When former Dallas Fed President Richard Fisher stepped down last March after a decade in that role, the New York Times (of course) wrote his professional obituary under the headline Richard Fisher, Often Wrong But Seldom Boring. Fisher had apparently viewed his own philosophical root and career at the Fed as something of an updated Paul Volcker, not surprising given that Volcker was apparently something of a mentor. Inflation was Fisher’s passion; always.

It was that in the middle of 2008 when he cared more about oil prices and rate cuts, worrying that the Fed might have been too “accommodative.” Speaking in Tokyo in April 2009, he said, “I have a reputation for being the most ‘hawkish’ participant in the deliberations of the Federal Open Market Committee, and I have a record that substantiates that reputation, having voted five times against further accommodation during the commodity-driven price boom of 2008.” If he was against “dovish” policy in 2008, he was more so when often the lone dissenting voice against balance sheet expansion.

Two years after his Tokyo speech, Fisher railed against QE2. “Having done our job, I see many risks to the Federal Reserve overstaying its position. There is the risk that we might breach our duty to hold inflation at bay.” The following April, heading toward QE3, Fisher warned:

I’m just reporting what I hear on the street, which is a real concern that with our expanded balance sheet, we are just a little bit in an ember of what could become an inflationary fire.

Then, the following summer after QE3 and then QE4, Fisher was at his most colorful speaking in Toronto, including himself with former Fed Chair Paul Volcker in a summation of something like modern Shakespeare.

We cannot live in fear that gee whiz the market is going to be unhappy that we are not giving them more monetary cocaine…

Only time will reveal the efficacy of current policy and whether the risks that I and more experienced observers like Paul Volcker fret over are as substantial as we surmise, or whether we have made much ado about nothing

That was in response the bond market’s “taper tantrum” with an MBS rout and actually rising interest rates. He wanted the FOMC to ignore any complications on the road to normalizing policy and the economy. Normalization, of course, didn’t last and “inflation” never did appear (in the official calculations) nor the economic utopia the FOMC had planned. Now a year out of office, Fisher is still worried about inflation and “monetary cocaine”, as if the market’s struggles are related at all to what Janet Yellen will or will not do.

Today on CNBC he accused Janet Yellen and the FOMC of, “living in a constant fear of a market reaction. This is not how the way you manage central bank policy.”

Fisher exemplifies many admirable qualities including the fearlessness to challenge the profession (academic) economists at the Fed. At one point he spoke what was likely the truth, exclaiming “My local dry cleaner, I would say that if you took him and put him against the whole Fed staff in terms of forecasting, he’s been far more accurate.” But that still leaves his quixotic inflation crusade on exactly the same level as the Fed staff, if only spun in what seems to be a different direction. They may disagree on how it works, but to all of them this is “money printing” and so they act (and warn) as if it were. Balance sheet expansion = money printing = inflation, even if it never happens (including Europe and Japan, where central bank balance sheet expansion has led to nowhere but continued and increasing financial distortion).

There is a tendency even among the Fed mainstream and its most vocal critics to assign far more power to the agency than is realistic or even evident. The most prominent dissenters to Janet Yellen have not been those opposed to the whole idea of monetary policy in the first place, they have been “inflation hawks” falling for the con of “money printing.”

In his seminal book, A Monetary History, economist Milton Friedman (along with economist Anna Schwartz) writes in a footnote during his chapter on what he considered “The High Tide of The Reserve System” (which was the 1920’s in his estimation, telling you a great deal about our current and continuing deficiencies since it is his disciples now claiming to run the global economy via money printing) a lesson that he nor those that followed his work ever seem to have truly accepted.

It is natural human tendency to take credit for good outcomes and seek to avoid the blame for bad. One amusing dividend from reading through the annual reports of the Federal Reserve Board seriatim is the sharpness of the cyclical pattern in the potency attributed to the System. In years of prosperity, monetary policy is said to be a potent instrument, the skillful handling of which deserves credit for the favorable course of events; in years of adversity, monetary policy is said to have little leeway but is largely the consequence of other forces, and it was only the skillful handling of the exceedingly limited powers available that prevented conditions from being even worse.

