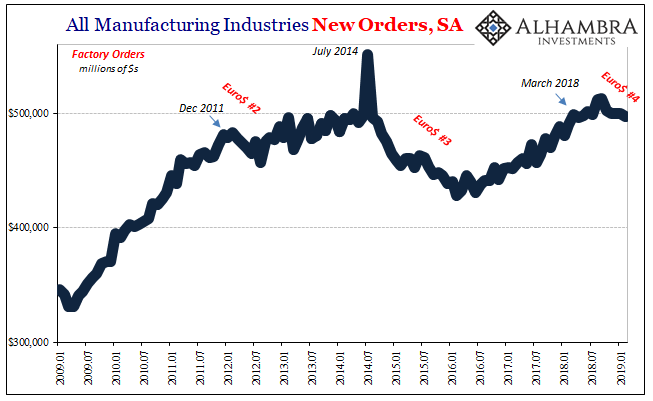

It’s the forward-looking indicators right now that look the worst. This is why we think Euro$ #4 is still closer to its beginning than its end. Even though it may be entering its fifth quarter of existence here in Q2 2019, these things are long processes that take a lot of time to fully play out.

Euro$ #3, for example, you can date its opening to at least the start of 2014 (CNY) if not the middle of 2013. It didn’t fully complete the (mini) cycle until early 2016, the middle of that year at the latest. In total, somewhere between two and a half and three years beginning to end. And throughout every bit of that time, the US economy in particular was declared to be “strong.”

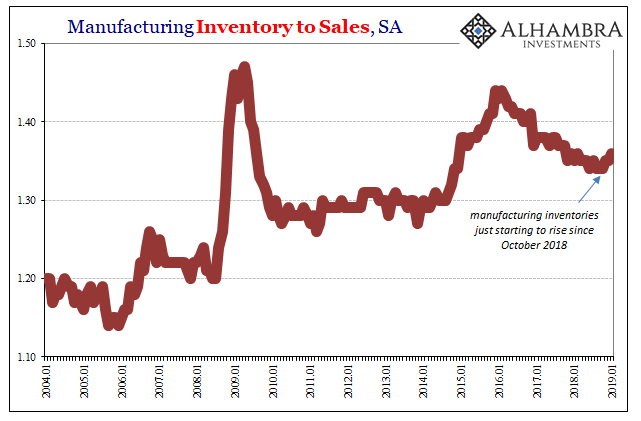

In manufacturing during Euro$ #4, which is where Euro$ #3 really showed up in the domestic economy, producers are still in the adjusting phase. That is, they haven’t yet delved into the deeper modifications to business schedules still believing right now that the economy is strong but softening.

Automobile manufacturers, for instance, posted rather negative sales numbers in Q1. As more complete data is being released, we now know that the topline comps would’ve been much worse had carmakers not “sold” so much product to fleet buyers. It’s the sort of pretend strategy that the big car companies have used forever (Chrysler’s “sales bank” in a smaller, softer form), hoping to smooth out rough spots until the economy actually lives up to its billing.

Stronger-than-expected new-car sales last month belied a dirty little secret: Automakers have been selling more vehicles to rental fleets in recent months to prop up volume.

Deliveries to rental-car companies and other non-retail buyers accounted for more than a third of total sales last month for Ford Motor Co. and Nissan Motor Co., according to data from researcher Cox Automotive.

Auto executives claim they are merely responding to demand from rental and fleet customers, but for some reason that demand always seems to show up just when its most needed. But they can only do this for so long before deeper adjustments will be required. Channel stuffing only works if the soft patch is temporary.

The hit to earnings from selling lower margin product, as fleet sales are discounted heavily compared to retail list prices, eventually catches up. Once it does, production really production costs will become the overriding concern.

