The key has always been the first part of the word rather than the more common focus on the second. A eurodollar is more about the “euro” than the more obvious monetary denomination. Since it began decades before Europe created its common currency, the eurodollar has nothing whatsoever to do with the euro. But those four letters mean absolutely everything. The whole world’s fate remains tied to them.

In its earliest days, it was simply called the Continental dollar. For various and perhaps competing reasons, at some point in the fifties there arose a robust trade of US dollars throughout Europe. Thus, “euro.”

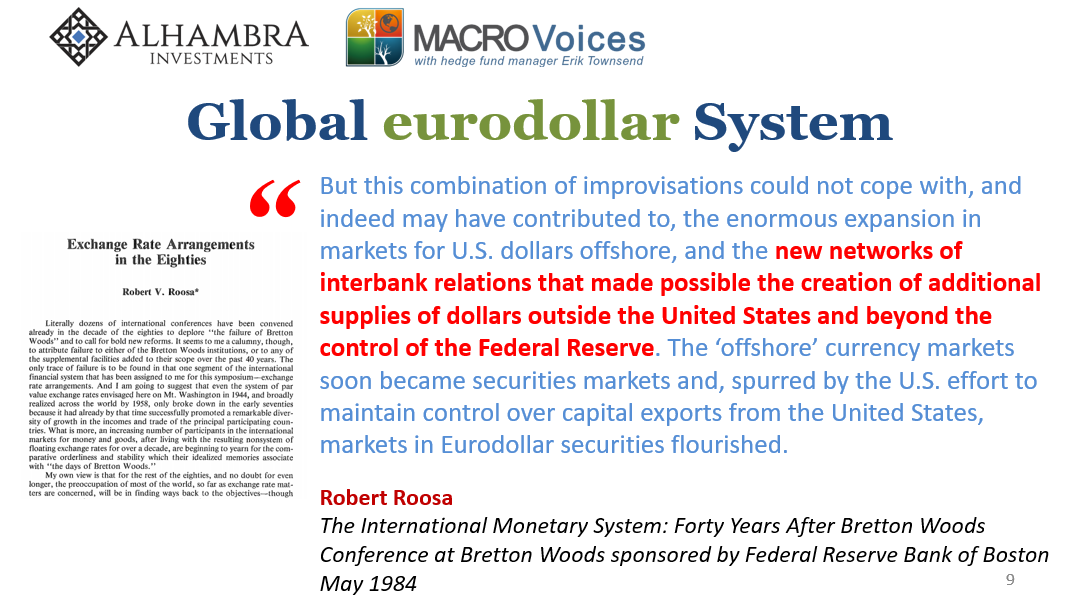

As the clear surviving successor for global reserve currency business, the British pound unlike the dollar didn’t truly make it beyond the thirties, and with European convertibility (and economic uncertainty) not yet restored, these baseline conditions of the time meant the usefulness of US dollars in Europe seemed obvious. The implications were not.

It was the premiere of a new way of doing global finance, this credit-based currency regime untethered (largely) to national interests and unbothered (largely) by international borders. The earliest official reference to the eurodollar market (that I’ve yet been able to find) written in 1960 spells out what had become even by that early date common practice:

In many European banks the manager of the bank’s money position is also the chief foreign exchange trader, a practice which is virtually unheard of in the United States and which indicates the close link in Europe between money and foreign exchange markets.

A truly global dollar, a global monetary system. Dollars outside the United States.

Fast forward to late 2007, and suddenly this worldwide system which up until then had been only too happy and willing to supply these eurodollars in overabundance suddenly became shy. Very, very shy.

As a consequence, the Federal Reserve belatedly remembering that its first duty – never mind the modern dual mandates – is currency elasticity in December 2007 it tried to offer some. In those first TAF auctions the bidders for the Fed’s liquidity were an odd collection, certainly not what one would have expected from the typical college courses on money and Economics or from what was always talked about in public and on TV.

I wrote about TAF a few months ago on the latest anniversary of August 9:

When the first one was conducted on December 20, 2007, we can now see that the first name on the list is Citigroup. As a courtesy, it seems, the big NYC bank had bid for a minimal $10 million.

The biggest borrowers, though, were other sorts of ostensibly New York banks; firms like, Landesbank Hessen-Thurin, Bayerische Landesbank, Dresdner Bank AG, Deustche Zentra AG, Landesbank Baden Wuerttemb, and WestLB (the LB stands for, as you probably guessed, landesbank). Those six “New York” banks alone accounted for half of the $20 billion allotted. Given the style of these names, you might already be sensing a theme.

Add the $2 billion which went to Dexia and the $1.4 billion handed to BNP Paribas Houston, that’s $14.3 billion out of $20 billion heading to US subsidiaries of overseas institutions in the first major overt liquidity act of the GFC.

Forget about all the complexities contained within these shadow money concepts for a moment. There’s also another dimension to the system that goes perhaps unappreciated, the very one that some of the experts and commentators of the missing money seventies had been warning about.

Since “euro” means offshore and offshore means not the US or anywhere else, who is ultimately responsible for what has been from its very beginning a complete monetary system?

