The emphasis on the labor market has become ubiquitous but it is not being used in the manner with which it should be used. It is now permanently attached to words like “despite” or “in contrast” no matter which economic data point is being described. The Wall Street Journal provides a perfect example in writing about the latest update for personal income and spending (as well as inflation).

Inflation remained modest in March, a sign that pricing pressures are in check amid slow growth in the U.S. and overseas, and low oil prices.

The slow price gains were accompanied by rising incomes and a savings rate that matched the highest level since 2012, suggesting caution on the part of consumers despite a robust labor market. [emphasis added]

The media keeps referring to this “robust labor market” but in every context it is only to describe why the opposite of what you would expect to find of such a thing is only going to be temporarily so. And they continue to do it even though “a robust labor market” has the entire time accompanied the “unexpected” appearance of all this negativity and weakness.

There is also the unspecified problem of “rising incomes.” The positive sign renders no significance, as the issue is the degree of positivity (lack thereof). In every account that still manages to be positive, it does so in the smallest of increments. The fact that it has continued in that manner for so long is both the pressing economic problem as well as the wiggle room by which the media can continue to emphasize only the plus sign. Real growth being so far in the past, they just assume nobody can remember what it was like.

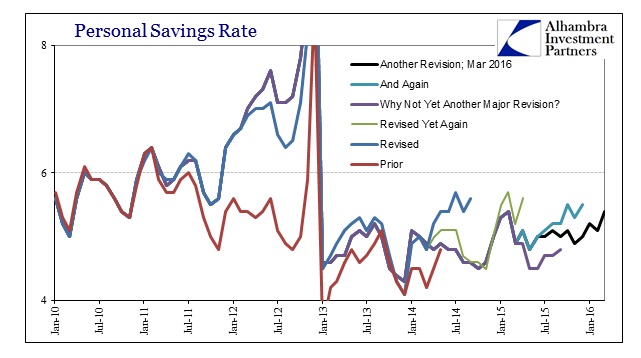

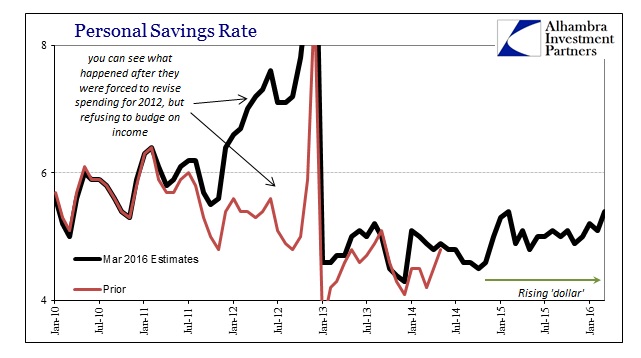

The savings rate rose to 5.4%, which may suggest caution as the Journal interprets, but the fact is we have no idea what the savings rate actually is or what it might be revised to in just a few months. The initial estimate for February was also 5.4%, which was revised this next month to just 5.1%. Over the past two years, the BEA has indicated a savings rate of 5.4% or above on nine prior occasions, but only one of those has survived the myriad revisions that regularly and significantly alter the fundamental view (from the PCE data perspective) of the aggregate consumer position.

