You aren’t going to find the worst economic quarter in Singapore’s modern history in either 2008 or 2009. It was actually posted in 2010. During the third quarter of that year, GDP declined by a whopping 11% annual rate. While that’s the biggest contraction still on record, initial government estimates thought it was closer to -20%.

Singapore’s Monetary Authority wasn’t worried, however. Officials often complain about lumpiness in their numbers, and in the city’s case it was actually true for once. For strictly local reasons, the pharmaceutical industry had experienced pure joy the quarter before. Output in this one sector had increased by more 350% sequentially in Q2 from Q1. There could only be a sizable pullback in Q3.

What that had meant was overall GDP gained a ridiculous 27% (Q/Q, seasonally-adjusted annual rate) in the second quarter following a 24% gain in the first. In the race to global recovery, Singapore was way out in front having lapped its competitors.

Q3 2010 was chalked up as an aberration, dismissed as nothing to be concerned about.

And yet, it wasn’t all pharma. In its biannual report published in October 2010, Singapore’s Monetary Authority admitted there was actually more widespread weakness. It just wasn’t eye popping like the quarterly GDP figure.

In the third quarter, the Singapore economy contracted by 18.7% quarter on quarter SAAR, led by a 53.6% fall in manufacturing value-added, which was weighed down by a plunge in pharmaceuticals output. The construction sector declined by 10.4%, while growth in the services sector slowed significantly to 1.4%. Excluding pharmaceuticals, the economy eased by 2.0%, following five straight quarters of sequential gains. [emphasis added]

Negative numbers are rare in this economy. For everyone to rush to ignore one during what was supposedly the absolute middle and strength of global recovery was interesting, to say the least – especially in the context of Ben Bernanke’s haphazard jump into QE2 at the very same time.

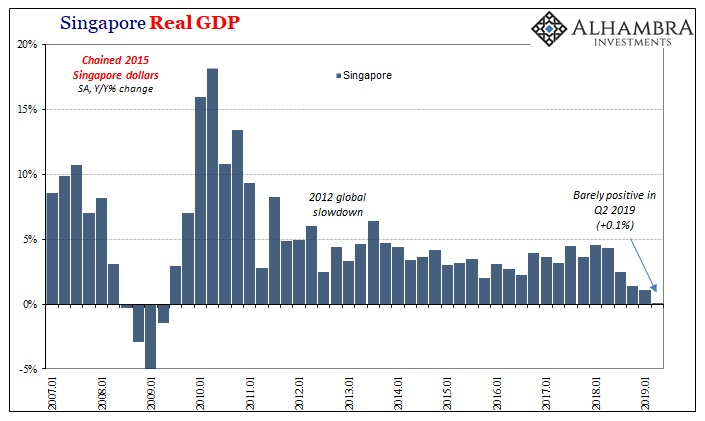

Quarterly growth would turn negative again by the second quarter of 2011 without any pharma factors and then repeat the minus sign one more time in 2012. Measuring output year-over-year (below), what actually happened becomes clearer; Singapore led the recovery in 2009 and the first half of 2010, and then was one of the first to pick up what would eventually become the (permanent) 2012 slowdown.

Q3 2010 wasn’t an aberration; it was a warning shot that “something” wasn’t right about even the best of the immediate post-2009 global “recovery.”

Year-over-year, GDP growth would fall to just +2.8% by Q2 2011 – and it hasn’t been the same since. The economy which had led Asia and the world out from under the Great “Recession” then led it straight into the post-2011 doldrums when even the best of Asia was no longer very good.

Therefore, as Singapore’s stumble in 2010 turned out to be significant, what then do we make of 2018-19? As you can plainly see on the chart above, on a year-over-year basis Singapore GDP just doesn’t do minuses. As rare as they are in quarterly terms, in annual terms they don’t ever happen; GDP rarely strays even close to a negative.

But since the second quarter of 2018 (there’s that month of May again), that’s what has been happening. Annual growth rates over the subsequent year have been whittled down now to practically nothing. Reporting last week, Singapore’s government estimates GDP in Q2 2019 dropped by nearly 4% (annual rate) from Q1. Sequentially, it has been negative in two of the last three quarters, something not seen since 2009.

Year-over-year, the growth was just barely remained on the plus side. At +0.1%, that’s by far the worst showing since the depths of the Great “Recession.”

There are quite a few canaries in quite a few coal mines out there right now, but Singapore’s might be worth distinguishing still further. What’s going on there is unusual, to say the least. And not the sort of good unusual as might’ve been the case for a few quarters at the outset of 2010.

