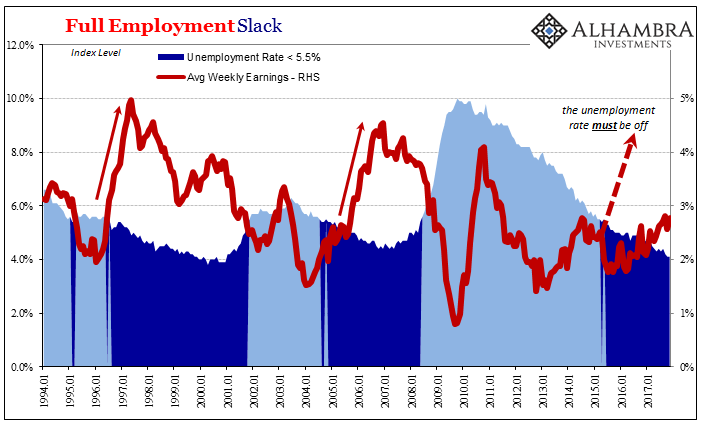

The biggest proponents of the BLS data have been FOMC policymakers. Right from the taper tantrum of 2013, the unemployment rate has given them, and the Economists who depend on their views for crafting their own, an almost definitive set of parameters for interpreting all other economic statistics. Everything is immediately filtered through the lens of the unemployment rate and some others.

It was why two years ago when manufacturing data all over the world was suggesting serious and sustained trouble, along with crashing commodities, interest rates, and even stocks for a time, the overall impression left in the mainstream was as if a different world altogether.

“It was pretty much everything you could ask for in a jobs report,” said Michelle Meyer, deputy head of United States economics at Bank of America Merrill Lynch. “Not only was the headline number strong, but there were upward revisions for prior months, the unemployment rate fell and wage growth accelerated.”

“The report was so strong and broad-based that it will be difficult to deter them from raising rates,” said Michael Gapen, chief United States economist at Barclays.

If you didn’t know when those quotes above were given you would be easily forgiven for placing them with any one but a handful of payroll reports over the past three and a half years. The latest jobs estimates for November 2017 were certainly characterized that way. Instead, the quote above was taken from an article written in November 2015 describing the “so strong” labor market of October 2015.

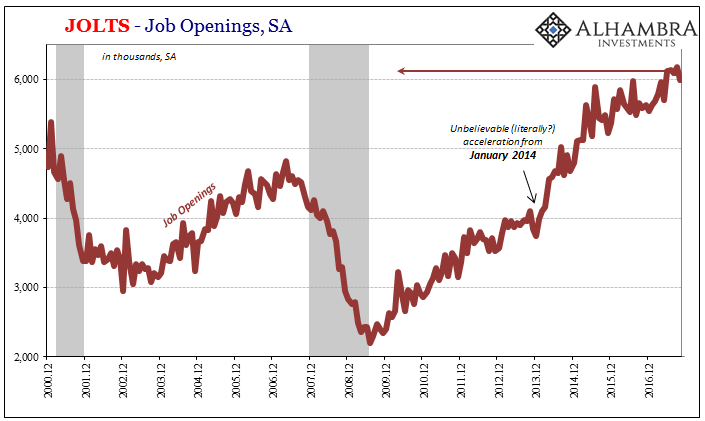

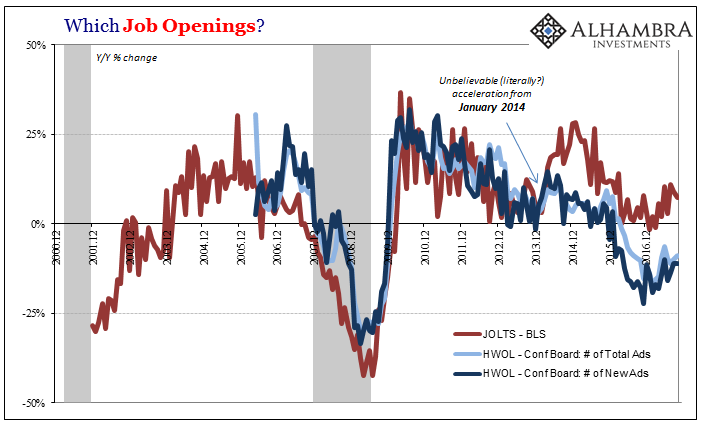

Wages are always accelerating in these quotes, if not in the data. One reason for the persisting expectation, as well as the characterization, has been JOLTS estimates for Job Openings. Going all the way back to economist William Henry Beveridge, there has been an assumed relationship between Job Openings and labor demand as a top-level proxy for the whole economy.

