At the end of last week, the Bureau of Economic Analysis reported data on US Personal Income and Spending that hit every sour note. There was the lowest inflation rate, the deflator to those spending figures, in years as well as the clear need to officially anoint a successor to the Verizon madness. The release also featured residual seasonality, and, most of all, even less of full employment than there had been at any time last year (which was never much).

Small wonder the President’s chief economic advisory Larry Kudlow was on CNBC Friday demanding an immediate 50 bps rate cut from Jay Powell. The need for a scapegoat is becoming perfectly clear.

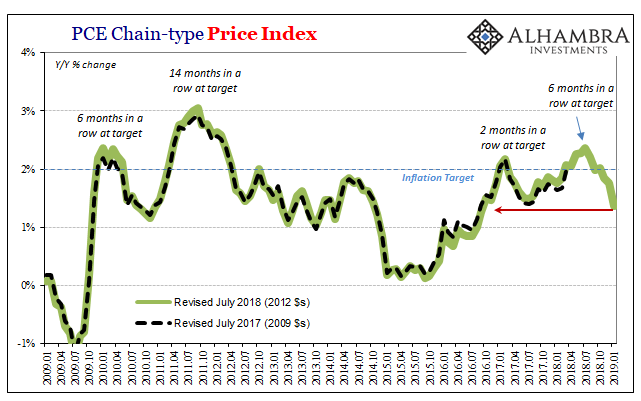

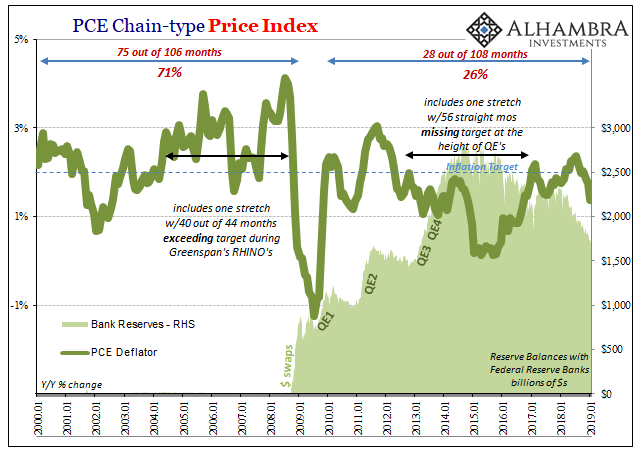

Taking each sour note in order, the BEA’s PCE Deflator index rose just 1.37% year-over-year in January 2019. According to this the Federal Reserve’s preferred measure of consumer inflation, monetary policy hasn’t been this far off target since September 2016.

In the parlance of the central bank, the newer dovish language version, inflation pressures do remain suspiciously “muted.” However, even that term is in danger of being revised. The way the index is going suggests a lot more than unfavorable oil price comparisons.

It is too early to know for sure, but there is quite a bit to suggest broad economic deceleration. What policymakers consider the worst case, outright deflation, is the point at which businesses are forced to mark down the prices of their products due to lacking demand. An inventory problem that spirals out of control, or what Economists call insufficient “aggregate demand.”

Consumers buy less goods, inventories pile up forcing companies to liquidate them as best they can at whatever price moves it out of their hands, which in turn convinces consumers to pull back spending even more as they begin anticipating nothing but lower prices for the future. It is a downward spiral from there.

This process needn’t play out in that worst case, however. There is tremendous potential for real economic weakness at much lower levels of imbalance and psychology. Inventory problems have historically been the trigger for recession even when it never reaches the full deflationary proportions. Those are often detectable by inflation indices.

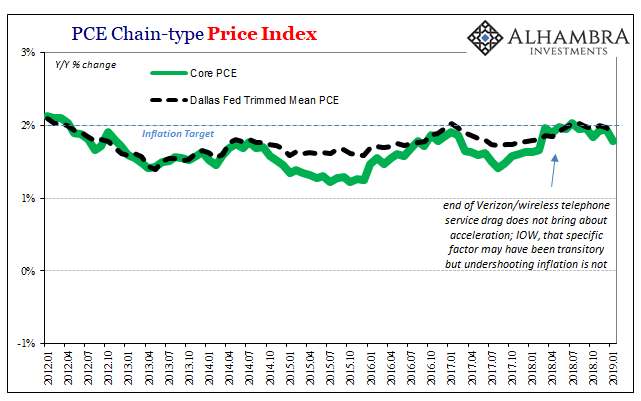

The so-called core inflation rate applicable to the PCE data increased by just 1.79% year-over-year in January. This was down from 1.95% in December and was the lowest since last February when Yellen, Powell, and all the rest had been blaming Verizon. They were, actually, right to do so meaning that the wireless data wars of 2017 and what was left of them in base effects in 2018 were responsible for wiggle in the core PCE Deflator. But the end of those base effects didn’t necessarily mean what they wanted (more visible underlying price acceleration).

The more immediate conundrum is how core rates like the headline can be so “weak” with the unemployment rate still less than 4%. If calculated inflation rates are significantly less in 2019 than the rates of 2018, what has changed? If the answer was economic breakout, as has been predicted, then inflation should have accelerated everywhere including the core numbers. The opposite means Jay Powell is going to need to locate a scapegoat himself, Verizon, obviously, will no longer suffice.