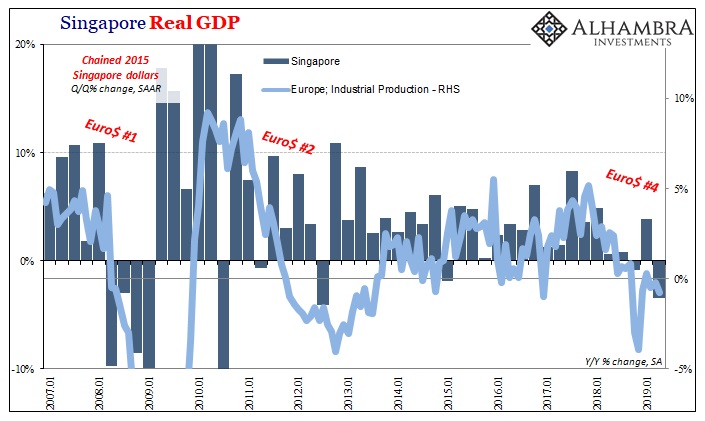

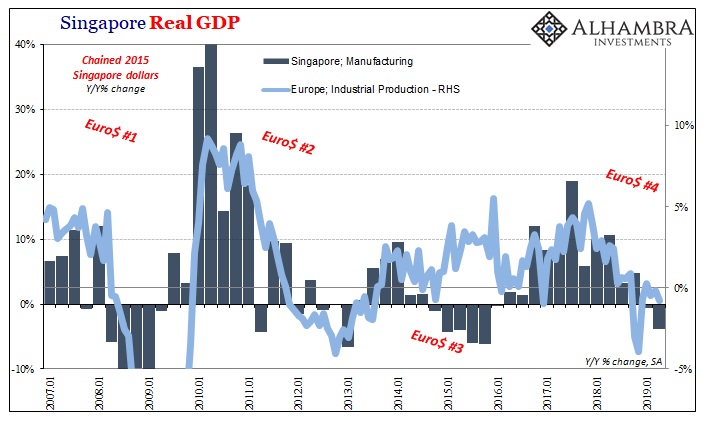

This belongs in the column of evidence for Euro$ #4 being, or becoming, nastier than its prior two predecessors. Perhaps Singapore, a relatively small economy, doesn’t matter or has its own problems which could explain the change. Then again, like South Korea or Germany, as a relatively open one there’s the obvious connections to global trade, global demand for goods, and therefore the global economy.

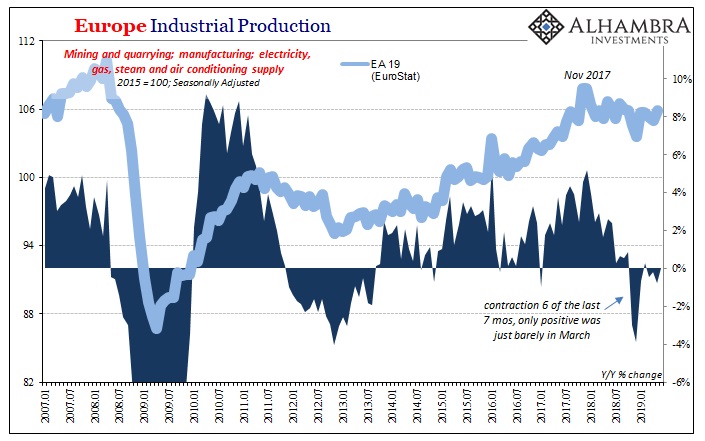

For example, the Europeans (EuroStat) reported industrial production numbers for the whole Continent last week, too. Some are calling them decent if not good – simply because Europe’s industry hasn’t totally fallen off a cliff. It’s May 2019 (in Europe IP), if there is one what is the recession waiting for?

Having finally given up on the boom, mainstream thought and narrative has now swung completely in the other direction. If it’s not a full-blown calamity in any data series, the thinking now goes, this whole thing must be nothing more than “transitory.” Either it collapses tomorrow, or there’s absolutely no reason for it not to go right back to being 2017.

As noted today with regard to China’s data, it’s a weird and spurious if understandable response to disappointment; almost a defense mechanism of sorts. To begin 2018, the global economy could do nothing other than boom. To begin 2019, if it isn’t totally falling apart then it will most definitely go back to booming very shortly (the second half rebound).

But in places like Singapore, it’s closer to falling apart than many would like to admit. There’s much more downside here already which proposes a meaningful, categorical change for the worse.

Quite like Singapore Q3 2010.

Whatever was going on in 2017 and maybe early 2018, I don’t think it was ever a boom, what it was it’s no longer there. For a second half rebound there has to still be a baseline of global expansion. What these estimates indicate is that there isn’t; not anymore. Nastier number four already.

The global economy isn’t falling off a cliff, but that doesn’t mean it isn’t going the wrong way. There isn’t as much difference between plunging and slowly being squeezed and strangled as is being assumed in these mainstream narratives. A slow-motion train wreck is still a train wreck.

Stay In Touch