It seems a paradox, at least like it is backwards. The financial media doesn’t help because good editorial standards rely upon the opinions and beliefs of credentialed people who have no idea what they are talking about. If you hold high office in some central bank, we are to assume you are competent about monetary issues.

It’s all given a gloss of geopolitics, too, which isn’t helpful. The dollar destruction people are also onboard with how interest rates have nowhere to go but up. If the dollar is to be globally rebuked, so must UST’s given how there’s so much deficit to be financed. Who’s left to do it without foreign assistance?

What I am talking about is “selling UST’s.” It seems just that straightforward. Why else would foreigners be dumping US assets? They hate America, probably hate Trump, and like the Chinese are keen to create a new world order that isn’t politically SWIFT-centric.

And if these overseas haters aren’t going to buy US assets any longer, how in the world can the government auction its debt for anything beyond huge discounts to where it is priced now? The bond market must plunge.

Anyway, that’s what you’ll hear and read each and every time the TIC data comes out. Foreigners are ditching the dollar with every UST coupon they dispose of.

And yet, the dollar remains as unchallenged as ever (it seems like people were making a big deal out of petroyuan, for example, but that was ages ago, just like bilateral CNY swaps even further back in history) and paradoxically whenever foreign officials are dumping their Treasuries, yields on them go down.

It’s not a paradox at all, of course, it is merely another conundrum for the Alan Greenspan’s of the world. These people who hold high office predicated not on banking and monetary competence but which Ivy League Economics degree they hold; repeating only the things passed to them in academic theory no matter how much contrary practice they come up against.

As a statistician, the true nature and basis of their schooling, they can become the successful general manager of a Major League Baseball team but are utterly lost in economy, markets, and most of all money.

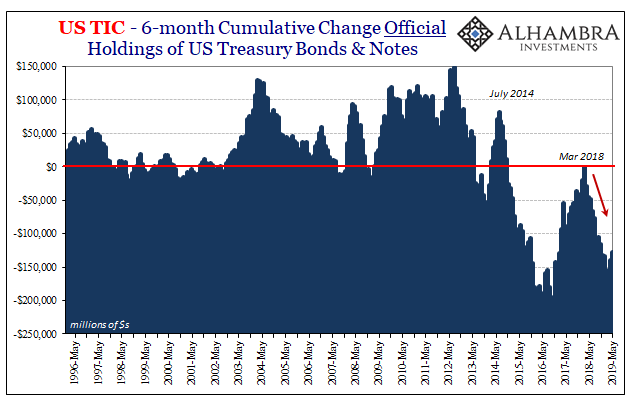

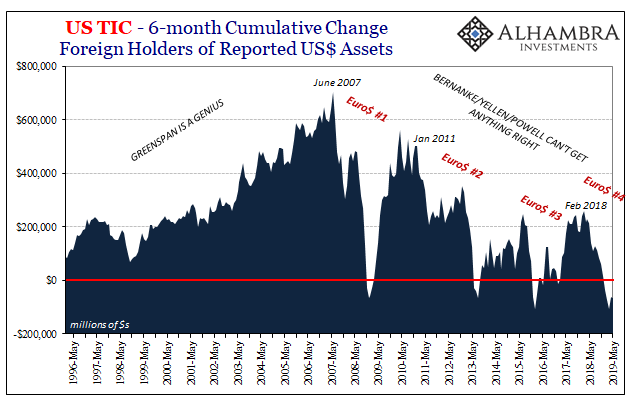

In April last year, the benchmark 10-year UST yield had moved to as a high as 3.03% which was the highest in years. In that same month, foreign governments and central banks began discarding their US federal government debt. Both of those things were characterized as evidence for the utterly ridiculous inflation hysteria.

