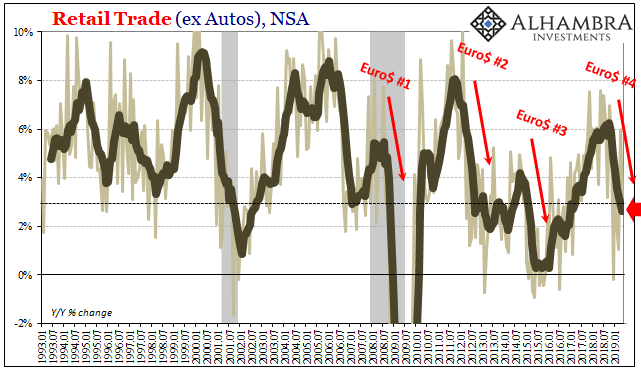

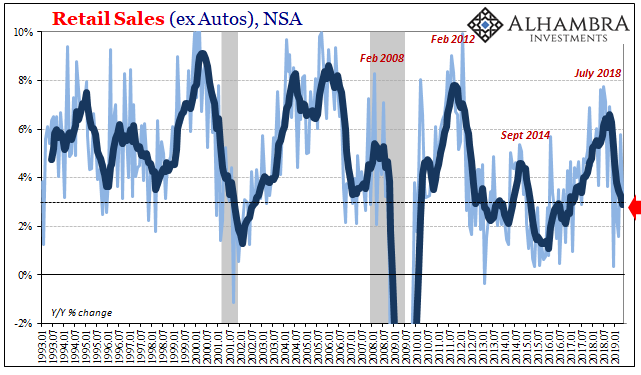

Retail Sales rose just 3.46% year-over-year (unadjusted) in May 2019. The estimate for April was revised substantially higher, now suggesting growth of 5.6%. Altogether, however, consumer spending continues to be unusually weak. How unusual? The 6-month average, a better gauge of growth conditions given the noisy nature of the series, is now below 3% for the first time since late 2016.

The 3% mark is historically more like recession than anything else. In more recent times, with the lack of inflation, it is consistent with at least a serious downturn or near recession.

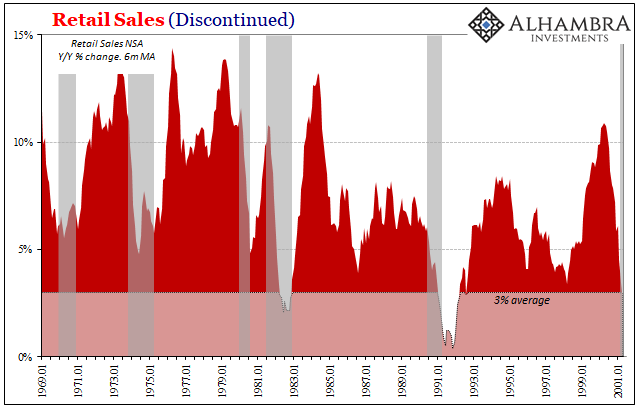

NOTE: The Census Bureau changed methodology in 2001, discontinuing its prior retail sales series which had dated back to 1967 (unadjusted) and 1947 (seasonally adjusted). The estimates, therefore, aren’t strictly comparable. They aren’t so different that they aren’t relatable in rough terms, however.

The Retail Sales estimates don’t account for inflation, which is why during the recessions during the Great Inflation nominal spending continued to rise at what today might seem robust levels. Still, even during the 1981-82 recession, one of the worst until 2008, retail sales on average only just fell below the 3% mark.

In the post-inflation era, the only times when retail sales registered an average that low was the 1990-91 recession and then again in the milder dot-com recession of 2001 (which just shows up in the last months of the data).

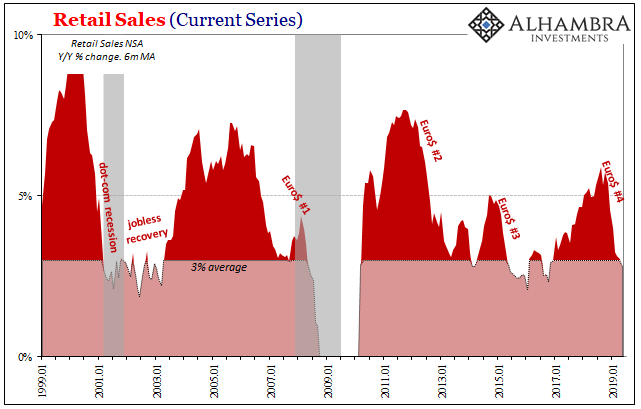

In the current set, getting below 3% on average continues to be a mark of serious concern. For instance, while Chairman Bernanke was saying “subprime was contained” early in 2007, retail sales growth at the same time was suggesting the housing bubble was something bigger than a small subset of the mortgage market.

In 2015, Chairman Yellen’s Fed believed the unemployment rate was signaling a shift to full and complete recovery, the US economy in far more danger of overheating and therefore in need of rate hikes at every possible chance starting at the earliest practical moment (many figured that would have been June 2015).

Retail sales instead suggested broad economic weakness which was forcing consumers into semi-hibernation. There was only one rate hike in 2015 at year’s end and then a full year before the next one.

