Former Fed Chairman Ben Bernanke welcomed himself to the online economics community by initiating a personal blog at the Brookings Institute where he has landed as a Distinguished Fellow in Residence. This initial posting has created quite a stir, as you might expect, which has to be among the primary reasons for this venture. I suspect and detect, however, that there may be another motive for Bernanke’s newfound public voice. In some sense, it may have made more sense for him to stay low-profile and let his work “speak” for him, but the way economics is going may have made that impossible.

The fact that he starts so defensively gives the endeavor away; he is concerned about a legacy and is obviously seeking to have at least a hand in shaping it – getting himself “on the record” before the judgment of history (and the fuller FOMC transcripts for the QE years) is fully congealed.

The bottom line is that the state of the economy, not the Fed, ultimately determines the real rate of return attainable by savers and investors. The Fed influences market rates but not in an unconstrained way; if it seeks a healthy economy, then it must try to push market rates toward levels consistent with the underlying equilibrium rate.

This sounds very textbook-y, but failure to understand this point has led to some confused critiques of Fed policy.

If you read through enough of the FOMC transcripts of the years that are currently available, especially prior to March 2008, Bernanke’s voice comes across as entirely robotic, cocksure in his theories and especially the abilities of the modern central bank apparatus to gain objectives. A good part of that was written during the housing bubble as coming from Greenspan forward there was a lot of certitude about how the FOMC had “guided” the US and global economies through only a mild recession despite a massive, 1929-style stock bust. It makes an impressive contrast to what he is actually saying now.

The disproportion of that view was given out in the form of the housing bubble, which its own bust has been the subject of all this “confusion.” When an orthodox official seeks to extricate past policy and involvement from any nightmare it always comes down to one theoretical capacity: monetary neutrality. As entirely expected, it is among the first assertions that Mr. Bernanke is making, shown above in the very first sentence in the quoted passage. If interest rates are low now or there is an asset bubble crash “the economy, not the Fed, ultimately determines” the outcomes; monetary neutrality.

To justify how that could possibly be, especially when under his watch the Fed went from implicit “guarantor” of global liquidity to explicit member who’s self-proclaimed job was to take over and manipulate entire markets, Bernanke turns to some 19th century theory on interest rates. That appeal to history is a logical fallacy of sorts, in attempting to establish his doctrine as if it were accepted hard science spanning more than a century.

To understand why this is so, it helps to introduce the concept of the equilibrium real interest rate (sometimes called the Wicksellian interest rate, after the late-nineteenth- and early twentieth-century Swedish economist Knut Wicksell). The equilibrium interest rate is the real interest rate consistent with full employment of labor and capital resources, perhaps after some period of adjustment.

Because of the canon of monetary neutrality, itself an outgrowth of general equilibrium theory and rational expectations, the most the Fed can expect is to influence shorter and intermediate “market” interest rates. The job of the central bank is to identify, as best as possible, what that equilibrium rate might be and then adjust the interest rate target to best manipulate current economic affairs. To slow an economy “overheating”, the Fed “must” bring interest rates above the equilibrium; to introduce “stimulus” is to push the market rate below equilibrium.

To Bernanke’s framing of the problem, there doesn’t seem to be any choice in the matter; at all. The Fed has to do something because it is central in the financial framework, so it may as well pick a target and exert beneficent inspiration.

A similarly confused criticism often heard is that the Fed is somehow distorting financial markets and investment decisions by keeping interest rates “artificially low.” Contrary to what sometimes seems to be alleged, the Fed cannot somehow withdraw and leave interest rates to be determined by “the markets.” The Fed’s actions determine the money supply and thus short-term interest rates; it has no choice but to set the short-term interest rate somewhere. So where should that be? The best strategy for the Fed I can think of is to set rates at a level consistent with the healthy operation of the economy over the medium term, that is, at the (today, low) equilibrium rate. [emphasis on “somewhere” in original; emphasis on latter phrase added]

This is clever (somewhat) reductionism, as Bernanke claims that the Fed will either set the interest rate or the money supply, and if it sets the latter it will by definition set the former. That was the philosophical evolution of monetary policy in the 1980’s, as they found a correlation between targeting some view of monetary aggregates and the effective federal funds rate. They just assumed that it would be simpler to remove the indirect mannerism and target the federal funds rate in the first place to save everyone the trouble.

That is why the phrase I highlighted above stands out, as Bernanke is actually admitting that this is just orthodox theory to which he thinks has been proven sufficiently to close out any argument otherwise. But if that were true, then why so much recent concern over the long run economy and thus his legacy?

