The ritual of payroll Friday really is a silly one. Everyone and the Fed claims to be data dependent and given the place the BLS is given in the hierarchy of data this one should be scrutinized heavily. But what sort of scrutiny? September 2019’s payroll report doesn’t fit neatly into clean, all-or-nothing interpretations.

To begin with, no one seems to know what to make of it. For stocks, it didn’t seem quite bad enough to join the same category of awful as the two ISM’s this week. For bonds, it was just bad enough to keep it too similar if not all the way there.

I guess what data dependent really means is a definitive signal one way or the other. Either we see something that confirms this economy is right on the verge of recession, or it can’t be.

But that’s not how things work. For what may be the very first time, I find myself in partial agreement with Jay Powell. Earlier today, speaking in Washington, the Fed’s current Chairman said the US economy “faces some risks.” That’s absolutely right. And it is the correct way to analyze the current situation.

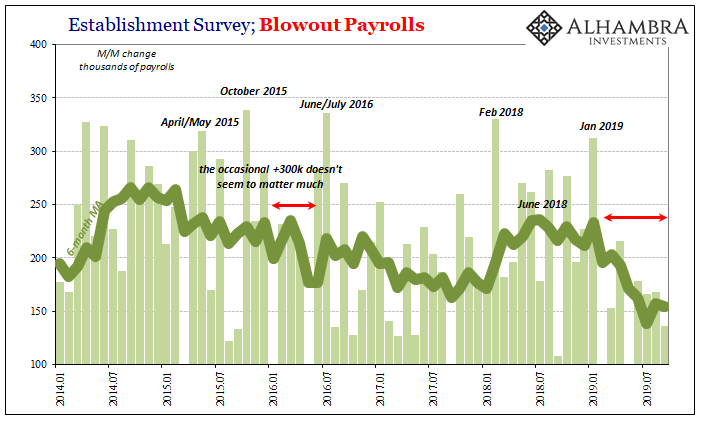

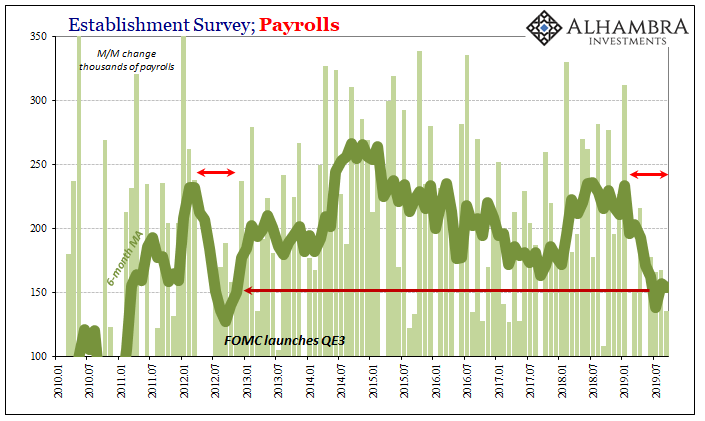

Nothing makes that clearer than the recent run of employment reports. According to the BLS today, the economy added +136k payrolls during September. As always, one monthly number means next to nothing; good, bad, or in between. Far more important, the 6-month average is down slightly to +154k.

What that means is the conspicuous lack of “blowout” reports continues for an eighth month. You have to go all the way back to January 2019 to find a monthly gain of more than +300k. And in that eight-month stretch, there has only been one above +200k while five have been less than +170k (including the latest one).

That’s highly unusual. In fact, you have to go all the way back to early 2012 to find a similar period totally lacking in any upside. It’s the kind of unusual which should immediately get your attention regardless of the word recession – especially when the presumed key to avoiding one rests upon the “strength” of the labor market.

Back in 2012, Ben Bernanke like Jay Powell had said something similar. That the economy faced some risks. Only, Bernanke saw them as decidedly tilted to the downside and that’s why he would launch QE3 that September (and then a fourth QE in December).

