It certainly doesn’t feel like a bubble. We’ve heard about home prices in many cities skyrocketing like there has been one, still there does seem to be something different. If it is a bubble, it sure isn’t the same as the last one, the big one fifteen years ago. Much is missing this time around.

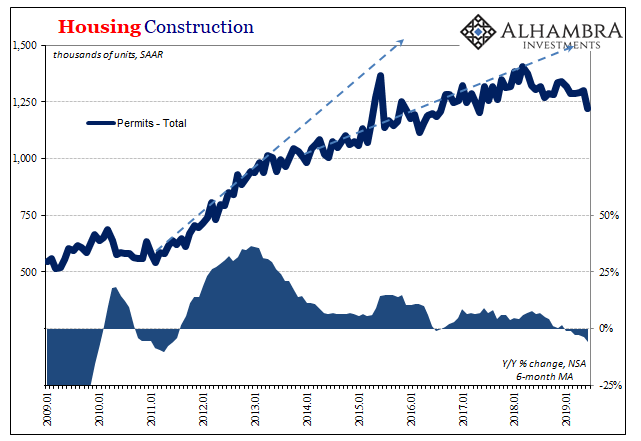

For one thing, prices are disconnected from volume. For all the talk of a boom in the economy the housing sector never joined in. Not really. I wrote last year that a truly booming economy is one that builds houses. This candidate consistently refused.

Real estate, like the economy, has never recovered. In fact, the two go hand in hand; the labor market has its participation problem, the housing market beset by the same defect.

When talking about a strong employment condition, invariably the unemployment rate is invoked even though it is misleading by leaving out millions. The building statistics are quoted, or were, as the highest in over a decade, a similarly misleading comparison for the same issue.

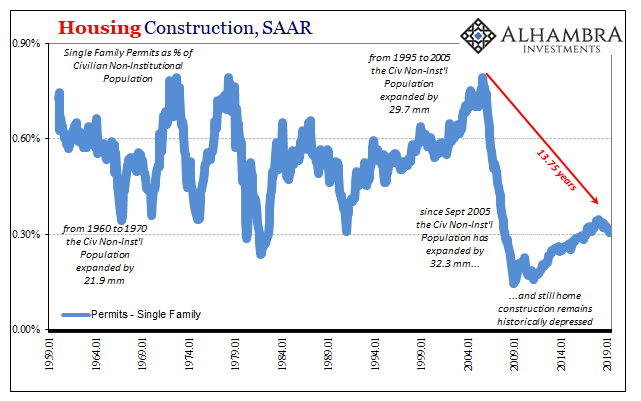

The numbers are astounding when you actually look at them. From 1995 through to the end of 2005, the Civilian Non-institutional population expanded by 29.7 million. Out of those, 18 million are counted as having entered the official labor force. And that wasn’t great.

From September 2005 up to the latest estimates for June 2019, the Civilian Non-institutional population expanded by two and a half million more, 32.3 million. And yet, the official labor force gained only 13 million. That’s an enormous difference.

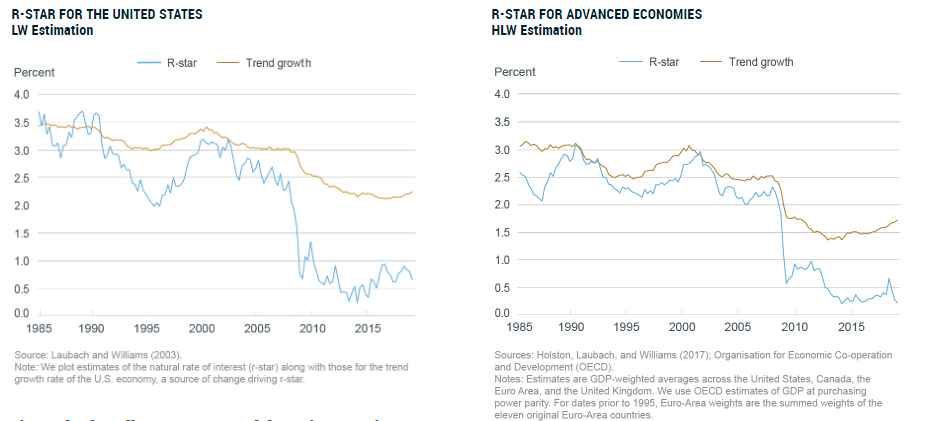

You would think more people more houses, but it is actually fewer workers fewer houses. Federal Reserve officials are running around blaming R* for this disparity even though an actual examination of R* shows what went wrong. The labor market didn’t suddenly die off in a drug binge of retiring Baby Boomers, all of it taking place during 2008.

There actually has been a recovery process in the US and global economy. It has just been restricted to those fortunate enough to have been welcomed into its narrow gravity, disqualifying the rebound from being classified as a general recovery.

