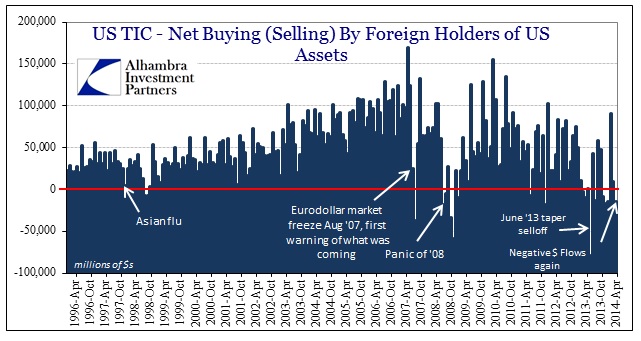

As much as overseas markets, particularly emerging, have come roaring back in a lot of places, there is still palpable unease in dollar allocations. That is as much expected as any kind of erosion or dysfunction will take a meandering course of ebbs and flows. But I am a little surprised at how easy the concerns of last year have been wholly set aside, which necessarily means ignoring funding markets as they persistently show that the dollar disruption of May and June 2013 was not a temporary bump but rather a systemic alteration.

Perhaps I shouldn’t be surprised at the willingness of investors in this day and age to overlook any such downside; that seems to be the current ethos. At any rate, the TIC data for April once again turned negative in terms of $ flows. After the massive rebound in February, it was perhaps a false signal that renewed dollar confidence.

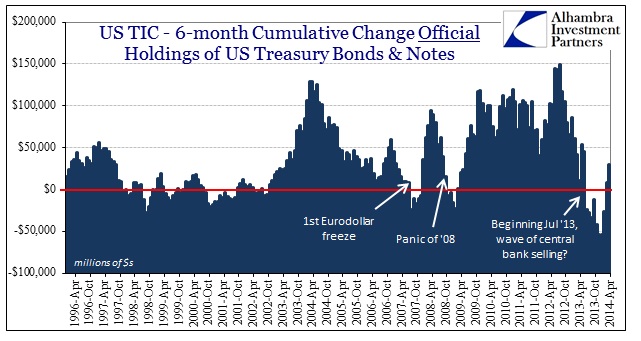

Unlike more recent months, however, central banks are not the primary culprit – at least not directly.

While not a full normalization, central bank flows have at least been positive to US $ assets for three months running (February thru April). That means that any additional dollar selling has been conducted via private channels.

Here the dollar accumulation pattern is perhaps the starkest. What was a durable and uninterrupted gain in US$ flows prior to the first eurodollar freeze has become a ratchet that very much looks like a spreading dollar desert. Maybe that too shouldn’t be surprising given that we know the eurodollar market (or think we know via indirect observations and anecdotes) has been shrinking since that first rumble in August 2007.

Even with that in mind, it is still more than a little unsettling (or should be) to see the dollar erosion that began around March of last year persist with little relative mitigation. Thus the central bank activities fit within this larger context – as central banks became the bypass avenue to procure dollars after the major tightening. And, given the non-linear nature of life including finance, it is not unexpected to see renewal. In other words, central banks bought some time and calm with their efforts but have not “fixed” the problem.

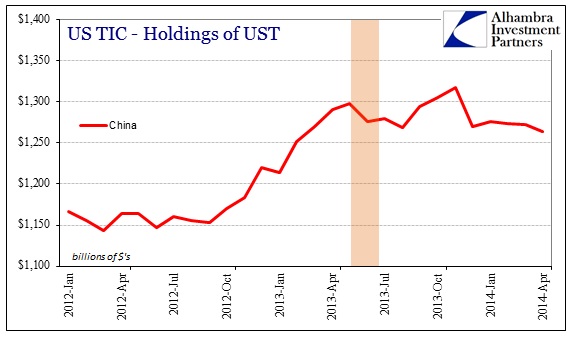

The TIC data makes it difficult to discern exactly where and what is taking place. Again, we are left with anecdotes and partial pieces (on top of staleness) to come up with what may pass for reasonable theory. Obviously, China still fits this dollar description.

Continued depreciation in the yuan against the dollar in April corroborates the idea of ongoing dollar funding difficulties.

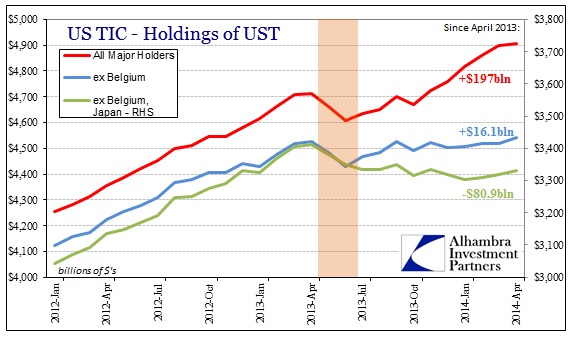

Outside of China, it appears as if emerging markets are squarely within this altered dollar state. Accounting for Euroclear in Belgium (which reversed and shed UST in April) and Japan, the rest of the world continues on a lower trajectory of dollar accumulations.

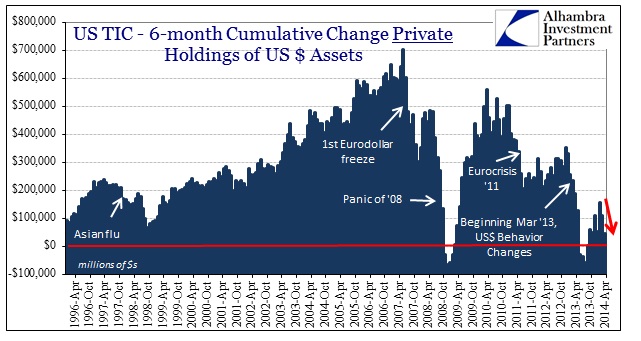

It would be far more helpful if TIC provided a country-by-country breakdown of private flows, but in any case a review of the dollar behavior by asset class is at least as illuminating of this same trend change.

Clearly private holders after the tightening selloff have overly favored UST, which perhaps makes sense in the context of a tighter dollar world. UST’s offer a high degree of liquidity and a relatively low perception of risk (outside of currency risk, obviously). Agency debt and corporate equities which had been bought heavily at the outset of QE3 are now being used as a source of currency liquidity.

To me, the sum total of all of this looks like a very fragile global financial state. Central banks, again, appear to have bought calm and time but are winding down their efforts as if those accomplishments were permanent. The data here shows they are not, as it is plainly evident that the dollar market has been cleaved by policy actions last year. Given the state of global trade and growth, this is a dangerous combination made all the worse by this maddeningly persistent optimism (driven by overcalculations of central bank efficacy) which yields nothing more than a thin basis for ignoring all of it.

Click here to sign up for our free weekly e-newsletter.

“Wealth preservation and accumulation through thoughtful investing.”

For information on Alhambra Investment Partners’ money management services and global portfolio approach to capital preservation, contact us at: jhudak@4kb.d43.myftpupload.com

Stay In Touch