I don’t think anyone really noticed the timing because nobody really noticed it had happened. What took place last year qualifies as a big deal in the world of central banking and moneyless monetary policy. The lack of clarity about it as well as what sure looks like indecision portrays an intellectual foundation at odds with public perception.

First, the timing. The middle of 2018 should not have needed any shift toward the inflationary. As officials were quick to point out, the boom was creating the very thing policymakers had long been seeking. The tight labor market signaled an end to whatever lingering macro factors had been suppressing economic instincts.

Central banks had done their job. It had taken a long while, but they had done it.

All Jay Powell (taking over from Janet Yellen), Mario Draghi, and Haruhiko Kuroda needed was a little burst of consumer price inflation to confirm the victory. It needn’t have been an eruption, just enough to push the numbers above each respective target (all 2%) and then keep them there.

Outwardly, officials in each jurisdiction played it confidently. This was going to happen, they said, surefire guaranteed. Kuroda even openly talked about ending QQE at the next fiscal year (which would’ve been several months ago). This time, not everyone laughed at the clown.

And yet, each of these central banks shifted their targets. If success was so assured, why the need to change things so substantially? More so, why do it in the middle of 2018 when everything seemed to be going right?

These are really rhetorical questions. We know why; despite all the bravado, the inflationary chest thumping purposefully hid more desperate unease. Mario Draghi’s January 2018 comment perfectly captured the real dynamic:

The strong cyclical momentum, the ongoing reduction of economic slack and increasing capacity utilisation strengthen further our confidence that inflation will converge towards our inflation aim of below, but close to, 2%. At the same time, domestic price pressures remain muted overall and have yet to show convincing signs of a sustained upward trend.

The financial media helped out by focusing entirely on the first part of his statement without ever addressing the doubts on display in the second. As to those doubts, central bankers altered their operations; inflation targets were no longer just targets, they were now “symmetric.”

In Europe, operations have been changed and the idea firmly grasped. Here’s what the ECB said in its most recent statement, the one from last week practically promising rate cuts and some form of renewed QE:

Accordingly, if the medium-term inflation outlook continues to fall short of its aim, the Governing Council is determined to act, in line with its commitment to symmetry in the inflation aim. It therefore stands ready to adjust all of its instruments, as appropriate, to ensure that inflation moves towards its aim in a sustained manner. [emphasis added]

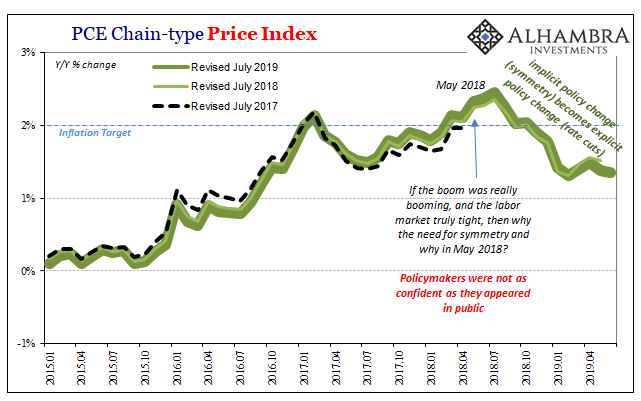

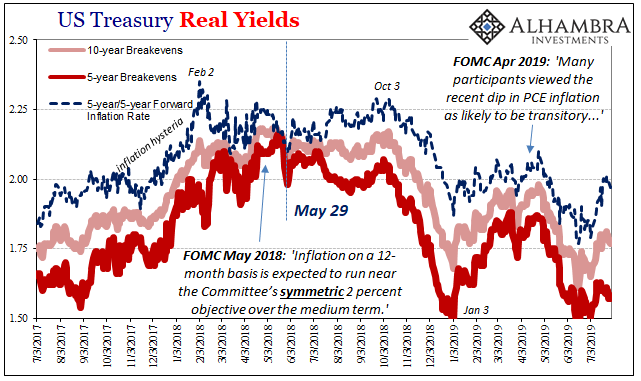

The whole world of central banking abruptly appended the collective mandate last year to include symmetry. The Federal Reserve added the word to its statements in early May 2018 providing the world with an unappreciated and still appropriate contrast. I reviewed what it was on May 29, 2019:

May 29 communicated quite effectively how something crucial was very wrong deep inside the effective monetary system; to which, the people who claim to be running these things, offered up only a single word.

