Because the goal of investing is to accumulate real wealth—an enhanced ability to pay for goods and services—the ultimate focus of the long-term investor must be on real, not nominal, returns.

– John Bogle, Common Sense on Mutual Funds

There is a robust debate these days about whether today’s high stock market valuations are justified. On one side are more conservative investors – like me – who point to the Shiller P/E, the Buffett indicator, the all-time low dividend yield of the S&P 500, and the concentration of that index in a few companies with very high future earnings expectations, as evidence that risk is higher than normal. More aggressive investors point to the tremendous potential of AI and say these valuation techniques are just discounting a future so bright we will all have to wear shades as we collect our unemployment checks. Okay, maybe that isn’t exactly what they say but high valuations do mean high expectations. Unfortunately, expectations aren’t always met or this would be a great argument.

Another common refrain is that valuation is a poor timing tool and my response is, yes, I know that, which is why I said exactly that in this article I wrote a few weeks ago. Valuation is a poor timing tool because it wasn’t meant to be a timing tool; it’s a risk evaluation tool. When valuations are high, so is risk and vice versa. Valuations are not high because things are good today; they come from high expectations about the future. If those expectations aren’t met, it’s a long way down. Low valuations, on the other hand, imply low expectations. If those expectations aren’t met, because the future is worse than expected, the market doesn’t have as far to fall. Falling off your roof hurts; falling off a skyscraper kills you. All I’m saying is that with expectations as high as they are, we might want to move to a lower floor.

Most of the comments on that article also implied that I’m just engaging in market timing and that never works, which is true and something I don’t advocate, at least not in the way most people think about such things. One of the most common mistakes I’ve seen investors make over my nearly 4 decades of doing this, is to make investing an all or nothing game. High valuations don’t mean “sell everything!”. High valuations for any asset class means only that you probably shouldn’t own as much as you normally would. The reason so many investors make this mistake is because they don’t know how much they would normally own. They don’t know because they have no plan, no long-term strategy other than try to own the stuff going up and not the stuff going down. That’s a recipe for failure. I could use a cliche here about failing to plan or an analogy to an ongoing Middle East conflict, but I’ll refrain.

Another common pushback on my “stocks are expensive” article is that the valuation techniques I chose are flawed. Dividend yield doesn’t mean the same as it once did because of stock buybacks. The Buffett indicator measures global revenue versus just the domestic economy or asset light companies have higher profit margins. Some of these complaints are legitimate but there are also some flaws. Buybacks are indeed a bigger part of how companies return capital to shareholders – but buybacks are also easier and more likely to be cut than dividends.

The argument I find least compelling is this one: the Shiller P/E would be lower if not for COVID. It is the least compelling because, well, it isn’t true. The Shiller P/E uses an average of 10 years of real earnings as its denominator and what the critics are saying is that earnings fell a lot during COVID so that means the denominator is artificially low. But the beauty of the Shiller P/E is that it doesn’t just rely on one year of earnings. In this case, the critics are right that earnings were depressed in 2020; how could they not be when we shut down the economy for several months? But what the critics miss is that just as earnings were artificially depressed in 2020, they were also artificially inflated in 2021. If earnings growth had just continued on its previous trend – no COVID, no earnings depression, no earnings rebound – the denominator for Shiller would be about the same as it is today. What might be different is the numerator; would the market be as high as it is today absent COVID? Arguably, no.

I do understand, though, why investors don’t like articles about high stock market valuations. Most of the time, articles like that just say you should “reduce your stock exposure” (or invest in the author’s fund or subscribe to his newsletter) without telling you anything useful about what you should do with your new cash. Part of the reason for that, at least in my case, is that as a fiduciary, I can’t give specific advice to an investor without knowing their circumstances. I write these articles every week for clients and potential clients (I’m looking at you, dear reader) and for myself. Writing for me is a way to think out loud and I am grateful others find it useful but I’d be doing it if no one was reading.

So today I want to see if I can bridge that divide a little and share what I mean when I said in that earlier article “it might not be a bad time to start reducing your bets”. I wrote a little about what that means in the article:

That doesn’t mean go out and sell all your stocks – blind optimists are a lot like blind squirrels. It just means you need to think sell before buy. Check your asset allocation; if you’re invested in stocks, rebalancing will likely involve selling some. Maybe hold more cash than you normally would. You might consider some inflation protection.

Those were intentionally vague but I want to zero in on that last one. There’s a reason I said you might want to consider some inflation protection although the reason is really not about inflation per se. What it’s really about is how you get inflation protection. What I was referring to are TIPS – Treasury Inflation Protected Securities. TIPS adjust your bond principal by the Consumer Price Index and pay interest. It is the only government guaranteed way to protect your spending power. How good a job the CPI does of measuring inflation is an entirely different conversation we’re going to ignore for today.

If we reduce our stock exposure, we have to put that cash to work somewhere and the alternatives aren’t all created equal. The classic response to a run in stocks like we’ve had is to rebalance back to your strategic allocation but that assumes you have one. For the sake of argument, let’s just assume your strategic allocation is the standard 60%/40%, stock/bond portfolio. If you don’t rebalance, the allocation to stocks will rise above 60% over time because they generate higher returns than bonds. Rebalancing just means sell enough stocks to get back to 60% stocks and reinvest the proceeds in the bond side of your portfolio. When you’re done, you will have sold stocks and the expected return and volatility of your portfolio is back in balance with your risk tolerance. It’s okay to let your asset allocation drift some – momentum in markets is a real thing and you should take advantage of it – but you don’t want the percentages to drift too far from your ideal.

