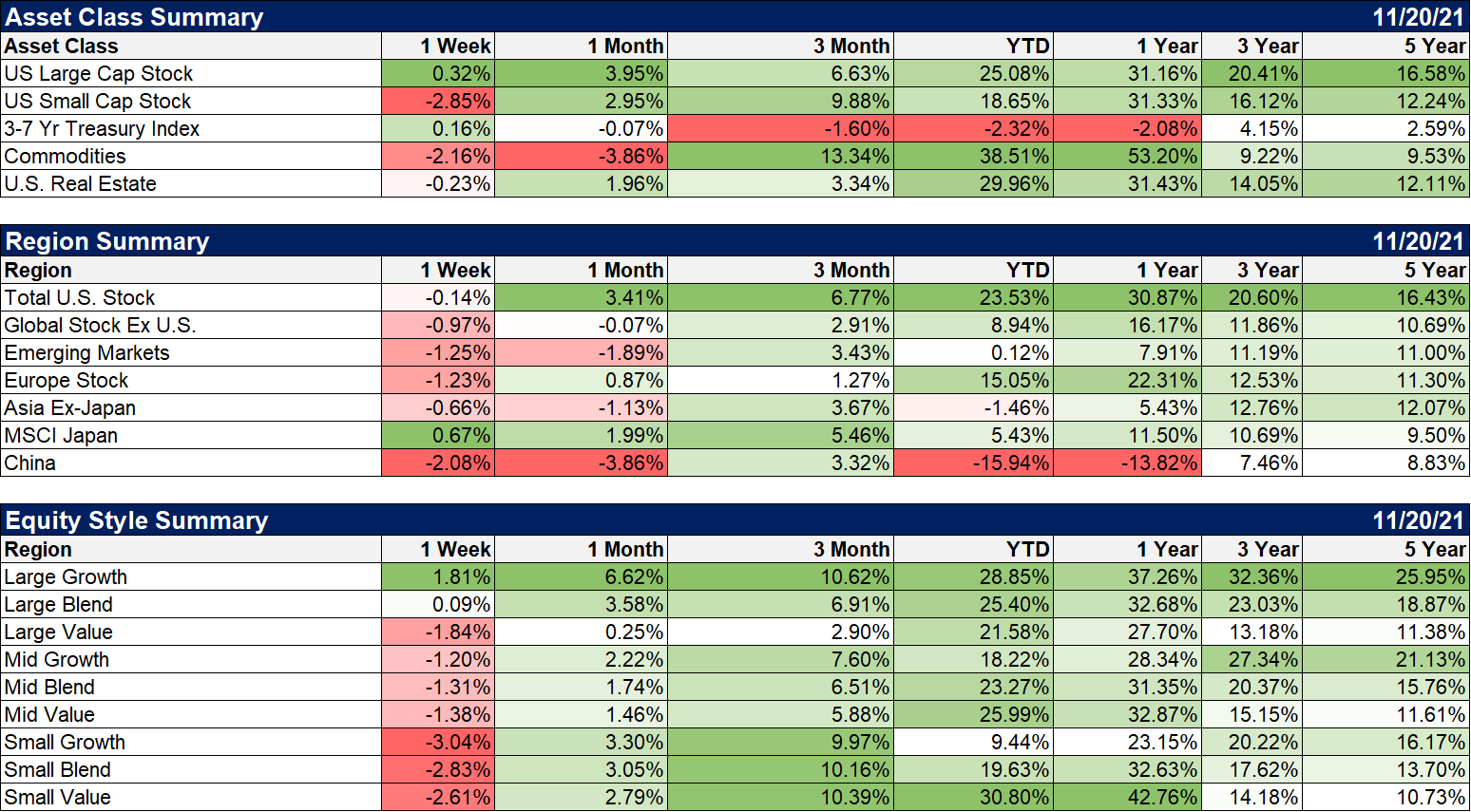

Stocks were generally lower last week and bonds were up a bit. Commodities took an even bigger hit as crude finally started coming back to earth. Foreign stocks did worse than the US with the exception of Japan, which was up 2/3 of a percent. Growth generally won on the week but only large growth finished the week in the green.

