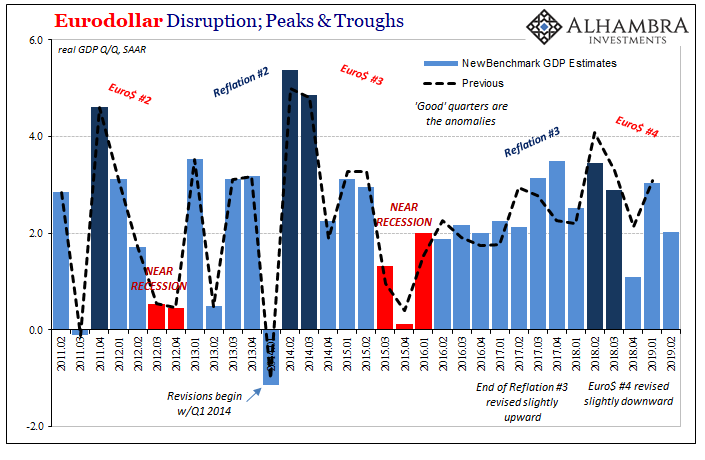

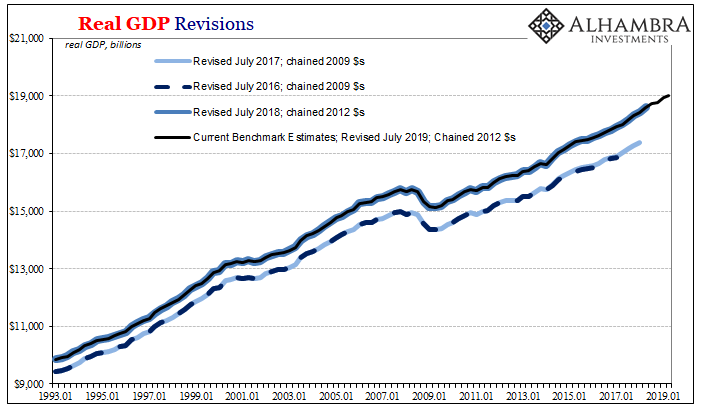

It usually takes them a little while, a couple of benchmark adjustments to better conform to the true shape. Today’s GDP report included the latest revisions to the underlying data. Overall, not much changed. The changes are applied to Q1 2014 and forward, upping Real GDP growth slightly in 2015, adding a little bit more to the tail end of Reflation #3 in 2017, and them taking some away from what’s recorded so far under Euro$ #4.

Most noticeably, that last 4% quarter (Q2 2018) is now gone and the landmine (Q4 2018) really hit hard. Originally thought to be 2.6% and quite a relief given what happened October to December, the Bureau of Economic Analysis now says the final quarter of last year managed just 1.08%.

The new figure for Q2 2019 came in at 2.035% (continuously compounded annual rate). That was better than consensus, but many positive comments discount the change in direction. Over the last three quarters GDP growth is barely 2%. For the prior five dating back to the end of 2017, it was better than 3%.

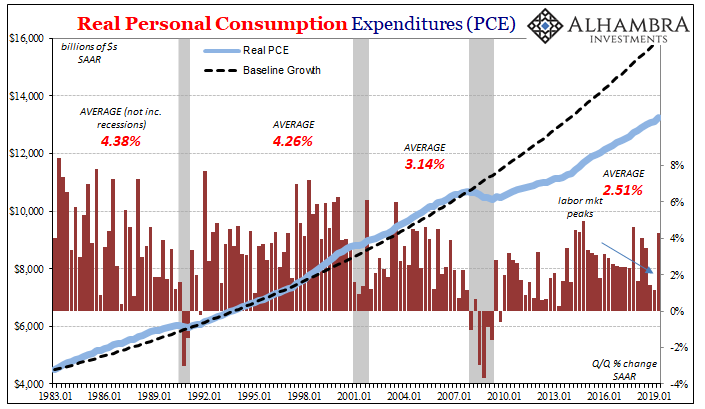

On the plus side in Q2, what held the figure from repeating Q4 was Real PCE. Consumer spending had been worse than originally thought in Q1 and then bounced back in Q2.