I used that John Bogle quote above about real returns for a reason. The goal of investing is to build real wealth; dollars are merely a means to an end, not the end itself. Wealth creation isn’t just consumption delayed (savings); the goal of investing is to increase the purchasing power of that accumulated wealth. After inflation and taxes, what you want is the ability to buy more stuff. Nominal returns feed your ego; after-tax, real returns feed your family.

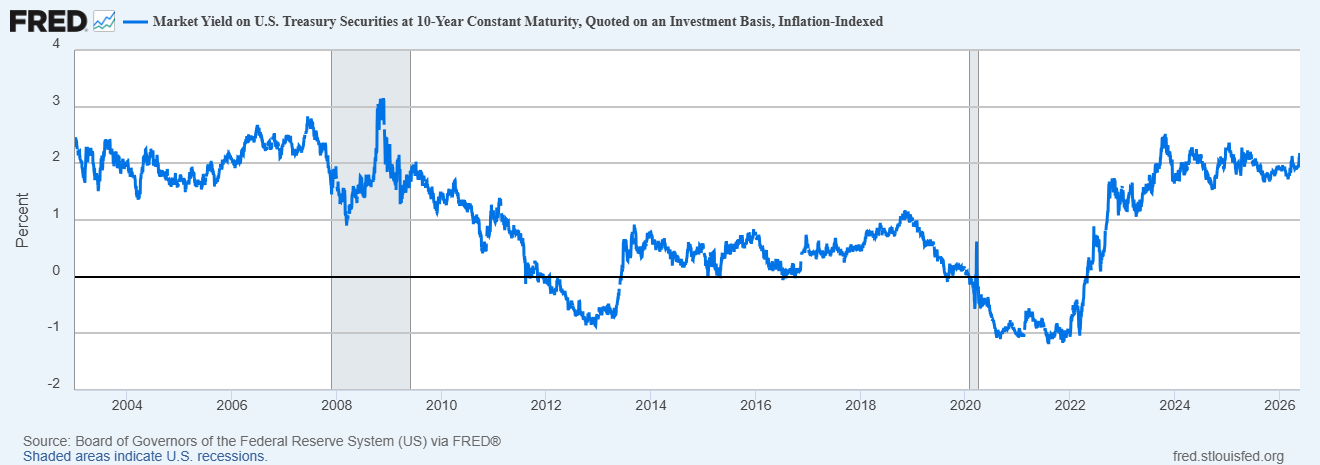

The TIPS market offers a unique opportunity right now. 10-year TIPS yields are over 2%, a real return that is high enough that you can likely improve the expected performance of your 60/40 portfolio by merely replacing nominal Treasuries with TIPS. Real yields over 2% (2.18% now) are good historically. The last time an investor had a chance to buy 10-year TIPS with a yield over 2% was 2006-2008 when yields briefly hit 3%. Subsequently, the 10-year real yield fell below 1% by early 2011, turned negative in 2012/13 and stayed below 1% until the fall of 2018. They soon turned lower again and yields turned negative again at the beginning of COVID. They hit an all-time low of -1.19% in the summer of 2021. Of course, things were quite a bit different when yields were that high before and it would not shock me in the least to see them continue to rise from here. But anything over 2% should start to get your attention.

Replacing your bonds with TIPS would allow only a modest reduction in your equity allocation but it also protects you from future inflation which I’ve heard is a bit of a problem at the moment. There are other tactical changes you can make that provide greater scope for risk reduction without giving up return. REITs have historical real returns similar to stocks (roughly 6.5% for each) and a fairly low correlation as well. This could allow a more meaningful reduction in your regular equity allocation – maybe 5 to 10% – without sacrificing potential return. You’d also be shifting from an expensive asset to a cheap one. REITs have been the worst performing sector of the market over the last 5 and 10 years. They are trading at about 15 times FFO (funds from operations, the equivalent of earnings for a REIT) and there are many REITs trading below NAV. “Work from home” is often cited as a reason to avoid REITs but that concerns a fairly narrow slice of the market. Debt ratios are also historically low.

Of course, with REITs there are no guarantees like there is with the shift to TIPS. And there are caveats with the TIPS idea too; you should buy individual bonds instead of a mutual fund or ETF, for instance. And there are tax consequences with both of these strategies which makes them more suitable for a tax deferred (IRA) or tax free account (Roth IRA). But constructing a portfolio that meets your expected risk/return needs, even without a full allocation to stocks, isn’t that hard.*

High real yields are a signal too. Real interest rates are the intersection of savings and investment. Real rates rise if there is an increase in demand for borrowing (data centers, budget deficits) relative to the supply of loanable funds (falling savings rate, foreign capital repatriation). What does that tell us about the current economic environment? I’ll have to come back to that question another time.

Adjusting your portfolio because an asset is highly – perhaps over – valued doesn’t mean you have to abandon it altogether. It means restructuring your portfolio to achieve your financial goals in another way. It means not following the crowd when the crowd is doing its best imitation of a plague of lemmings. And before you waste your time looking it up, yes, a group of lemmings is called a “plague” and no they don’t actually commit mass suicide. But it is a great market metaphor because what they really do is panic when their population gets too large. Which sounds a lot like what happens when a great bull market expires. Don’t be a lemming.

Joe Calhoun

*If you want to know more about what we do here just click on that Contact button up above and drop us a line.

Stay In Touch