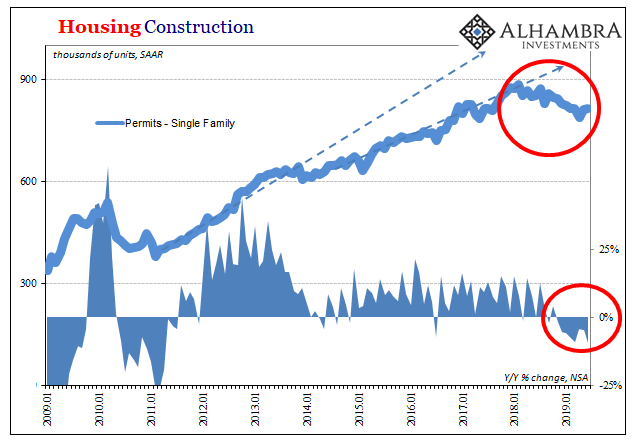

Despite following the largest, most sustained contraction in eighty years, the “expansion” which followed applied to the fewest number of people – as you can plainly observe in homebuilding. These are the people who have bought and built houses. On the other side of things, no job, no home of your own.

What that means for 2019 is actually pretty simple. If there is something going wrong in that reduced space which had been going right, that’s really something to become concerned about. It’s one thing to chalk up weakness to those who haven’t been able to participate, quite another to find out a looming bust is because of those who have.

There is increasingly no doubt as to what is unfolding. The real estate market is going bust; not bust in the 2006-10 sense, but a serious setback nonetheless; by far, the most serious since 2011. The small silver lining, if you want to call it that, is how because housing never really recovered this sector doesn’t carry as much economic weight as it used to.

Unlike other times in the past, homebuilders aren’t going to force the US into recession. Not by themselves.

That is where the good news ends. Again, if there is something going wrong in the few pieces that have been right, what does that tell us?

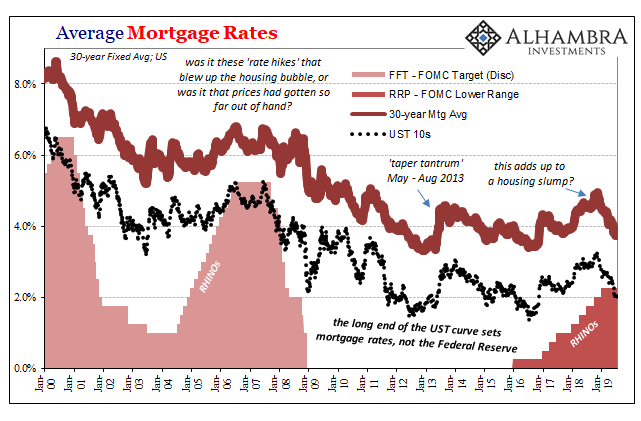

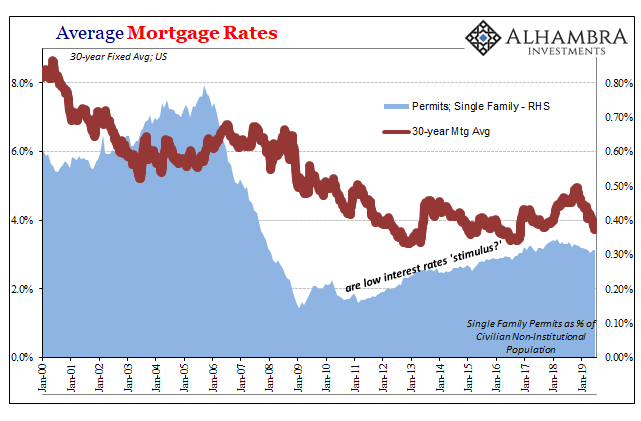

This isn’t a product of interest rates, either. While many have been quick to see “rate hikes” and an over-aggressive monetary policy: first of all, the Fed doesn’t set any mortgage rate, monetary policy doesn’t really influence them; and second, mortgage rates have been falling for more than half a year – and still the housing market won’t bounce.

The average 30-year mortgage rate nationally is not far off record lows (in truth, it never got all that far away from them).

If more homes are built because more have jobs, what does fewer homes being built suggest? Maybe not job cuts in the present tense, almost certainly more who are growing concerned about being vulnerable to being left to join those too many who have remained stuck on the wrong side of the economic divide.

It is a common belief that the Federal Reserve reacts most to the stock market, it might even by captured by the NYSE’s ebbs and flows (more the former). While that’s true it’s only to a limited extent; December 2018’s market swoon being a surefire example.

More than stocks, however, Economists and their DSGE models pay closer attention to housing. As a less volatile indicator of where things stand, policymakers are surely taking note of what’s going on in this sector. The S&P 500 sits at or near an all-time high, but the housing data says it’s not interest rates causing negative pressures in the smaller piece of the economy which was actually working.

That, plus EFF, is why there will be rate cuts in 2019 where rate hikes were supposed to have been. And that’s only the start.

Stay In Touch