This isn’t at all unusual, and it’s not the basis for underlying strength. PCE expenditures are and have been noisy ever since the middle of 2017. Since the labor market peaked way back in 2014, the trend in consumer spending has tracked lower like the jobs market (unemployment rate aside). At times, like Q2 2018 or Q4 2017, there’s a temporary splurge.

The lack of consumer spending has been one reason why the globally synchronized growth upswing in the US economy remained subdued when compared to the prior one. Reflation #3 overall was less than Reflation #2 and the labor market/consumer relationship was a big reason why.

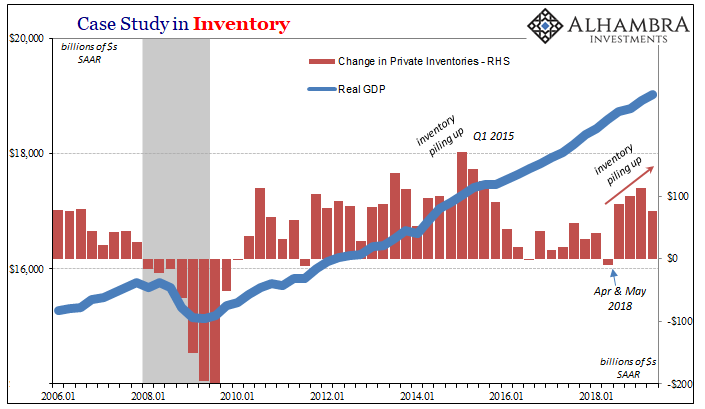

It begins with inventory. Though a reduced pace of inventory piling up subtracted from Q2 GDP, it was still a substantial increase despite the PCE bounce. It adds more color to what we are seeing in the manufacturing sector (PMI the lowest since 2009).

Therefore, for PCE to become the foundation for a second half rebound something meaningful would have had to change the situation. The labor reports suggest it has – in the wrong direction.

That’s a problem because the rest of the fundamentals outside of this one quarter’s PCE indicate growing retrenchment – starting with consumers.

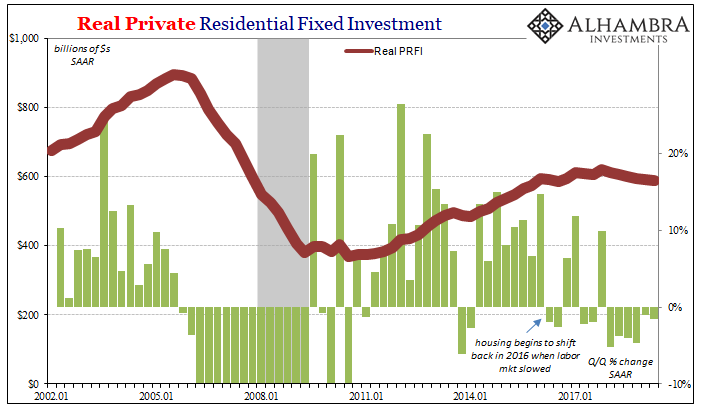

Housing has been subtracting for six straight quarters, and has been weak and unsteady going back to Euro$ #3. Obviously, by itself that’s not a big deal. As a proportion of GDP and the real economy, because home construction has never recovered from the last bust this sector isn’t nearly as big a proportion as it used to be.

In other words, housing isn’t going to be the cause of a recession or downturn (even so, you better believe the Fed is nervously watching this go on and on). Instead, its significance lies in what it says about consumer attitudes. Like the underlying baseline in PCE noted above, home construction indicates entrenched caution – which gets back to the expectations for what comes next.

I never thought I’d requote the NAR’s Larry Yun, but quite by accident he really got it right this one time:

Either a strong pent-up demand will show in the upcoming months, or there is a lack of confidence that is keeping buyers from this major expenditure.