That was written in 1963 about policy discussions and economic interpretations of the 1920’s, but it could have just as well been written in 2009 studying not just the disaster that had unfolded (the last sentence is the entire premise of Ben Bernanke’s last book) but the years preceding it that basically guaranteed the outcome. In other words, the Fed, from Greenspan forward, believed that through first threats of “money printing” and then actual balance sheet expansion (which they all take as money printing) they were in charge of the global economy; and that they are still in charge now, only being relegated to the latter part of Friedman’s admonishment, the “years of adversity” with very “little leeway.” Those inside, and now outside, attribute to the central bank powers it likely never had going back as far as Friedman’s work close to its inception. They champion their own power because what else are they going to do? It has always been a bureaucracy, so there is no surprise that has this entire time acted the part.

If we limit this take to just the past two or three (or five) decades, it is the literal truth since the global economic system had risen and now falls on something entirely unrelated to their intentionally narrow self-interest. There is no inflation or recovery since 2009 because money hasn’t been printed it has been destroyed; and continues to be so, which is the true worry of 2016. There is no “monetary cocaine” except insofar as those who believed in it acted on the illusion, only to run into the very real consequences of a monetary system in reverse – systemic reset through liquidation(s).

The reason for this is blindingly simple, too, and traces back to the same human tendencies that gave Friedman his premise. As I wrote back in October, the Fed warned itself about eurodollars starting in the late 1960’s, only to by the late 1970’s dismiss them as an interesting but irrelevant “investment choice” for global banks. Economists and policymakers stuck instead to their 1950’s view on money and believed they were running things, ascribing anything good and positive to especially Alan Greenspan, the “maestro”, when it had almost nothing to do with him, interest rates or their conception of “money printing.”

Before 2008, prop trading and spreads were not just favorable but undoubtedly so as any number of unrelated firms suddenly became FICC centric. GE Capital became a leading provider of mortgage warehousing as well as “investing” while formerly uninteresting insurance companies like AIG transformed into both securities dealers and prime purveyors of dark leverage, especially CDS. It was all, of course, artificially inflated by the nature of that time, the Great “Moderation” because the whole system long ago departed basic and operational sense.

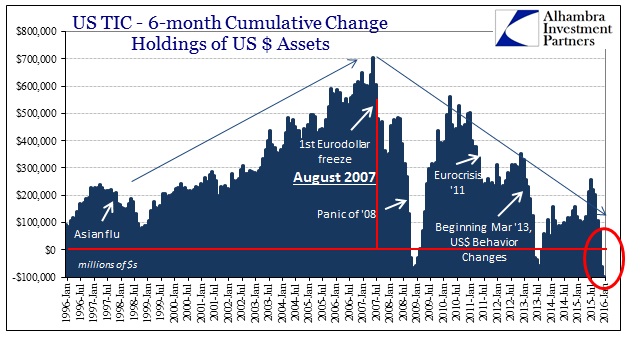

Behind it all was the eurodollar…some timely appreciation for it might have saved a whole lot of acute trouble and maybe would have pushed for some real reform (and then a real recovery to follow). What is really frustrating, maybe criminally so, however, is that monetary officials were debating eurodollars not in 2006 but rather 1979. At that early stage, the Fed along with other central banks couldn’t quite make out what it was, how it got there or where it was all going. They were even debating at that time whether a eurodollar was actually “money” at all.

Again, they decided it wasn’t, leaving to them what was on the official ledgers and nothing else. They have blinded themselves because they have thought all along their power completed and comprehensive. That has led to the perversion we find today, where what counts as money in the monetary statistics is mostly not, while what does not count or is even attempted to be counted actually is. Central banks have expanded the count of “not money” while actual “money” decays and falls apart. It explains a great deal about why things are the way they are, how it came to be that way, and begins to at least suggest what to expect coming down the road.

Stay In Touch