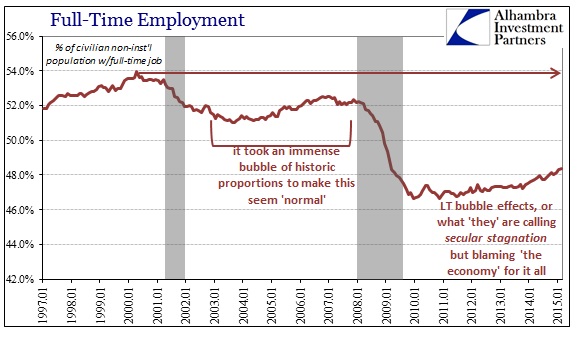

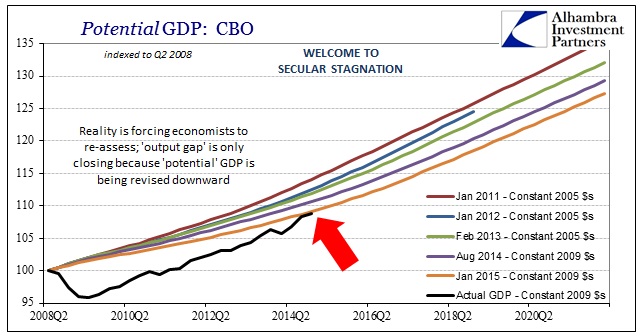

By any reasonable judgment, if that theory on targeting were openly valid then there would be no debate in 2015 whatsoever. The economy would have undertaken a full and true recovery probably by 2013 at the latest, so that at this moment the entire monetary discussion would center on inflation and inflation alone – no wage problems, no worries over gaining re-recessions here and elsewhere, and certainly no disagreement on whether we have undertaken recovery at all. Bernanke’s answer to that muddied array of outcomes is to blame, as secular stagnation, the natural economy. That is the main point through his entire piece, that the Fed is entirely limited and can only do so much to influence longer-term objectives.

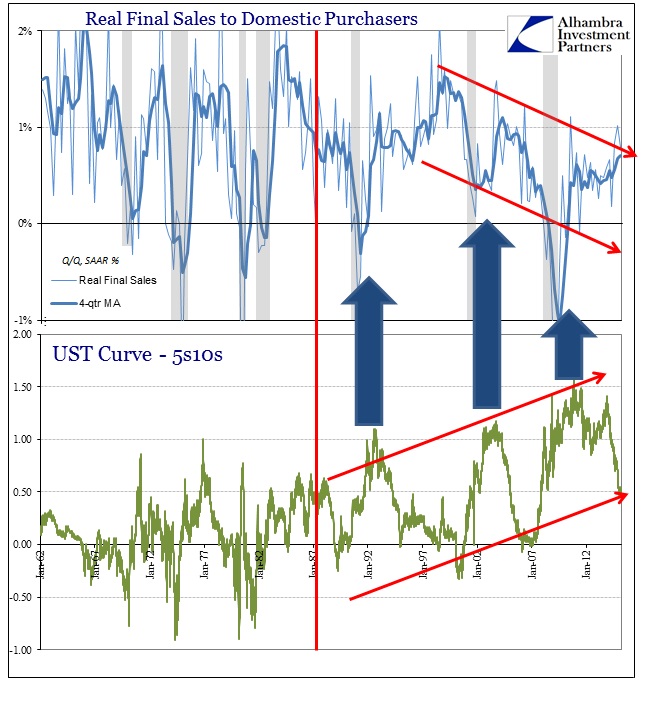

The central axis upon which all this revolves is that equilibrium interest rate. By keeping his favorable view of his own work, Bernanke is insisting that the equilibrium interest rate has fallen and actually has been falling for decades. We know nominal rates have been in steady decline for thirty plus years, but Bernanke is saying that that was a secular trend and only served to make the Fed’s job harder. To stimulate via orthodox methods again means to bring “market” interest rates below the equilibrium rate, and if the equilibrium rate is falling (again, supposedly on its own) further and further then the FOMC will have to reduce its short-term target further and further through successive “cycles.”

The net result is as I showed last week, with Bernanke excusing this behavior exactly as I predicted then.

The fatal flaw in his arrangement is introduced by his own description of what a low equilibrium rate actually might mean (if you believe in such things). He says, “In a slowly growing or recessionary economy, the equilibrium real rate is likely to be low, since investment opportunities are limited and relatively unprofitable.” What we can reasonably infer from that statement is secular stagnation as he sees it, where “investment opportunities” have been becoming, apparently, increasingly limited and “relatively unprofitable.” If that is the trend in the equilibrium interest rate as he suggests, then by rearrangement of his concepts and interpreting them with a more general view the economy has been slowly eroding toward perpetual and unending recession ever since the equilibrium rate surpassed some point of no return.

That is the only way to interpret this theory as consistent with the reality of the current economic malaise. In the end, the only way to preserve Bernanke’s legacy and any positive job performance is to totally and completely admit that the FOMC is economically useless and powerless. That’s not exactly the message that was being sent in the 1990’s and 2000’s when the FOMC formed all these grandiose delusions about its capacities.