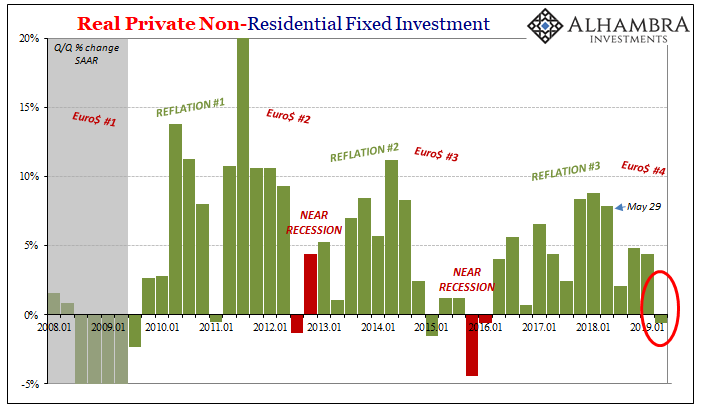

Unfortunately for Jay Powell, this thought process applies to a lot more than housing or even consumers. It is doubly true for businesses. The most concerning aspect of the GDP report continues to be a slowdown in private non-residential fixed investment (PNRFI), better known as capital expenditures or capex.

For the first time since the trough of the Euro$ #3 downturn, PNRFI was negative Q/Q in Q2 2019. Not only that, businesses are following what is a clear and established pattern.

It is the domestic component to what is already a pretty-well (though belatedly) established chain-of-events. Issues in the financial system, meaning liquidity, tend to hit capital-intensive sectors first and most. Capex is sensitive and susceptible.

That’s why PNRFI turned negative in Q1 2015 ahead of what would be a substantial downturn.

The larger problem, however, remains exactly the same. There is no accounting for the real baseline condition. No matter what GDP is or is not in each quarter, the mainstream perception is an economy that may be experiencing some small and temporary issues though it is otherwise in very good shape.

No one can really tell what Fed officials are talking about with R*. When you break it down, though, it’s pretty simple:

This is where the analogy [of central banks as auto repair shops] fits best; if something “needs” to be repaired for a prolonged period of time the person or group conducting the repairs really doesn’t know what’s wrong or how to fix it.

Not so, says the monetary mechanic. The counterpoint is the status of the vehicle undergoing examination. You may see a fine and workable economic automobile with low mileage and little wear. But to top mechanic Draghi [or Powell], what you’ve brought to him is an old, dilapidated piece of junk held together by duct tape and chewing gum.

Of course it needs constant maintenance.

This is the essence of the argument, the pseudo-intellectual foundation of what’s called R* (or R-star).

This lack of understanding contributes substantially to economic confusion – how come a healthy economy can never seem to sustain itself. Why aren’t 4% quarters the norm, and 2% quarters the rarity they used to be?

In the absence of any explanation, because officially none is required, the economy an old junker car in need of constant maintenance, people are increasingly filling in the blanks with their own perceptions; and then acting on them politically and socially.