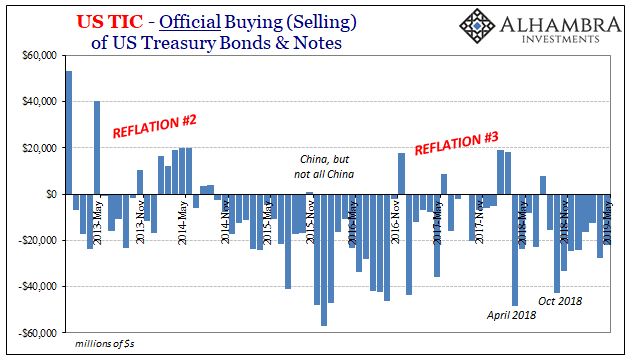

Over the fourteen months since, including April 2018 and concluding with the latest TIC data for May 2019, official selling has totaled an astounding $314.5 billion.

Almost a third of a trillion has been dumped. And yet, it was just two weeks ago that UST 10s yields had dipped below 2%. They are closer again to all-time lows than they are to last year’s highs, let alone rates much higher.

It is, it can only be, a fundamental misunderstanding of how things really work. This isn’t actually a surprise; if you’ve followed Economics and especially its takeover of central banking you know what really happened.

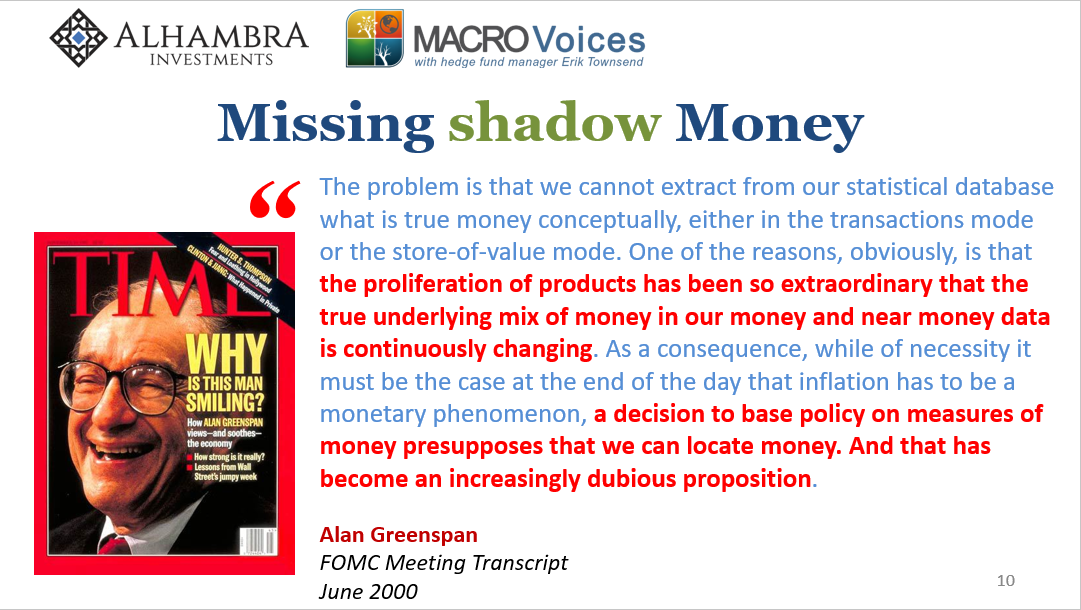

Long ago, central banks found out they could no longer define (forget measure) money. Realizing the difficultly of the task, they just stopped trying. In place of technical capabilities, it was assumed that none were needed; that managing people’s expectations by moving the federal funds target rate around a quarter point here or there would suffice.

The assumption seemed to be a valid one, made so upon “evidence” of the Great “Moderation.”

Our big problem in 2019 is in how nobody grasped the operational implications of 2008. It disproved the assumption. That’s really all the Global Financial Crisis had been; proof that interest rate targeting and expectations management amounted to nothing more than an untested puppet show. About as effective, too. When the world needed some real monetary intervention, Ben Bernanke and crew had no idea what to do.

The only real difference between interest rate targeting and QE is how the latter is a tested puppet show.

The big parts of that monetary evolution were both its strangeness (Greenspan’s “proliferation of products”) and its location. Offshore. Offshore. Offshore. Shadow money, and, as many are now learning, shadow shadow money.