In other words, what Bernanke was really saying about risks was that the US economy seemed to be doing well – and then it didn’t. That could’ve meant a 2012 recession (and it’s arguable how close the economy came to one) which is why, QE3 and then QE4, he took no chances. Recession or not, it was not a good place to be.

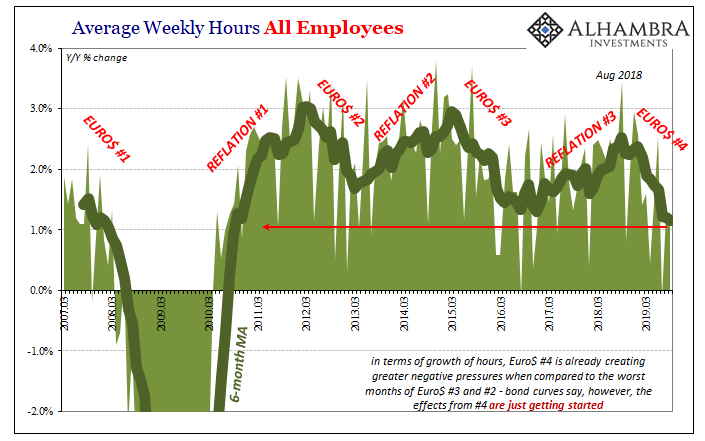

What the labor market data like the two ISM reports suggests is those same risks – perhaps even more elevated than they were seven years ago. While the headline Establishment Survey average is about equal to those depths, underneath there are other indications of a labor market which has been left even weaker than that earlier comparison.

The BLS’s index of aggregate weekly hours has, on average, continued to reach new “cycle” lows. The last time the 6-month average was down this close to 1% growth it was 2010 when the economy was just struggling to get out of the Great “Recession.”

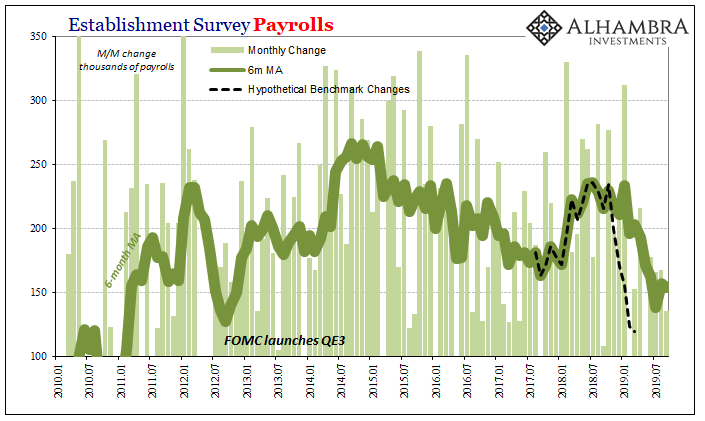

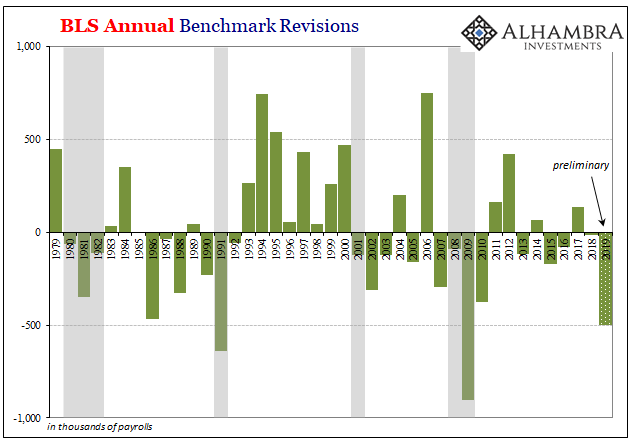

And we also have to keep in mind that there is a non-trivial chance the Establishment Survey looks the same way or potentially much worse. According to the preliminary benchmark assessment released in August, the payroll figures are going to be revised substantially downward early next year. We don’t know how that will turn out, nor do we know how it will affect estimates beyond March 2019.

