Scarcely a day goes by without a flood of new articles in the financial media expressing shock and disbelief over Treasury yields. It’s not just that they are wrong, these say, it’s that they have to be wrong. What they are implying just isn’t compatible with the what “everyone” is expected to believe. Consumer sentiment is still high as are stocks (maybe a relationship?) Central bankers are still forecasting a second half rebound.

Officials have even gone so far as to claim financial conditions have improved of late.

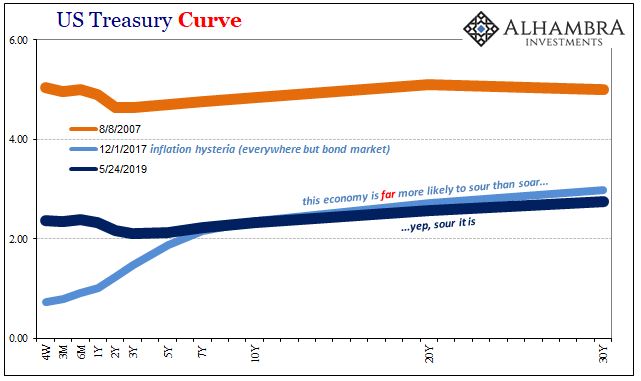

The yield curve, in conjunction with eurodollar futures, swap spreads, inflation expectations, dollar exchange value, etc., is looking at something much more than a soft patch. That might’ve been the first blush of yield collapse in December. Now, as the 10-year UST breaks below 2.30% in yield, almost a full ten bps below federal funds (effective), the bond market further escalating its warnings.

But this might be the BIG ONE We already know 'what'; curve inversions and whatnot are about coming #ratecuts. When? Check the T-bills. They are now all falling together, even the 4-week.

Powell should be sweating, but he's celebrating the recent NYSE ticker. pic.twitter.com/VLbI4TDEcU

— Jeffrey P. Snider (@JeffSnider_AIP) May 24, 2019

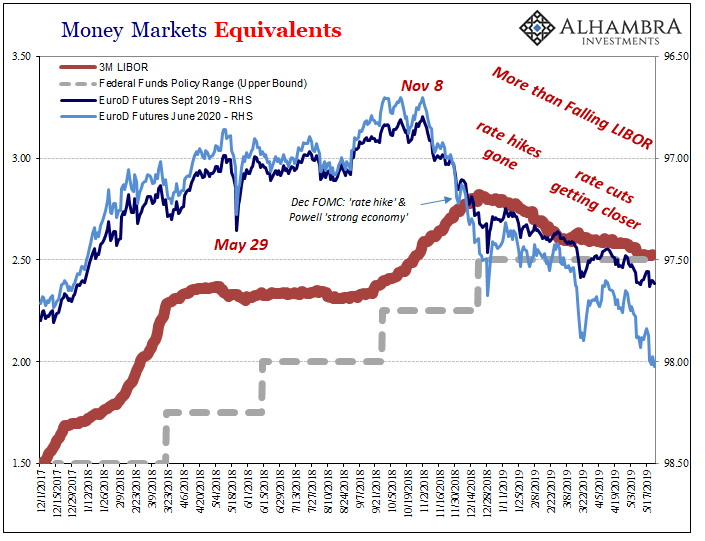

But it’s not just the long end of the yield curve. As noted last week, the big one is actually the short end. T-bill rates are now dropping, too, and not just the 52-week. Even the 4-week bill has seen its equivalent rate lose 8 bps just this month.

It’s like the US economy is on the verge of real trouble. Something like this:

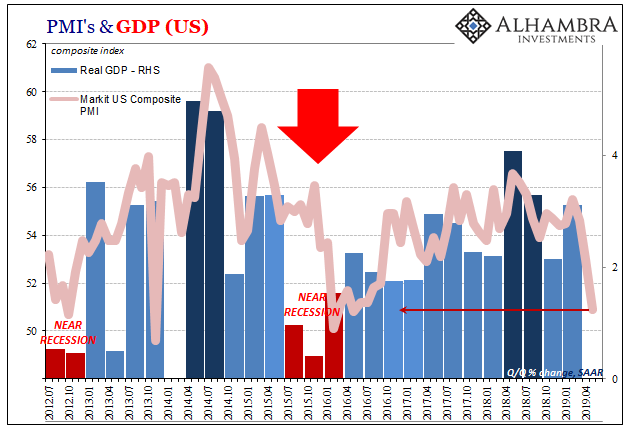

For those clinging still to the unemployment rate view, IHS Markit has some very bad news for you. Its flash composite PMI, an index combining the organization’s measures of both manufacturing and services, fell sharply this month. Released last week at 50.9, it was the lowest reading since the worst months of Euro$ #3.

While manufacturing continues to be the lead drag, the service sector isn’t offsetting anything. In fact, the services component is just barely above 50. Down from 53 in April, at 50.9 in May 2019 not only is that the lowest in this section of the economy in more than three years it’s the largest single-month drop since the near recession of 2015-16.

The manufacturing index was just 50.6. That’s the lowest in 116 months. Enough said.

Consequently, firms put the brakes on hiring. The latest increase in employment was only marginal and the smallest for just over two years. Companies also noted little strain on capacity due to weak demand, and reported the first decline in backlogs of work since June 2017.

As I’ve been writing since January, Euro$ #4 appears to be much nastier than Euro$ #3 at least in the US and Europe. Unlike the third squeeze, this fourth one seems to have cast a much wider net, a far broader target area. Whereas in 2015-16 it was focused so much more on Asia and the EM’s, this time everyone is in the path of the monetary storm; EM + DM.

One big reason why I say this is the bond market. Markit’s Composite PMI is already matching the lows of the last one and the yield curve is telling us this isn’t the end, it’s just getting started. The inventory pile up and distortion in Q1 GDP appears to have finally reached its limit. What’s contained in the PMI report is the stuff of recession.

The eurodollar futures curve nearly a year ago first suggested rate hikes were at an end. Shock and disbelief, official denials followed. They ended. Late last year, the bond market began to suggest rate cuts were coming not in the far-off distant future but at some point this year. More denials. What would make Jay Powell turn all the way around 180 degrees and do such a thing over the next few months?

There never was decoupling. The bond market has had it right ever since the “best” days of this “boom.” The global economy, US included, was far more likely to sour than soar. It would inevitably get interrupted by the malfunctioning global monetary system.

Here we are. Even stocks got a taste of sour late last year. Rather than indicate “transitory”, yields and curves are saying there’s only a steady diet of it from here.

Stay In Touch