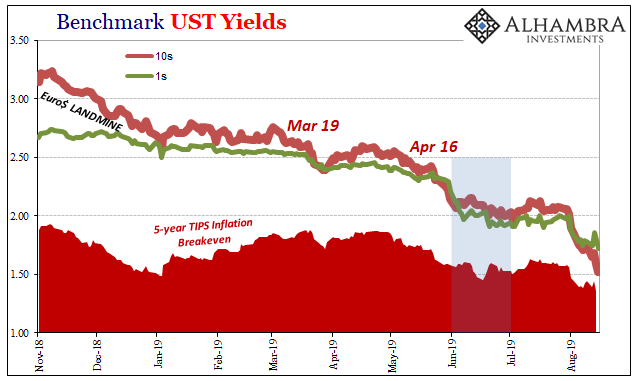

As far as recent times may be concerned, June 2019 wasn’t that bad of a month. Compared to some this year, it was downright uninteresting. Starting with the UST market, there was a plunge in yields (bad sign for global dollar shortage) in the second half of April and throughout May. June saw more steady trading which continued into July that was almost reflationary – until the Fed’s panicky “one and done” kicked off this month’s mess.

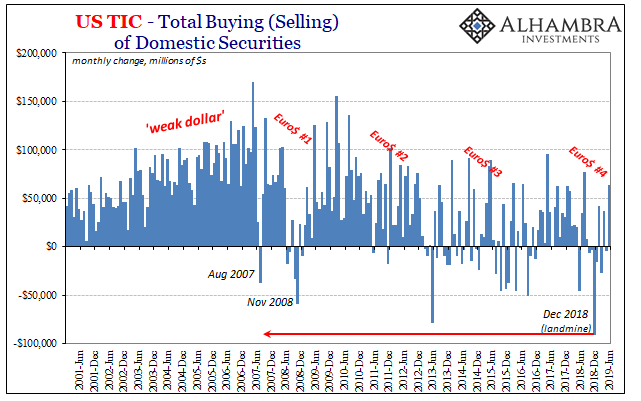

The latest TIC figures now updated through the month of June follow along with the picture presented by yields. The earlier months of this year were, shall we say, rough. Dollar destruction was evident throughout any number of series along with the usual flagged enigmatic wonders (CLO’s and the Caymans). Plenty to corroborate the bond market’s descent into fear.

The landmine and all that.

As bonds took a break in June, so did the “UST selling” – at least somewhat. The private side roared back into US$ assets. At +$63.2 billion net, that was the largest increase in foreign private holdings since August 2018. About a third went into US equities while a little more than a third went toward still more agency paper (there’s a story here for another day).

Private foreign entities even managed to buy about $7 billion in UST’s.

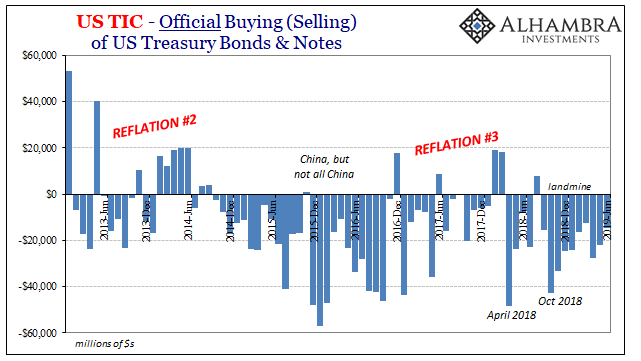

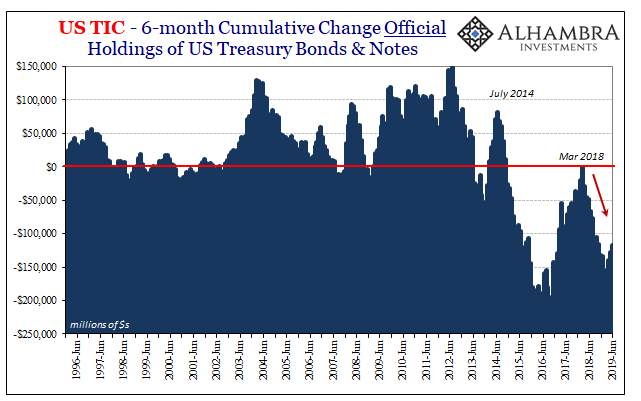

The official sector likewise managed to take a break from heavy selling in June. Total holdings of US$ assets rose by $534 million; not a big number, though compared to what had become usual this was a noteworthy reprieve. Overseas central banks and governments still sold UST’s on net.

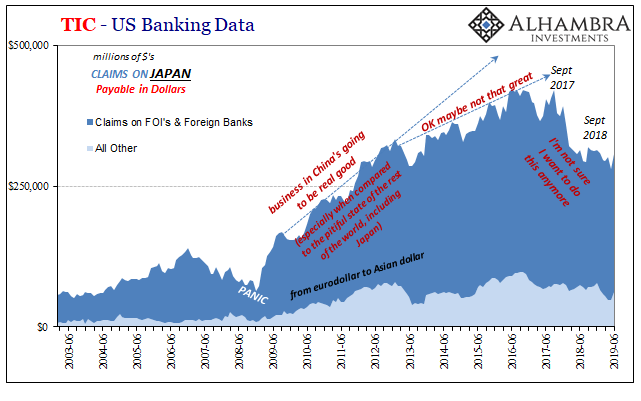

Even Japanese banks, or at least the detectible traces of Japanese banks (which is what TIC shows us), came back in June. Having dropped about $40 billion between September 2018 and the start of June, US bank claims on Japanese banks gained $27 billion during the month.