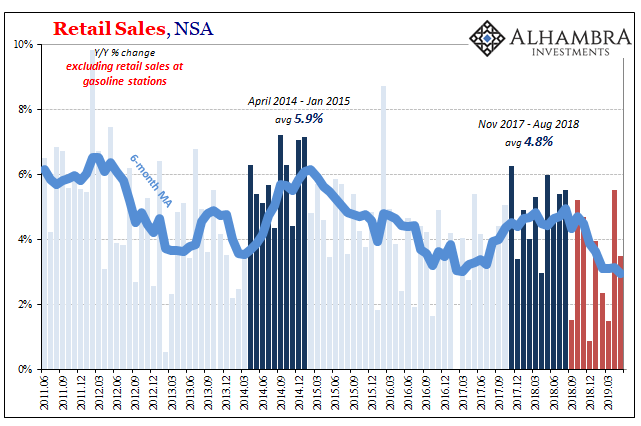

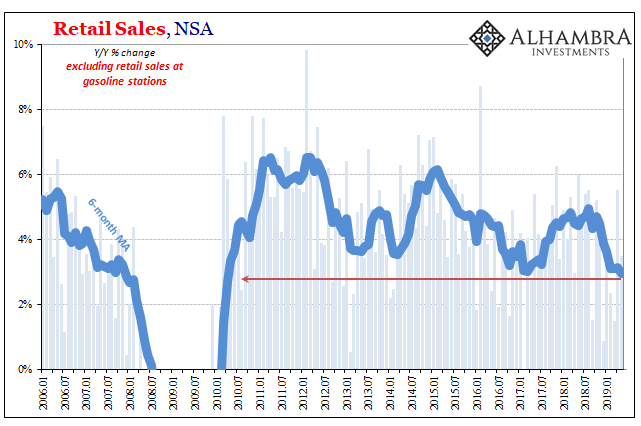

If we strip out the price of oil, which in retail sales means any sales recorded by gasoline stations (of any products, though mostly gasoline), growth was 3.5% year-over-year in May and likewise the 6-month average fell below 3%. Unlike Euro$ #3, the current average is the first time retail sales ex gasoline have been below 3% since 2009. It was close in the aftermath of the 2015-16 downturn (3.02%), but never quite falling fully below.

The other various parts of the spending catalog are all in the same situation; sub-3% averages all around. It might not add up to a full-scale recession at least not just yet, but it is consistent with the more immediate idea of a substantial change in economic fortunes right around the last quarter of last year.

In other words, forecasts for a “soft patch” begin with the idea that the economy is otherwise strong or very strong due mostly to the labor market (unemployment rate). As such, it should turn around relatively quickly. Rate hikes would resume early next year if not later this year (the real hawkish view).

With retail sales data now below the line for the recession danger zone, and sticking at least very close to it in the recent monthly figures, it doesn’t add up to a strong economy nor a strong labor market. The conventional explanation is that the stock market’s drop in November and December caused a minor panic in consumer expectations. They pulled back from spending especially, shocking at Christmas (December 2018).

The stock market, though, rebounded very quickly which if consumers were afraid of those financial signals rather than a very different view of the economy/labor market, we would’ve seen that translate into acceleration somewhere before now.

Together with other labor market data, not, obviously, the 50-year low unemployment rate, it suggests the other more durable set of negative factors. Those that don’t picture a soft patch even if we don’t yet know where the real bottom or downside might be.

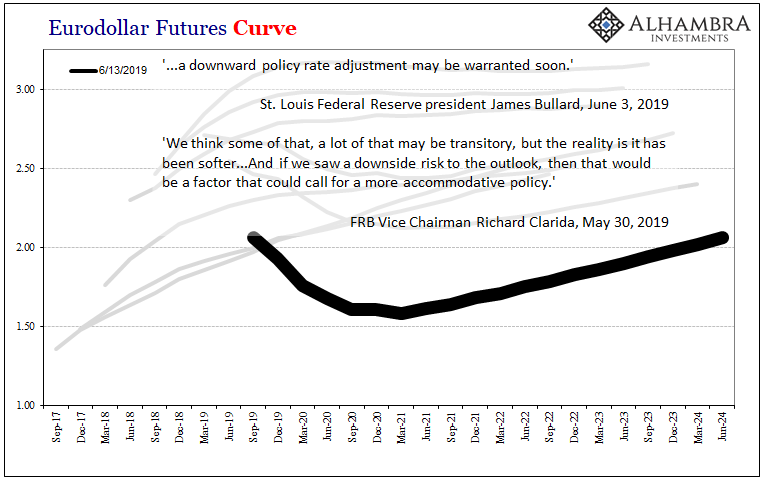

The only factor that is perfectly apparent is that the US economy is experiencing the negative effects of Euro$ #4 and those effects are already to this point serious and concerning. With money and bond curves suggesting that this is just getting started, what is the likely condition in the second half of 2019?

A rebound because of a tight labor market doesn’t seem very likely, especially in light of what it really must be that is at root of this persisting spending retrenchment. It’s not the S&P 500.

Stay In Touch