Generic as always, there isn’t any reasons postulated as to why the equilibrium interest rate has been falling in the first place. He may think it enough for him to just say so now, but I would think that anyone in his place as Fed Chair would see the falling equilibrium rate as nothing less than a fatal challenge and would commission any and all resources to explaining it in advance of the worst possible outcomes. In other words, if that is the excuse he wishes to offer for being helpless as the US economy staggered toward perpetual non-growth, then that is just a further indictment (perhaps more serious) in that the FOMC did nothing to investigate why the economy was faltering so badly after the mid-1990’s instead of telling everyone how they had it totally under control.

Even if it were not monetary policy to blame, you would at least think that he might want to know how or why so that they could at least make some judgments in advance rather than allow it to simply happen “unexpectedly” as everyone now says. But that view, too, is irreconcilable, namely that if the panic in 2008, the Great Recession and the lack of recovery were all “unexpected” then nobody could have known that the equilibrium interest rate was falling and so low which they now assert in arrears was the case. Otherwise, the equilibrium rate was falling, suggesting mortal economic danger, and the Fed did not know it. They cannot have it both ways; how can they claim reasonable competence now when the most important aspect of monetary policy escaped their understanding, measurement and ultimate decisions upon intemperance?

His post makes plain that he believes professed ignorance will suit his legacy much better. I’m not so sure, especially by established contrast with his attitude and demeanor (policy-wise) prior to the obvious economic break. Rather than admitting they got it all so wrong, they are instead saying that the theories are all sound but that they were just so very bad at applying them.

What is happening is what usually happens in these political kinds of affairs, namely that they are backfilling interpretations to fit the facts and outcomes rather than allowing observation to dictate theory (actual science). If the general interest rate environment is dictated as orthodox theory proclaims, then there is no mystery about secular stagnation. Cause and effect are easily viewed just inside any generalities that still govern the limits of mainstream curiosity about such things.

If low interest rates denote lack of opportunities and no “risk taking” then might that be instead a reflection of both financial incentives and opportunities? Every time the Fed reduces its interest rate target it induces an artificial blending of opportunity costs; this is not difficult to surmise as this “Greenspan put” lowers the perceived risks of “financial investment” as opposed to more extreme views on productive risks. This is most especially true at and around recessions, where productive risks are at their perceived highest but so are profit opportunities.

Instead of focusing on those profit opportunities longer term in productive investment, the central bank introduces this “stimulus” to remove any and all financial “tail risks”, meaning that investors are largely shaded to believe that asset prices are far less risky (under central bank cover) and that returns will be more than sufficient. In other words, who in their right mind would invest productively when it is far easier and more assured to take part in the “wealth effect” of asset inflation?

The actual basis for recovery is shorted at its very inception by this continued appeal to financialism over and above everything else. If the equilibrium interest rate has fallen so low then it has because of the proportional increase in financial opportunities at the direct expense of productive opportunities – so the idea of “stimulating” aggregate demand without any attention to “supply” simply ends up consuming resources without any attention to long-term replenishment. This deficiency is felt in many ways, but most especially in construction and replenishing of collateral. If there is a depressed equilibrium rate, then the lack of sufficient collateral creation in the real economy is its most obvious symptom – and also the greatest evidence that monetary policy has been a cause not a bystander.

The biggest part of enabling the surge in mortgages during the housing bubble was the financial engineering of MBS as top-notch collateral removed several steps from the houses themselves (which would have been artificial but still “real” in the economic sense) or, in a true economic advance, business capacity (factories and machines rather than paper built upon more paper). The FOMC’s common response of interest rate targeting is to build even more paper without acknowledgement of that imbalance, to the point that derivatives and esoteric “flow” components are more currency than currency. So financialism dominates at the direct expense of true economic potential.

The FOMC is trying to cover their collective liabilities over the now-acknowledged economic deficiency, one that is so large it threatens long-term economic stability across all continents. They now assert, conveniently and retroactively, that the incidence of lower and lower interest rate targets was in response to lower and lower equilibrium rates wholly out of their control. Rather than warn on such existential danger, they kept up the main thrust of their demand theories and the idea of their own power and prestige. What really happened was far more simple and easy to establish – that their own policies led to the results; that if there is an equilibrium rate and it has been falling then that is the byproduct of intruding into the marketplace (and I haven’t even covered eurodollars here, which only strengthens that link).

Bernanke says that there were only two choices “I can think of” with regard to central bank activity, targeting money supply or the market interest rate, but in reality what he means is that those are the only choices under a regime where his discretion applies. Any other option simply removes the central bank from consideration of any active inputs, which doesn’t seem so bad now when even central bankers are appealing to their own incompetence to save their reputations or reserve any tendency toward criminal retribution. The bottom line is that the central bank is not consistent with market rates on anything, and so the long run derivation of these serial bubbles traces to that fact alone. The only necessary component to accept such observation and real world establishment is to discard the full parts of general equilibrium theory rather than to retroactively reengineer them to garner the best possible historical judgment. History will not so easily be fooled when it is so obvious.

Stay In Touch