No one and everyone. There’s no backing or authority yet we all share in the consequences. Except central bankers and Economists, of course.

In August 2007, for example, when the crisis first erupted the FOMC discussed how this stuff just wasn’t their job. Though the problem was dollars and dollar funding, in the opinion of the central bank’s experts these were “London banks” out there increasingly naked in the eurodollar markets.

Here’s one how one staff economist at the FOMC meeting in September 2007 characterized the situation:

MS. JOHNSON. So the spreads of overnight pound LIBOR, relative to target, opened up widely, and they were not addressed. They were allowed to just sort of sit there. The term pound market had a problem, too. Of course, many of the dollar issues that we have spoken of— and that Bill talked about—are really being captured as a London phenomenon. But you might say that, from the point of view of the Bank of England or the U.K. economy, these dollar issues are somewhat separate from the domestic economy. There is some truth to that, but also the institutions are involved, the institutions have obligations, and the shocks to the institutions reverberate back into the domestic economy, it seems to me. [emphasis added]

Did they really expect the Bank of England to step in the eurodollar market to supply – dollars? It appears so.

It goes back to the original question. Is the Fed’s job the dollar, or the US banking system? It seems like it should be an easy question to answer, but the very fact that there was a bank panic proved how unready policymakers were to even ask it. They had no answers because, to that point, it was just never considered. Banks were banks and money was money, all of it following the clear, bright lines set forth in every single Economics textbook in print (many of which were written by central bankers).

The word offshore, the term “euro” in front of dollar, was a deeply fundamental factor that hadn’t ever been fully reckoned. Being utterly unprepared for a global dollar crisis was how we got the Global Financial Crisis. Why were German and British banks being nationalized left and right, why were Japanese banks begging BoJ (and the BoJ begging the Fed) for dollars over what was reportedly a US housing bubble?

Thus, TAF auctions and overseas dollar swaps. Oh, and the constant focus on subprime mortgages as the supplied villain for the crash. It was true “Wall Street” had been reckless, sure, but more so the Fed if for very different reasons.

It is as much a political issue as monetary. What to do about money without borders? A thorny topic before even getting into the details.

Yesterday, the Financial Times reported that the Federal Reserve has agreed to set aside rules it was contemplating which would have imposed strict liquidity requirements on domestic branches of foreign banks.

The Federal Reserve will announce on Thursday that it has decided against forcing US branches of foreign banks to hold a minimum level of liquid assets to protect them from a cash crunch, according to people familiar with the decision.

While most of the public remains unaware of who, exactly, was showing up at the TAF auctions nearly twelve years ago it didn’t go totally unnoticed behind the scenes. It did take more than a decade for that to lead somewhere, though.

The proposed measure, from what I can tell, was a narrow one intended to make sure that all those German-sounding names wouldn’t cause so much trouble the next time around. Foreign institutions were desperate for dollars in the eurodollar market the last time, so authorities think it will make a difference to force their domestic subs hold to some artificially created liquidity number this time.

Though somewhat on point, it misses the point. And now it has been rendered moot. The Fed has punted the issue over to international regulators. One reason why:

A senior executive at the Wall Street arm of one European bank said he was hoping to see a recognition that foreign subsidiaries benefit from “significant extra resources” that their parents can deploy in times of difficulty.

There’s a couple of big things wrong in this statement that get to the heart of the matter. First of all, the whole reason Hessen-Thurin and Bayerische ended up at TAF was because their parents were being shut out of the eurodollar markets offshore.

They ended up using these domestic subs as a bypass or workaround, hoping to be able to find some domestic dollar funding which would then go the exact other way – foreign parents trying to benefit from TAF resources and the like that their subs could scrape together in times of difficulty.

The Fed appears to have it backward (again). The problem wasn’t ever domestic subs operating exclusively in the US, it was those funding markets outside of it.

The bigger problem, as I see it, is that the Fed despite what looks to be official recognition of a global monetary system is still compartmentalizing. They still don’t account for offshore, apparently willing to continue to treat US subs of foreign banks as US banks totally separate entities from those foreign parents.

What happens outside the US border, to the Fed, isn’t a dollar problem, it continues to be someone else’s problem. They care only about the US banking system as if any implications end at the US border. Or that trouble outside of it, in dollars, won’t land here.

As I wrote at the outset, the key part and therefore maybe the first step toward getting past 2008 finally is to fully appreciate and recognize that this isn’t some separate, firewalled system which incidentally happens to reach into everyplace around the world. The US banking system wasn’t the problem in 2008, the global dollar system was.

It is truly a global matter whether that comports with anyone’s laws and commonly accepted official practices.

If that means rewriting statutes and gaining international cooperation, then rewrite the statutes and gain international cooperation (for the record, I’m not advocating the Fed take over the eurodollar system, far from it; just that someone politically needs to step up and take some responsibility so that it can be reconstructed). Continuing to view the eurodollar system as some externality will only lead to more of the same.

As we were reminded a little less than a month ago. What was that repo rumble? Jay Powell wouldn’t know. Especially if, as I suspect, it had some origins (collateral) offshore in the “euro” part of the “dollar.”

Stay In Touch