It’s only reasonable to assume that payroll gains as low as they are now will be recalculated to even lower levels. Something has definitely changed in the economy and labor markets, and maybe something has really changed.

That doesn’t mean there is a recession right now nor does it necessarily mean there is one looming just over the horizon. Powell is right; the US economy “faces some risks.” And they are substantial, more significant in a broad cross section than perhaps at any point since 2009.

And right there is where we have to diverge from the Fed Chair. The rest of his statement said, despite those risks, “overall [the economy] is—as I like to say—in a good place.” If the risks are the highest they’ve been in a decade, as good data dependent analysis has it, that doesn’t seem like a good place at all. It may not add up to recession, not yet, but it’s quite some distance from good.

Powell has instead exhibited the same tendencies as pre-crisis Bernanke; the steadfast denials, the consistent over-optimism. Post-crisis Bernanke wasn’t much better, except in that he seemed to have learned to become less resolute and rigid, to not be so unflinchingly optimistic. That’s why in 2010 a second QE as bond market indications that he had ignored in 2007 and 2008 repeated the same signals.

Same in 2012.

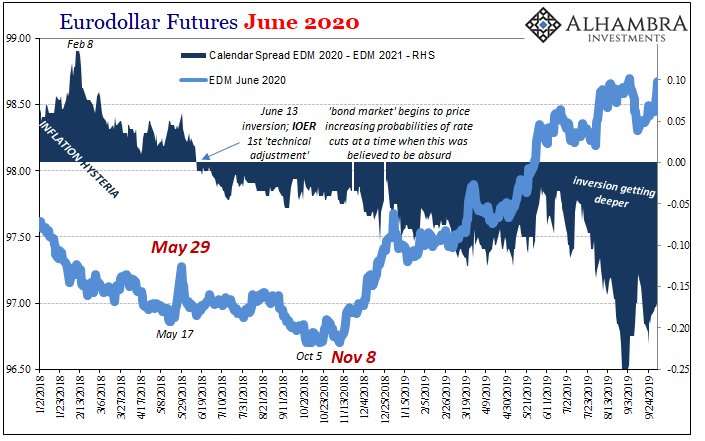

Maybe it’s just the fallacies that new Fed Chairman follow. It’s already been mistake after mistake in the same way during Powell’s first turn. To repeat myself again, the eurodollar curve inverted all the way back in June 2018 at a time when relatively new to the job the Chairman couldn’t have been more “hawkish.”

The trend has simply kept going ever since. The bond market pushes a little more on the economic uncertainty, and then months later Powell must concede on risks. First it was rate hikes becoming a Fed pause. Then it was a Fed pause becoming a one-and-done rate cut. Now it’s two rate cuts, but the economy, as he likes to say, is still in a “good place.”

That’s not the bond market view at all. The labor market data, as well as a lot of other accounts, are displaying an abnormally high level of uncertainty. That’s why the yield and eurodollar futures curves (along with swap spreads and inflation expectations) keep pushing further and further. As I wrote elsewhere today:

While the labor reports were reportedly sky-high last year, the liquidity reports were becoming uniformly negative. In between, the labor reports have become more like the liquidity reports.

Negative, but not obviously awful. The liquidity reports (curves, inflation expectations, swap spreads, etc.), though, are still moving closer to that territory.

The stock market reaction was right in one very narrow sense: the September 2019 payroll number was not a recessionary one (at least we don’t think it was; we won’t really know for sure for another four months). But that doesn’t really mean what everyone seems to think it means.

The downside uncertainty keeps rising because the biggest risk indicated by the labor since 2012 if not 2009 is almost the very opposite of a good place.

Stay In Touch