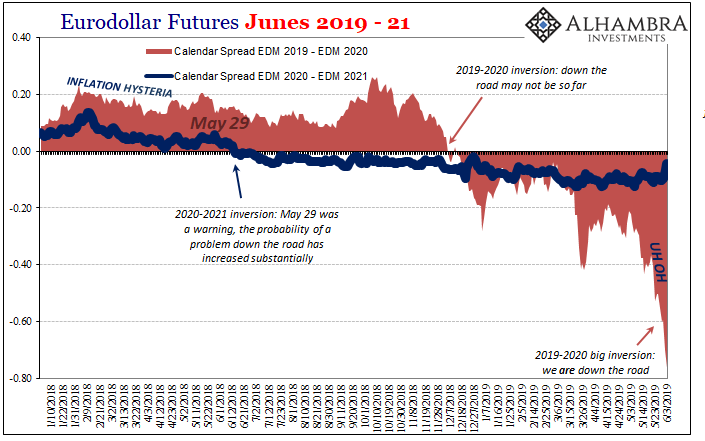

When the eurodollar futures curve first inverted a year ago in the wake of May 29, 2018, it was the market beginning to hedge against serious and rising risks of something that would force the Federal Reserve to turn around. When that might happen, or how many cuts would eventually follow, those were questions the immediate inversion couldn’t answer.

All the curve said at that point was a serious chance Jay Powell was going to be forced into an involuntarily U-turn at some indeterminate moment in the future. I interpreted this market inversion early in July 2018:

Officials believe right now the economy is “very strong” and that demands the same “rate hike” trajectory. The futures curve is betting there is a good chance they are wrong about that and at some unknown point they’ll have to turn around and face their own mistakes yet again.

This was the middle of 2018, remember, when everyone (in the mainstream) was totally convinced. JP Morgan’s CEO Jamie Dimon had just said the 10-year UST was about to fly upwards to 4% in large part because the Fed was being forced by wage pressures and therefore inflation into becoming more aggressive.

Rate hikes.

For the same man to have his mind changed for him in the space of a year, what would have to happen in the world for this contrary scenario to work out? Nothing good.

Over the last year, “nothing good” has become more and more the baseline.

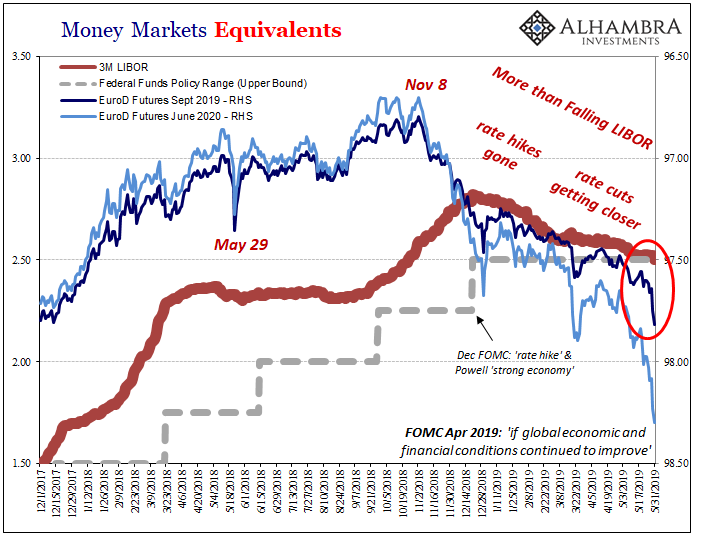

Over the past week, the “bond market” has surged meaning nominal yields have plunged at the same time expectations for future short-term money rates have, too. We are starting to get some answers about when and how many.

Meaning rate cuts. Soon.

FOMC officials view a second half economic rebound as likely. The market is laughing at them. As of right now, there is a very high probability the first rate cut in what the market is projecting as a series will take place by September. This year.

The Fed meeting during that month is a little over three months from today. Again, what would have to happen in the economy between now and then to force Jay Powell kicking and screaming to propose and then vote for what would be a huge admission of his own huge error?

The headline [Markit Manu] PMI fell to its lowest level since September 2009 as output growth eased and new orders fell for the first time since August 2009. Weak demand conditions and ongoing trade tensions led firms to express the joint-lowest degree of confidence regarding future output growth since data on the outlook were first collected in mid-2012.

Markit’s Manufacturing index was never this low even during the worst of the “manufacturing recession” of Euro$ #3. We are already seeing these sorts of stark negative comparisons which the bond market, eurodollar futures curve included, says is only beginning.

We may already be as bad as the bottom of the near recession of 2015-16 – and Euro$ #4 is just getting warmed up.

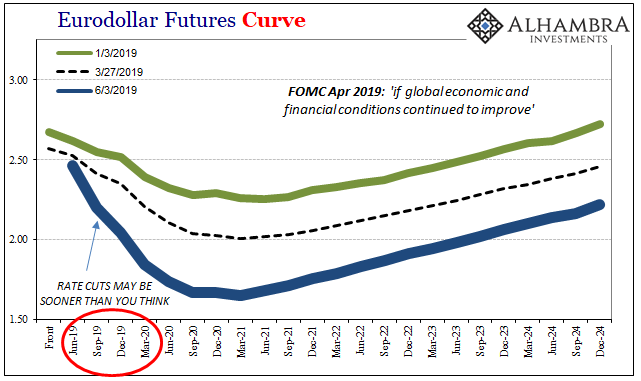

If this is the correct view of the economy, then the downside view of eurodollar futures prevails. As those contract prices skyrocket, they increasingly suggest a probability distribution whose downside case is rapidly becoming renewed ZIRP.

What would have to happen in the economy for Jay Powell to kicking and screaming start cutting rates in September 2019 and then keep going all the way back to the zero lower bound? Where full, completed recovery was supposed to be, only more ZIRP and probably more QE.

Even IHS Markit gets the big picture in the quoted passage above. “Weak demand” before “ongoing trade tensions.”

It’s already pretty shaky and the market is saying this is still just the opening phase.

Stay In Touch