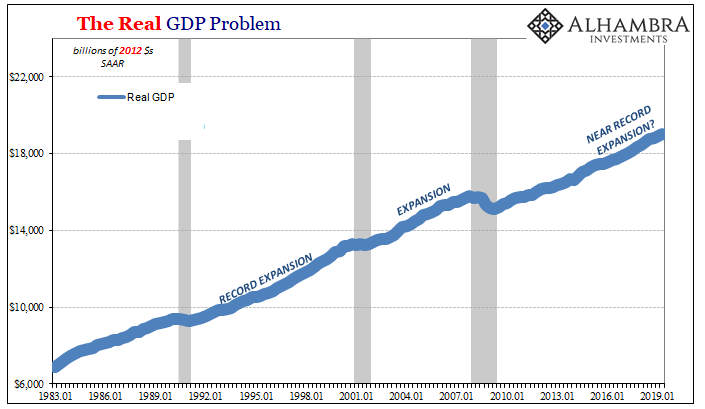

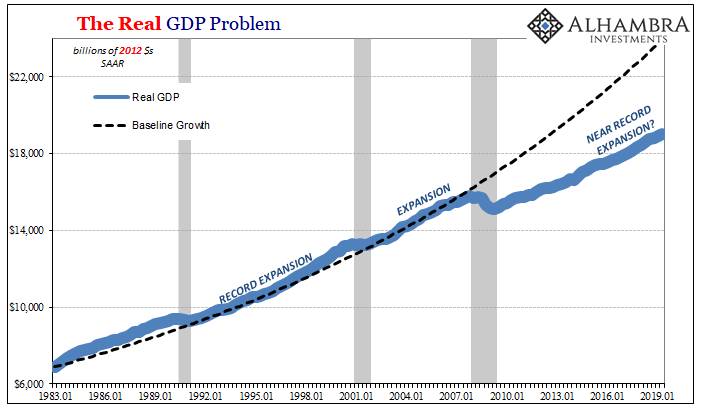

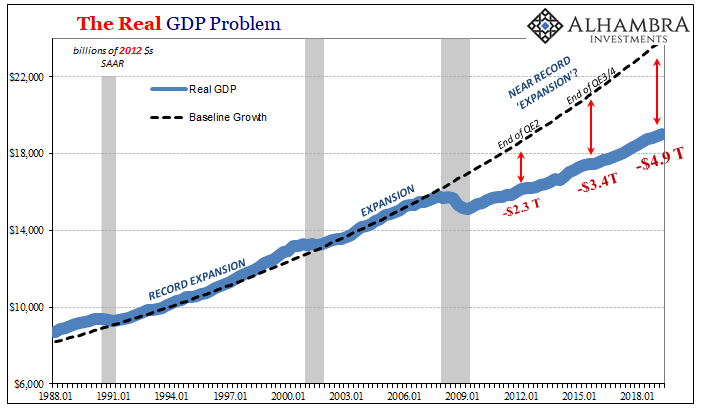

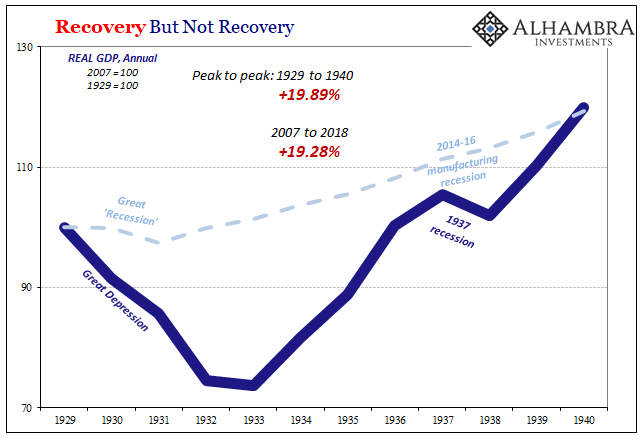

Had the Great “Recession” been an actual recession Real GDP in Q2 2019 would have been somewhere close to $23.9 trillion. Instead, the preliminary estimate is a “record high” just above $19.0 trillion for the first time. There’s an incalculable level of anger and dissatisfaction inside that incomprehensible almost $5 trillion gap.

While that’s a bigger picture problem, the more immediate concern is one of vulnerability. As the FOMC has been quick to point out, the fundamentals of the economy are strong and the US economy is only experiencing temporary “cross currents.” In other words, it is strong enough to withstand them, a little boost from a rate cut or two just to make sure.

Seeing the economy this other way, the more appropriate way, its vulnerabilities rather than strengths stand out. Starting with capex and getting into what real estate might say about those fundamentals in terms of consumer spending.

In the parlance of central bankers, the balance of risks is tilted to the downside regardless of the cross currents. The cross currents are this tilting; they already appear under the headlines. A couple more benchmarks and they might show up better in the topline GDP figures, too.

Stay In Touch