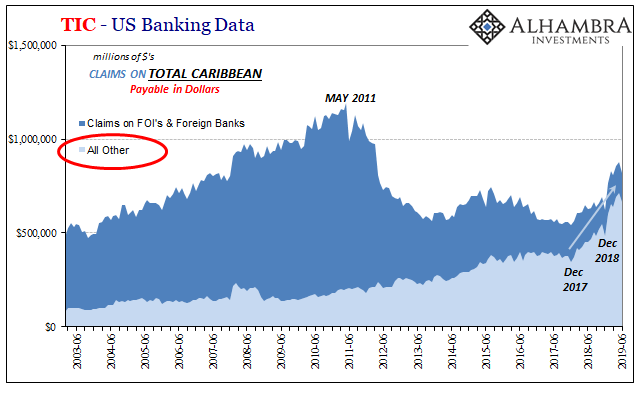

Somewhat interestingly, claims on Cayman Island financial firms (“other”) fell back. As noted last month, there has been a huge change in the direction of bank liabilities in the Caribbean which are related to the sudden appearance of CLO’s now being custodied by US banks. It’s a tangled mess of unknowns which doesn’t immediately suggest any answers.

The size of the anomaly and its central focus, CLO’s, holds our attention for what it could mean (collateral) assuming we can ever figure it out.

At -$57.6 billion, June was a substantial difference. If the decline continued into July and then jumps in August, then we might be able to connect these flows and the mystery they now represent to wider conditions (a Cayman Islands bypass? For whom?)

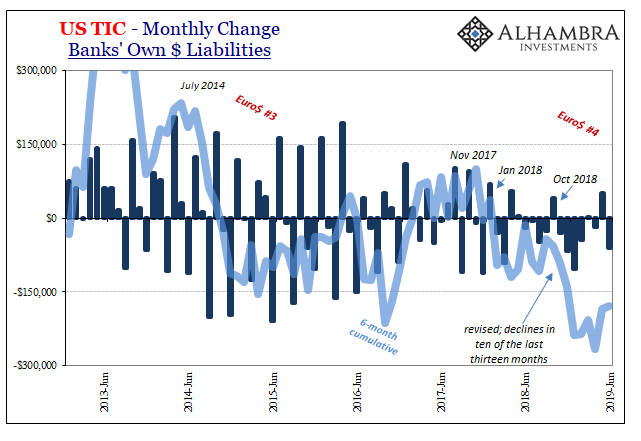

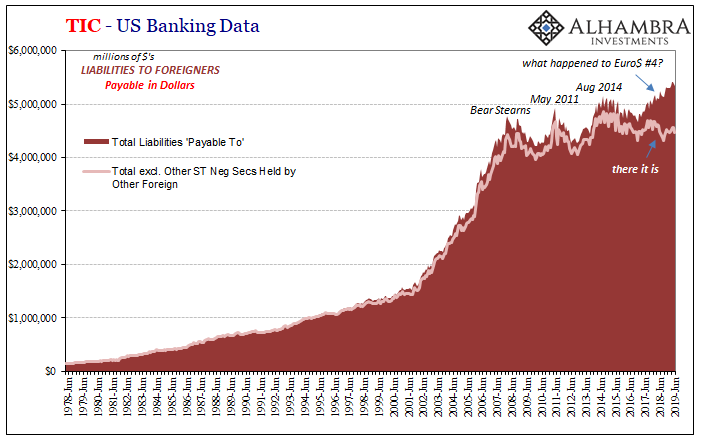

Underneath all of that other stuff, US$ bank liabilities in general took a substantial hit in June. So, while placid on the surface you can definitely see the markets and economy being set up for what’s been unleashed in August.

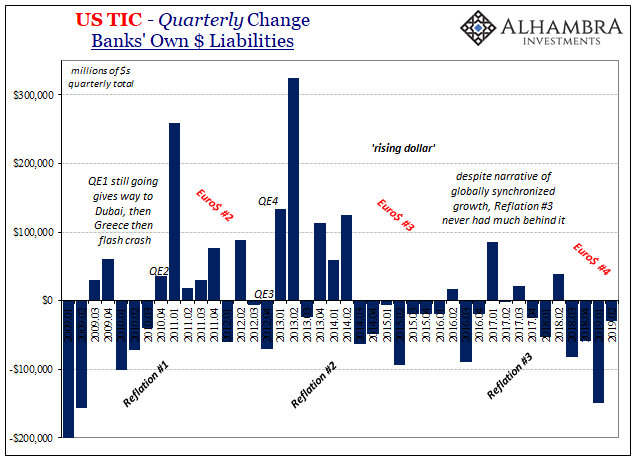

TIC tells us that reported dollar denominated bank liabilities declined rather sharply in June. Down by nearly $62 billion, that was a pretty severe final month for a quarter. For all of Q2, liabilities declined by about $30 billion which was actually the best quarter since Q2 2018. That was due solely to a rebound in liabilities in May, which was promptly given back in June (and then some).

By the (new) trend in bank liabilities you can see how the banking system leads in the background before trouble breaks out at the surface in the bond market (and elsewhere). There were big declines in February and March 2018 – followed by the dollar’s destructive dance through EM’s (and China) last April and May. The landmine in November and December. A rebound in liabilities in May 2019 preceding June’s less chaotic trading.

Now a big drop for liabilities in June which sets everything up for the Fed’s trigger at the end of July (it will be interesting to see what TIC reports next month for the month of July).

You can never get this data to give you a perfect 1 to 1 cause and effect – there’s just too much in the shadows. A lot is admittedly left to subjective interpretation. Still, overall there is a pretty good general fit for what the TIC data describes might have gone on two months ago given what did take place in global markets.

Stay In Touch