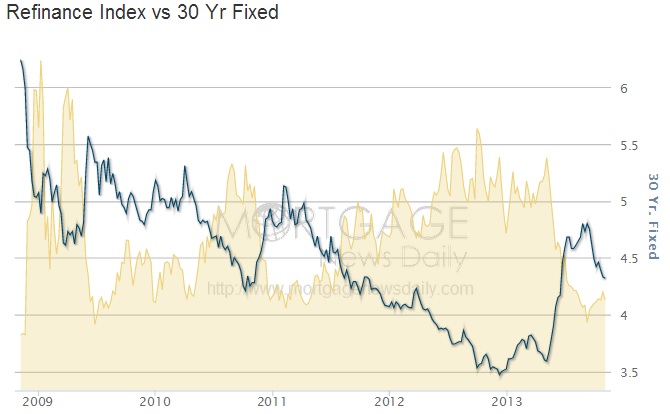

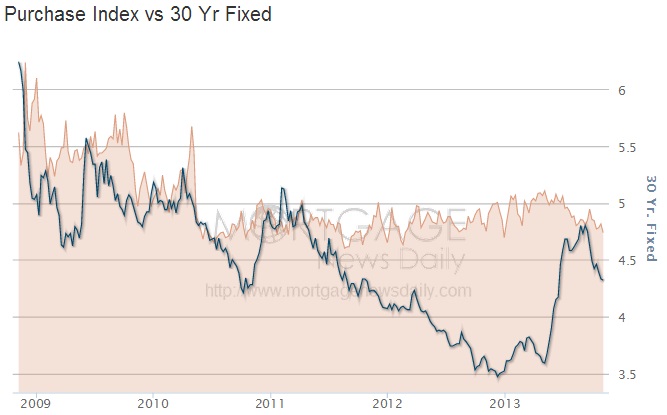

Despite a slight rebound in mortgage refi applications from the absolute low (for now) in the middle of September, the decline in purchase applications actually appears to be steadily eroding mortgage finance. We already know about bank concerns over declining volumes, and the potential liquidity issues from QE, left unanswered to this point is the consumer effect. While this monetary channel has been unable to register enough of an impact to foster a rising economy, its potential reversal, as we might be seeing now, portends nothing good.

Despite an apparent acceleration in Q/Q GDP growth in the 3rd quarter, consumers were conspicuously absent in everything from PCE to imports (more details here).

Refi applications remain 55% below 2012 levels, while purchase applications are now down 5.6% Y/Y. Worse than that, purchase applications are revisiting the generational lows from 2010 and 2011.

We won’t know for sure what kind of impact that will have on the housing market until later this month. The Census Bureau, blaming the “recent lapse in federal funding” has decided that it will hold off publishing permits/starts data for September.

“Data collection for estimates of housing starts and completions occurs in the field with resources that are shared with other critical surveys. Full data collection will occur in November but will require extra time; hence, the scheduled releases are much later than originally scheduled in November. Normal data collection and data releases will resume with the release of the November data in December. Building permit estimates for September have been collected but cannot be published without the release of the remainder of the data in the NRC release.”

So not only will we have to wait for the October data to include September, the October release is being pushed back to the end of the month rather than the middle. Until that point, we are going to have to rely on other sources for our estimations of mortgage-related damage.

The National Association of Realtors reported at the end of October that its index for pending home sales fell 5.6% in September, after declining 1.4% in August. On a Y/Y basis, the pending sales index was up 1.1%, but like construction data, that was the smallest increase in 2 years. And it likely means that pending sales in the coming months will show declines in both M/M and Y/Y terms.

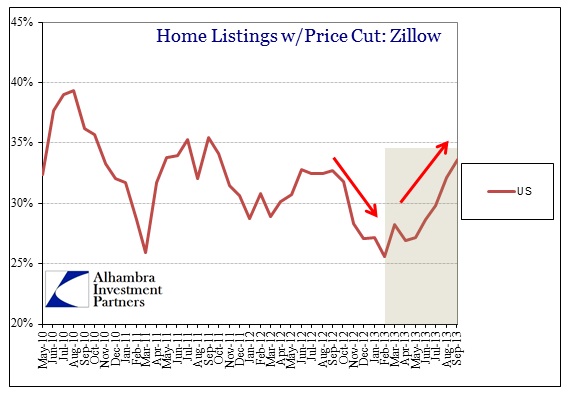

That is not good news for those that expect continued price appreciation to boost consumer emotions, or fear any price reversal, since a decline in purchasing activity may begin to force homes on the market to further slash prices – which is exactly what we see in the incoming (lagged) data from third parties like Zillow.

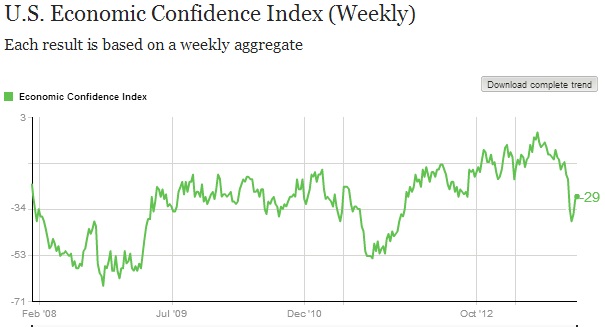

Consumer confidence has been hammered since September, which correlates much more closely with the mortgage/housing events than the government shutdown. The small bounce since the middle of October, according to Gallup’s survey, may show some of the reaction to the shutdown, but the lack of follow-through to this point suggests that housing and mortgage flow may be the larger culprit.

With an economy that has been largely based on inventory growth in the past few quarters, any “headwind” for the consumer, particularly renewed housing “uncertainty”, is dangerous. Too much inventory means too much discounting at some point, spilling over into production (as we saw in Q4 last year). It also means this could get “worse”:

Click here to sign up for our free weekly e-newsletter.

“Wealth preservation and accumulation through thoughtful investing.”

For information on Alhambra Investment Partners’ money management services and global portfolio approach to capital preservation, contact us at: jhudak@4kb.d43.myftpupload.com

Stay In Touch