All Presidents love to talk stocks when the stock market is making record highs. It is the one asset class the public knows about. Even the iconic 1980’s movie Wall Street made it seem just that important. The Masters of the Universe are buying equities, so everything has to be awesome.

The BSD’s on Wall Street were never stock jockeys, though. Never. They were the junk bond kings and derivatives shakers. Fixed income. FICC. These are the things that actually move, and describe, the world.

It’s a bit conspicuous, then, how at a time when stocks are back up at their lofty record perch the President demands a 1% rate cut from the FOMC today (and some more QE while they’re at it). It’s some pretty lofty dissonance.

China is adding great stimulus to its economy while at the same time keeping interest rates low. Our Federal Reserve has incessantly lifted interest rates, even though inflation is very low, and instituted a very big dose of quantitative tightening. We have the potential to go…

— Donald J. Trump (@realDonaldTrump) April 30, 2019

….up like a rocket if we did some lowering of rates, like one point, and some quantitative easing. Yes, we are doing very well at 3.2% GDP, but with our wonderfully low inflation, we could be setting major records &, at the same time, make our National Debt start to look small!

— Donald J. Trump (@realDonaldTrump) April 30, 2019

This is a blatant contradiction. An economy doing well is one where interest rates are relatively high, at the very least something more closely resembling normal. The short end isn’t stuck at around 240 bps, with officials calling for 140 bps. Low rates don’t assure let alone create prosperity, prosperity ends them.

The day the entire world has been waiting for ever since August 2007 is the one when the entire bond market begins the massacre. That’s the day we know there is a real recovery underway. The upward move for interest rates will be as welcomed as it will be immaterial. A booming economy thrives as the 10-year jumps.

That’s what these stock market record people are saying, essentially. Everything must be going gangbusters in the economy otherwise what do share prices actually signal? You can’t call for a rate cut and stick to the NYSE as the main point of economic emphasis. The two things do not go together in that context.

The President is setting up Jay Powell for the fall. Donald Trump ran his campaign saying ignore stock prices and the unemployment rate, then spent the balance of his first term trumpeting the stock market and the unemployment rate. And now the stock market and unemployment rate are, predictably, about to let him down.

He knows it. Thus, the contradiction and search for scapegoat.

May 29 last year wasn’t just a warning sign. Before that date, there were any number of indications and events which were warnings and which were always dismissed as nothing to get worked up about. When stocks fell sharply at the start of last February, recall how the mainstream narrative was how things were in danger of becoming too good; the economy was going to boom in such a massive way the Fed would have to raise rates farther and faster. Growing illiquidity was supposed to have been a sign of recovery?

It makes quite the contrast to the first few months of 2019 and the picture of rate cuts.

Whatever happened specifically on May 29, it more and more has proven to have been the point of no return. The overall balance, the economic center of gravity was tipped back to the wrong side by the tightening eurodollar noose (the rope itself being made out of collateral).

Even after, the intensified warnings were dismissed. Curves began to really fall apart, eurodollar futures inverted a little. Bonds were mispriced, they said. The stock market on the rebound to new record highs was the right view of things.

Then October to December, the very real sense that the entire global economy struck some sort of hidden landmine. The US economy despite talk of “decoupling” was not immune. It was a total worldwide mess, chaos from which even the stock market could not escape. Stunned and confused, officials went dovish.

The new narrative took shape. OK, there had been something going on at the end of 2018, but that’s all over. It was “transitory” factors that even if they mattered will be easily handled by dovishness. Jay Powell has pledged not to do more hikes.

And yet, that is proving just as ineffective. There are more “anomalies” now than there were earlier this year. There are more minus signs across the global economic landscape now than there were when in October, November, and December things really started to look legitimately scary.

The October-December landmine seems to have caused much more than superficial damage.

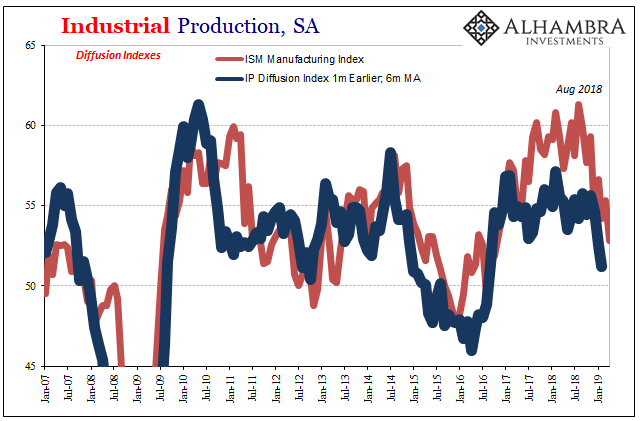

The ISM Manufacturing Index today becomes the latest to indicate growing economic sickness. The manufacturing sector, at least by sentiment and prices, was the core of what was supposed to be globally synchronized growth. In 2017 and 2018, these sorts of PMI’s were the kinds of indications President Trump would tweet about as evidence for his claim the US economy was booming.

Ever since last August, though, even the ISM has plunged. Registering 61.3 in that month, it was still a little better than 59 in November. Dropping more than 5 points in December alone, the latest number for April 2019 comes in at just 52.8. That’s the lowest in 30 months.

Global money, global economy. Timothy Fiore, Chair of the ISM’s Business Survey Committee, says:

Exports orders contracted for the first time since February 2016. The PMI® trade elements are in contraction territory. The PMI® has been inching down since November 2018. The manufacturing sector is expanding, but at recent historic lows.

“Inching down” is a most charitable way to describe it, though one also at odds with an immediate 100 bps FOMC rate cut. The last time the Federal Reserve contemplated anything like that was January 2008. Back then, the FOMC voted for one 75 bps cut and then another 50 bps a week later.

Rate cuts, stock market highs. Those two things don’t belong together at least as both describing the same economy.

Stay In Touch