The administration continues to plead for rate cuts. I think they understand the gravity of the situation, if not quite the situation itself. The President’s chief economic advisor, Larry Kudlow, was back at his old TV home on CNBC today. In the wake of more “muted” inflation figures one quarter of the way through 2019, Kudlow said:

The inflation rate continues to slip lower and lower. Even according to the Fed’s own spokespeople, from the chairman on down, that could open the door to a target rate reduction.

This is actually a much bigger problem than it may seem. The issue doesn’t end with monetary policy constraint. Last year, for several years now, Economists and central bankers have been predicting a noticeable pick up for inflation. It was more than their justification for “rate hikes.”

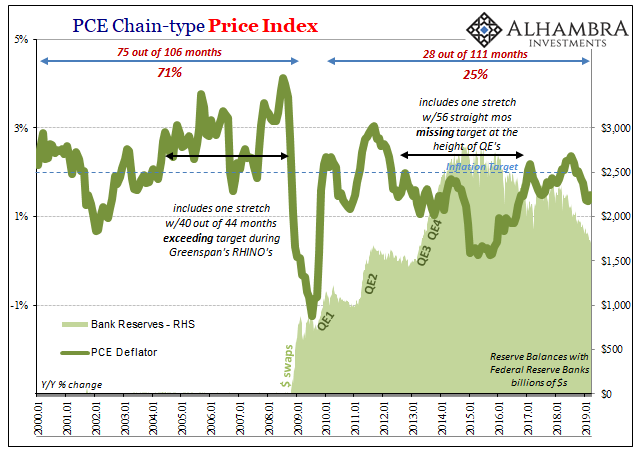

Inflation would have confirmed their economic understanding. QE (in the US elsewhere) created the virtuous recovery circle which was presumed to have been nearing completion. Thinking it was money printing, consumers bought more than they would have and businesses invested the same way (expectations management). This pump priming, as Keynes called it, led to a reduction in economic slack.

Eventually, this fixed macro factor should have led to wage-driven price increases, the competition for scarce workers being passed along to consumers. The PCE Deflator gets up to 2% and stays there. The Fed comes in with rate hikes to make sure it doesn’t get out of hand.

Cue Disney ending.

The lack of inflation, therefore, doesn’t just let the Fed off the hook for further hikes; or even give them margin for rate cuts as Kudlow wants.

What the President should be considering, and I think he already has, which is why he’s made the Fed the central focus for this economic debate (the real rationale behind Kudlow’s repeated public requests), is what must be wrong given these circumstances. Why has the mainstream economic message broken down?

The inflationary scenario would’ve confirmed the boom everyone was so sure of just a few months ago. Some people breathed a sigh of relief on Q1 2019’s GDP report, but far fewer than they might imagine. There was much more wrong with GDP as right.

Without inflation, you have to question the whole premise. You can’t be so wrong for so long about something so intrinsically basic. If you are, and the recent numbers confirm, you wouldn’t have any idea whether the economy is really strong, or really weak. The one thing you have been depending upon for confirmation isn’t cooperating at all.

What Kudlow is saying, if you believe his R* stuff, is why not? Cut rates Jay Powell because you can’t justify not cutting them. There is enough economic uncertainty and no longer any basis for the whole overheating scenario. To begin with, this is already a very different outlook than just a few months ago.

The politics is far more ruthless. Cut rates or be blamed for the negative consequences that certain very important markets are forecasting for the not-too-distant-future.

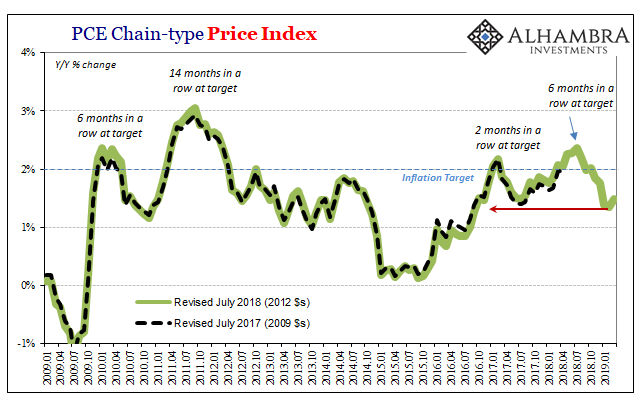

The PCE Deflator accelerated only a little in March 2019 from the lowest in years registered during February. And that was with a small oil price tailwind. According to the BEA’s measure of consumer inflation, in general prices rose 1.49% year-over-year last month compared to 1.34% the month prior.

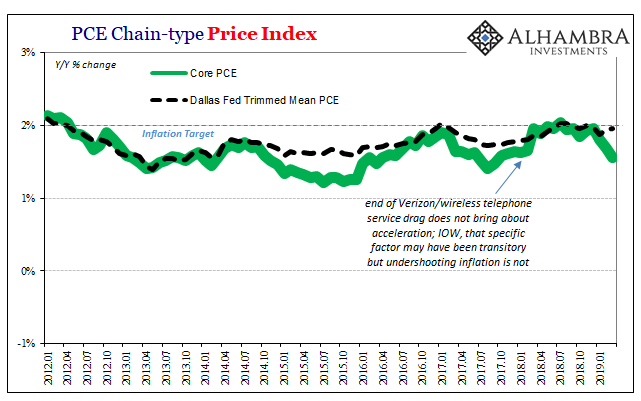

Of more concern for the US central bank, the core inflation rate dropped to a multi-year low of just 1.55%. Unlike the last time this happened, there is no Verizon to immediately (and wrongly) blame. Inflation undershooting, it seems, remains the base case – which totally undermines the argument. The economic paradigm was supposed to have shifted to something different, much better in 2017 and 2018 than at any point over the previous ten years.

Instead, more and more it is confirmed nothing changed. That’s a big problem way, way beyond these federal funds rate exercises.

Larry Kudlow is right about one thing. Jay Powell has no excuses, especially not after the last few years of public assurances. If only someone would honestly investigate why it never works out the way the central bank promises.

Stay In Touch