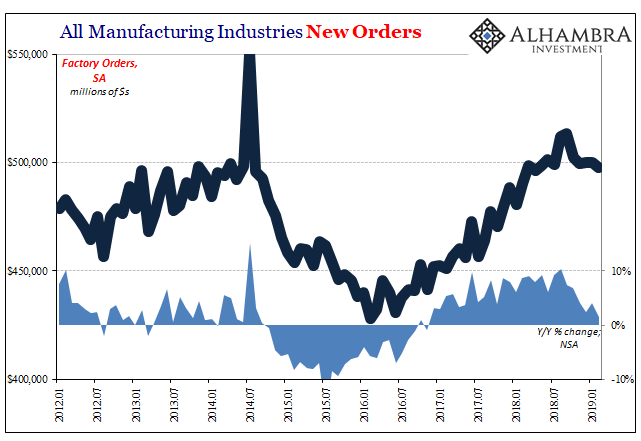

The Census Bureau reports today new orders for the overall manufacturing sector. These Factory Orders are some of the forward-looking indications that right now are on a slight downward tilt. At $497.4 billion in February 2019, that’s down 0.5% from January and a little less than last March.

Reminder: it was during the month of April 2018 that the most visible signs of global monetary trouble erupted.

Unadjusted, US Factory Orders in February were essentially flat year-over-year, barely avoiding the first minus sign since the end of 2016 (the start of Reflation #3). It’s growing more serious rather than fading away. Apart from the upward volatility in September and October 2018, it’s been eleven months now of at most sideways.

These spikes in new factory orders seem to occur at each and every economic inflection, another important consideration. Whether it is a last hurrah as production is ramped up one final time before expected downshifting, or for other reasons that may never be fully clear, the small curtailment (so far) in the US manufacturing sector is consistent with growing trouble spreading throughout the global goods economy – via global trade first and foremost, the piece of the economic equation most sensitive to monetary and financial disruption.

It may be possible that manufacturers are already cutting back by more than what’s presented here in the current estimates (which won’t be revealed until in the future by further benchmark revisions), but we can only go with what’s in front of us. Even this data as it is now presented suggests at the very least going backward.

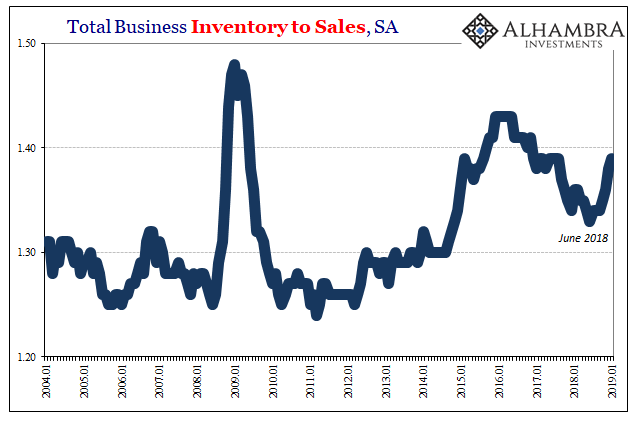

That means either this economic soft spot clears up quickly (the effective Fed “pause” scenario) and everything goes back to growth, or the sector is inching closer to the next level of adjustments beyond the “tricks” currently being employed (not just in the auto sector; there have been reports of channel stuffing among European jewelers, for instance, and rising levels of inventory across most sectors).

This is one reason why bond curves and other things like EFF are important; though the federal funds market doesn’t really matter at least not directly, it is a signal of ongoing difficulties if not outright systemic dysfunction. Most people may not pay attention to something like that, but more and more real businesses operating in the real global economy won’t be able to just dismiss it – something seems wrong. It’s much harder to hang in there and wait when a lot of things really start to pile up on the wrong side of the ledger.

It is the very reason why the Federal Reserve has almost panicked itself into not just this dovish position but also further tinkering with its irrelevant policy rate (the technical adjustments to IOER, the joke, and the leaked rumors of a standing repo facility). The more business remains weak coupled to inverted curves and monetary anomalies, the greater the probability real economy businesses throw in the towel and head for the bunker.

What we see in the auto sector is basically a hedge, partway to the bunker but not yet ready to completely give up on that “strong” economy officials were adamant about last year. Forward-looking, though, how much time is left on it? With inventory up across-the-board, the question is not just one for the auto segment.

Stay In Touch