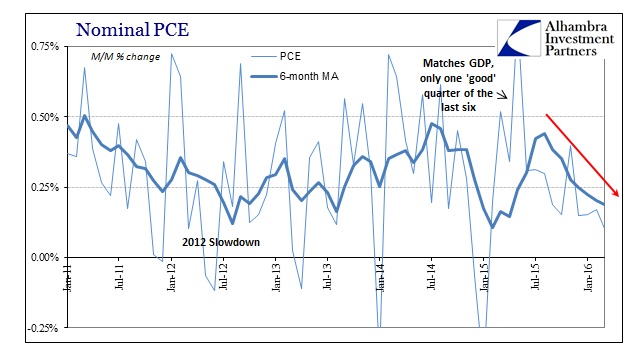

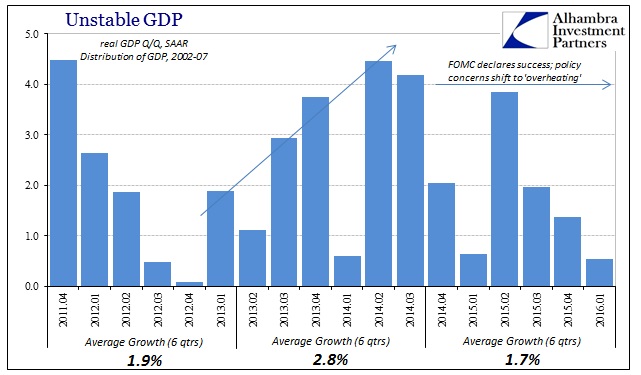

Nevertheless, the current estimate for the savings rate matches last February’s multi-year high which does seem appropriate in light of a wider survey. It is, for now, consistent with the noticeable slowdown in indicated consumer spending (including PCE for services) that began in late 2014. The month-over-month changes align almost perfectly with the trajectory of GDP especially in the last six quarters of intensifying weakness.

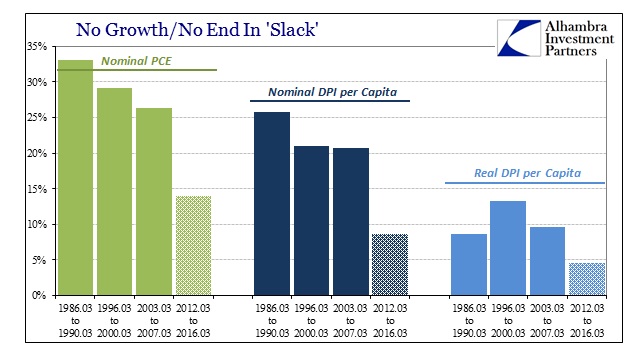

Subdued levels of spending are simply a function of subdued and stunted income growth. The fact remains, and this is all that really matters, incomes are so weak as to be depressive. There are any number of ways to see this quite easily, but in comparison to prior “cycles” there can be no doubt as to this deficiency.

Since March 2012 and the sudden appearance of the slowdown, nominal disposable personal income per capita has grown (positive numbers) by 8.6% total. That is much less than half the gain registered over similar 4-year periods in past recovery/growth phases. Even during the relatively weaker economy of the mid-2000’s housing bubble, per capita DPI gained almost 21%. It is then not at all surprising that nominal PCE would be of the same proportions; +14% the past four years as compared to +26.3% in the last cycle.

Factoring calculated inflation doesn’t alter the comparison. Real DPI per capita has grown just 4.5% this last four years, an unbelievably slow and paltry amount (from that we are supposed to expect “robust labor” to the point of “overheating”?) that is again less than half the gain registered in the middle 2000’s. And it is just a third of the increase of the later 1990’s when BLS labor statistics (Establishment Survey) were last comparable to now.

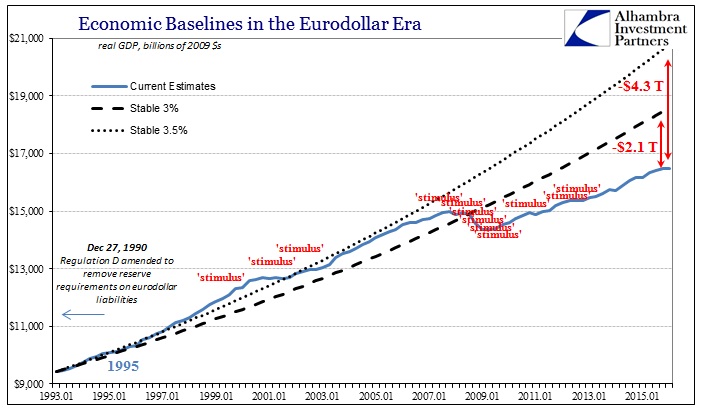

As I wrote earlier this week, it is and always has been about this dizzying deficiency in personal income. The word “rising” has no meaning, as incomes rarely fall in nominal terms even in recession. The degree has not changed despite four years of additional “stimulus” and all the assuring language that has gone along with wishing the unemployment rate was actually meaningful. The US economy, as the global economy, is in very rough shape and increasingly so. Rather than just accept it and try to frame it as a positive outcome, it is imperative that economists and policymakers (and the media) come to terms with reality – the economy as it is, not as it “should be.” After all, we are already $2 to $4 trillion behind where it really “should be”, which goes a long way to explaining why incomes remain so disastrously weak.

Stay In Touch