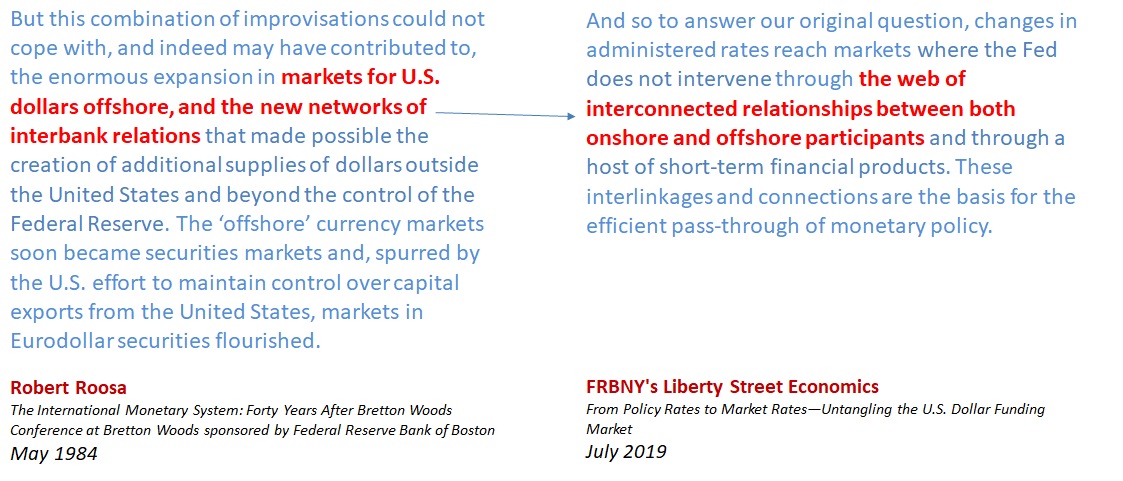

But how does any current central banker like Jay Powell stand up in front of the public and admit to what can only be described as decades of monetary dereliction? It might first start with an otherwise nondescript blog post written out of the Fed’s New York branch, followed up by what might seem to be in orthodox terms a peculiar speech in Paris this week (thanks M. Simmons).

The global nature of the financial crisis and the channels through which it spread sharply highlight the interconnectedness of our economic, financial, and policy environments.

Chairman Powell, giving this speech, then added that this posed challenges for domestic monetary policy (you think?), something which “requires that we understand the anticipated effects of these interconnections and incorporate them into our policy decisionmaking.”

In 2015, Janet Yellen’s Fed had dismissed “overseas turmoil” during Euro$ #3. It seems as if Jay Powell doesn’t have the same luxury, not with a potentially more disruptive Euro$ #4 and rate cuts staring him in the face just a few weeks from now.

It’s not even close to admitting eurodollars as being the real global reserve, and therefore the malfunction in that system which explains both “selling UST’s” (global dollar shortage) as well as the concurrent contradictory behavior of their yields (flight to safety, meaning liquidity hoarding). This isn’t even much of a first step (Powell is blaming differences in monetary policies for contributing to overseas turmoil).

It is the bare minimum: official recognition that the story you’ve been told for decades isn’t so simple and straightforward as you’ve been told. There’s stuff going on out there in the rest of the world that actually does matter. What I wrote last week applies here:

New York central bankers finally come out and admit offshore dollars are important, that they must play some fuzzy role in things, but don’t yet grasp just how important.

Jay Powell isn’t going to admit tomorrow to how the Fed was really a bystander to the Great “Moderation” and that its top Economists were just too eager to take the credit for what was a historical accident.

Don’t get too excited, however. Janet Yellen in 2016, not surprisingly, finally began expressing doubts, too, before then embracing globally synchronized growth in 2017.

As I’ve written before, it’s not these eurodollar squeezes that are the worst. It is the reflations in between. Just when reluctant central bankers finally open their eyes just a little, like that, the urgency disappears and the recovery fantasy begins anew. The worst thing is how it repeats over and over, the only constant these false dawns each and every time.

The end result? The mainstream still believes interest rates have nowhere to go but up, even when they fall, and that selling UST’s is an act of geopolitical defiance rather than the sustained monetary incompetence which, when truly discovered, will actually point the world in the direction of actual rather than imagined recovery. The final false dawn.

Stay In Touch