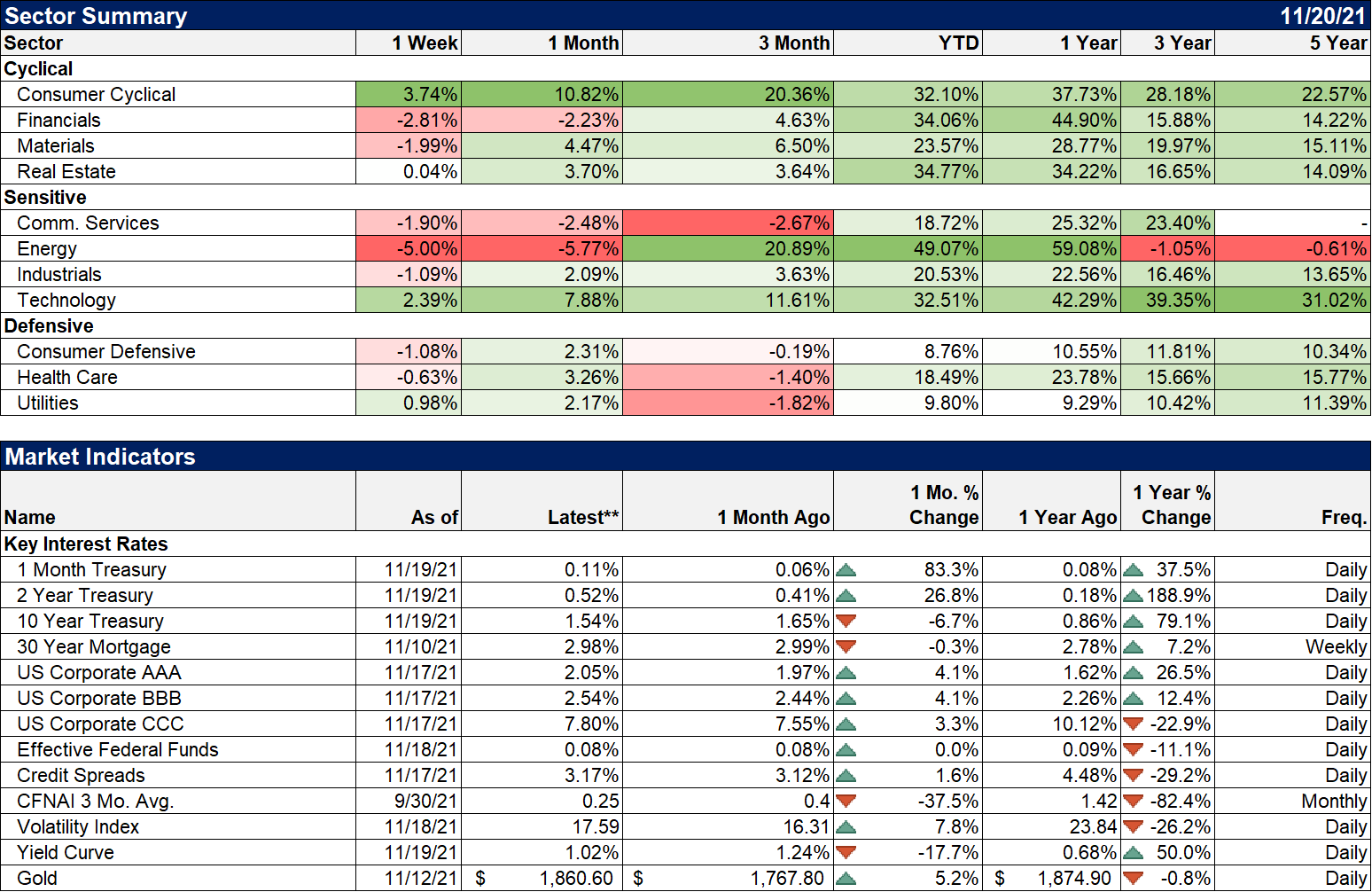

Energy got whacked with crude and financials are starting to feel the flattening of the yield curve. Technology, shocker, was up on the week.

There are a lot of market players out there today wondering who the sucker is, who’s gonna play the patsy. There are plenty who say it is those of us trying do the right thing, trying to actually analyze investments before we invest our hard-earned dollars. I saw a tweet from some twit this week that said:

Fun Fact: Did you know there’s still some people that don’t know the entire market is driven by options and liquidity, and they still think fundamentals matter? Crazy, right?

The person who wrote that has no idea why we look at fundamentals. He thinks we look at fundamentals to judge whether an investment will rise or fall. That isn’t it at all. Fundamentals cannot tell us whether an investment will rise or fall because it isn’t fundamentals that move stocks or markets. It is perception, what people believe about a company or a stock that moves the price. Fundamentals can’t move markets because most people in the market – like this twit – don’t know what the fundamentals are. ROE? What’s that? But fundamentals do tell us about risk. Think of fundamentals as the odds posted on a football game or horse race or a game of chance. Now ask yourself, would you ever make a bet without knowing the odds? So who’s the sucker?

Joe Calhoun

P.S. I started trading options in 1987. I know a thing or two.

Stay In Touch