But to the Economist, that single word was a very, very powerful one. By saying “symmetry” this meant the official position had changed to allow inflation to run hot for as long as central bankers deemed necessary to make up for lost time and effort.

Before, a 2% target meant just that; inflation would reach 2% and would be stopped by determined “tightening.” The target was something like a finish line.

Now, inflation might get to 2%, then 2.5%, maybe 3% or 4%, and monetary officials would allow this. It was a big change in implicit bias toward the inflationary. It was indirect, sure, to the central banker and Economist a central bank only ever needs to be indirect.

I explained a few months ago what it was supposed to accomplish:

By purposefully adding that one word, orthodox doctrine says it raised inflation expectations which had the effect of lowering real interest rates the moment “symmetric” made its first appearance. To Economists, this is stimulus. To the bond market, eurodollar curve included, it was beyond absurd.

In April 2018, “everyone” believed central banks would let inflation get to 2% and no more. In May 2018, “everyone” heard the word “symmetry” and understood that maybe inflation would go much farther – and central bankers would let it. Discounting this policy change, “everyone” then had to factor much higher inflation into their forecasts.

That was, to Economists, a reduction in real interest rates – back in May 2018. Economic agents were believed to have acted upon this change in inflation expectations, carrying out the processes whereby it would become a real thing, a self-fulfilling prophecy. Start spending and investing (in the real economy) more today before the inflationary avalanche arrives tomorrow.

The end result, in theory, is that you create the very thing you seek just by being indirect.

Did it work? Of course not. This is nothing more than the opening act for a puppet show.

Since May 2018, the world has gone more and more the wrong way. Nowhere is that more obvious than in Europe. The US economy isn’t nearly as far along on the downslope, but the slope (or balance of risks) is the same anyway.

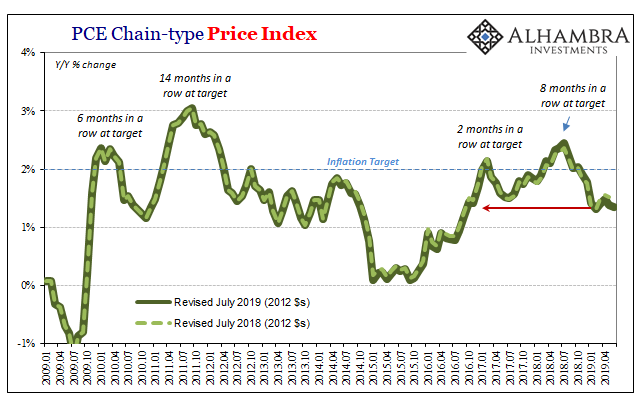

That’s why despite an even lower unemployment rate official inflation numbers keep falling. The PCE Deflator for June 2019, released today, gained just 1.35% year-over-year. Benchmark revisions have reduced consumer price increases in recent months (while increasing inflation slightly in late 2017 and the middle of 2018).

June’s inflation was nearly as low as February, back to more like 2016 than the inflation hysteria of 2017. This despite “symmetry.”

Here’s why this matters in 2019. Jay Powell and his group of policymakers are telling you that the economy is otherwise strong and that the rate cut(s) tomorrow is just insurance to keep it that way.

But he and they also told you the same thing (actually better) a year ago – and even they didn’t really believe it, otherwise they wouldn’t have introduced “symmetry.” It raises substantial questions about policymakers’ ability to analyze and appreciate the nature of the economic condition in the first place, while at the same time it calls into question the effectiveness of anything they might try to do to help.

Rate cuts merely take things a step further than symmetry – an explicit rather than implicit change in policy. Both are supposed to change real interest rates today.

Symmetry was supposed to have been insurance for an economy that was perceived to be awesome. Rate cuts are supposed to be insurance for an economy that is perceived to be questionable. The only things that have changed: the so called insurance becomes more explicit as questions about the economic condition become harder to answer.

It is the same “law” of central banking exposed since August 2007: monetary policy isn’t stimulus, it only tells you how bad the economy is performing. The more central bankers feel they have to do, the worse it already is.

Stay In Touch