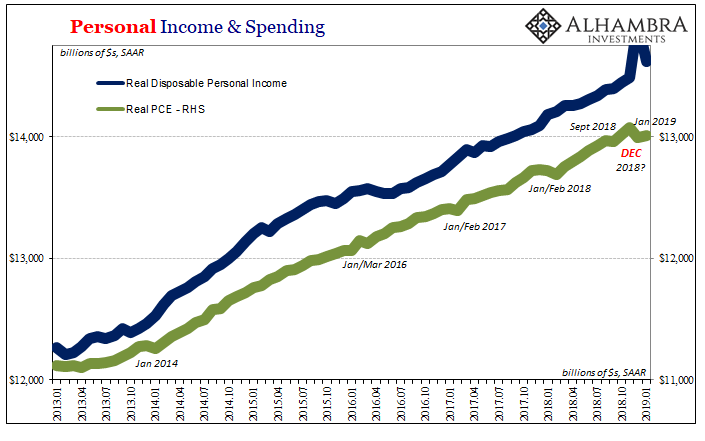

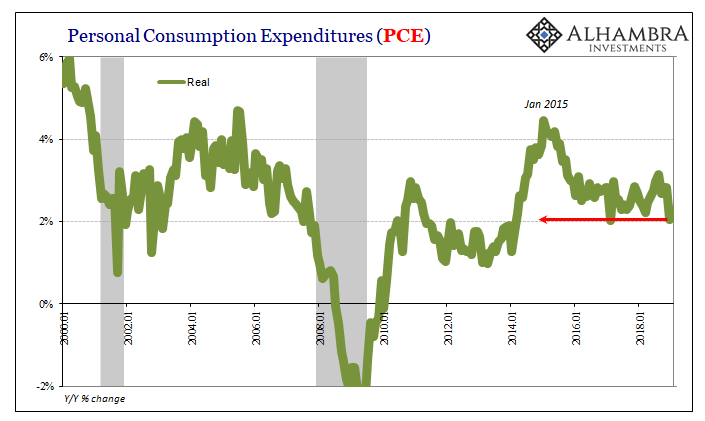

We are drawn to inventory simply because of residual seasonality (which isn’t a residual, though it is very clearly seasonal). As noted last month, the Personal Spending section of the data confirmed the disastrous 2018 Christmas season. This updated series, Real PCE, for January adds the expected residual seasonality (weakness in the aftermath of Christmas) to what was already an important slipup in holiday spending.

For the second month running, Real PCE was unusually soft. Year-over-year, the growth rate was just 2.29% in January following 2.05% in December. These are the lowest consecutive monthly increases since 2014.

Given how retailers and the rest of the supply chain below them were almost certainly primed and ready for a truly awesome Christmas experience, the word “boom” couldn’t have been used any more than it was all throughout 2018 right up until the middle of December, this would’ve been a complete shock. Throw in some market turmoil to add to the confusion and uncertainty, and it is no wonder on the surface things throughout the economy are becoming a little more unstable.

It’s actually consistent in this way; if businesses seem more uncertain about topline growth and the state of consumers, consumers might be even more uncertain about the labor market. For all the constant talk of the unemployment rate and wage-driven inflation, there would (should) have been a very clear response first in nominal incomes.

You don’t need an Economics degree (it often helps if you don’t have one) to understand the process: if wages are rising quickly, and more workers are working more, incomes have to surge because that is the end output of this most beneficial economic trend.

It’s just not there – it has never been there. For as long as the unemployment rate has been below contemporary estimates of “full employment”, estimates that have to be constantly downgradde as the unemployment rate goes lower, nominal incomes continue to advance at subdued rates anyway.

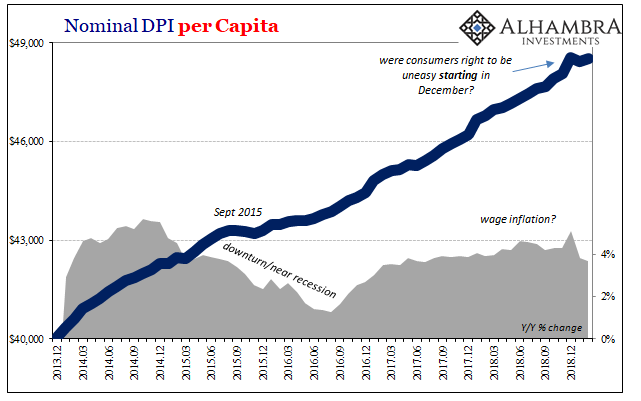

In February 2019 (note: the BEA has released February estimates for most of the nominal series; the real data remains one month further behind because the PCE Deflator has yet to catch up from the government shutdown), nominal DPI per capita rose by just 3.67% year-over-year. That’s down sharply from 5.08% in December, February’s rate the lowest since the summer of 2017, suggesting consumers may have been right to become concerned about the real state of the labor market heading toward 2019.

These are all short-term indications right now but they are starting to pile up across series (and even agencies). Recall the shockingly weak payroll report last month, the headline figure nearly flat. From inflation to spending to income to that BLS data, on top of markets reacting in real-time, there is a lot of short run consistency that points to at the very least serious and growing uncertainty.

If they aren’t already, scapegoats are almost certainly going to be in greater demand than rate cuts.

Stay In Touch