The BLS’s JOLTS series suggests a very, very sharp rise in JO during 2014, thus labor demand and therefore what seemed to be complementary estimates to this majority narrative about the economy. So it didn’t matter that wages weren’t actually accelerating as they should have been, since between the payroll reports and JO that would all come very shortly.

“The data now signal unambiguously that the labor market is unable to supply the people companies need. Usually, that means wages will accelerate, though the evidence for that now is mixed,” said Ian Shepherdson, chief economist at Pantheon Macroeconomics in New York.

The above (and below) was also pulled from 2015, this time in relation to the JOLTS estimates for that July.

“Will today’s blowout job openings number tilt the scales at all for next week’s Fed decision? One might think it should matter … but with data dependency apparently now extended to how equities trade, it is not certain how this report will shade their thinking,” said Michael Feroli, an economist at JPMorgan in New York.

That’s how twisted everything has become over the last decade. Here we have one major bank economist thinking it was stock prices rather than a serious downturn and global “dollar” illiquidity that was giving FOMC officials second thoughts about “rate hikes” despite a “blowout” economy. Maybe it was stock prices that the Fed cared more about in the end, but that’s not what was holding the real economy back then – or now.

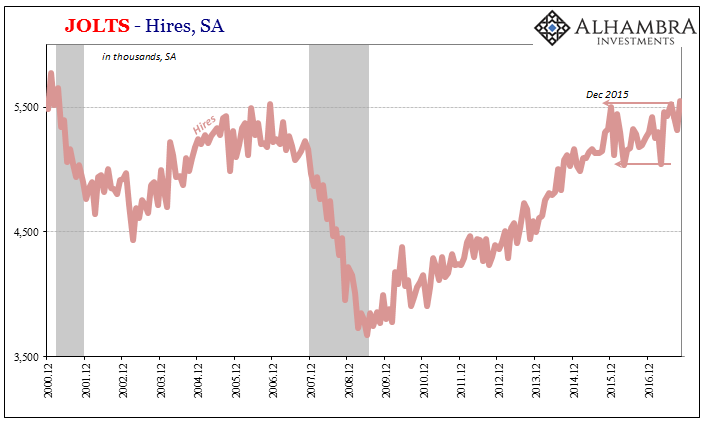

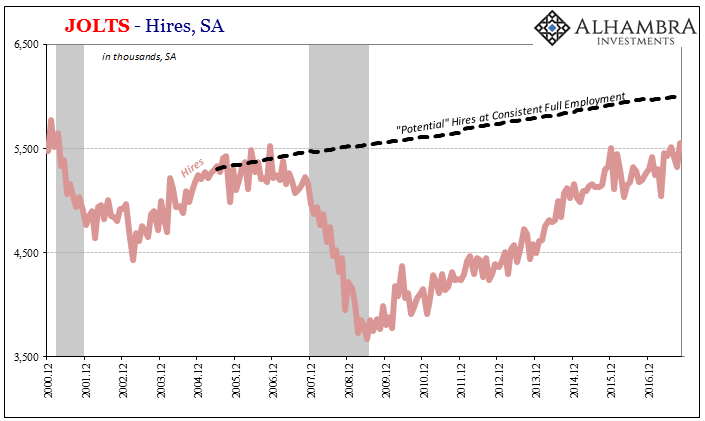

The latest JOLTS estimates are for October 2017 among the best. Job Openings are down only slightly from record highs the past few months, while Hires jumped to break above December 2015’s number to the highest level since before the 2001 dot-com recession.

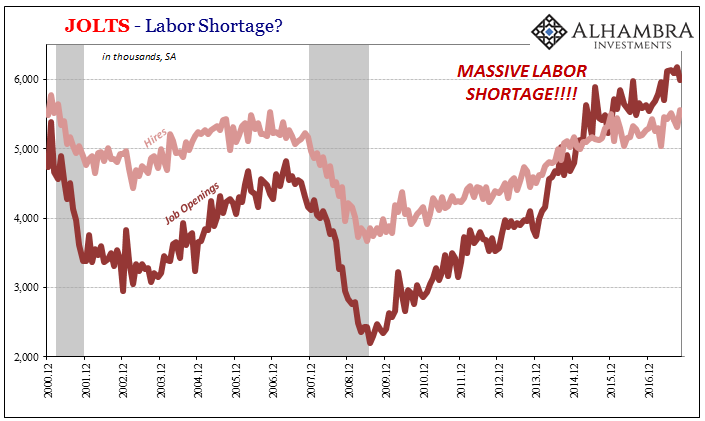

While both are viewed as very positive, it is the climb in JO over and above HI that drove the narrative. With labor in such high presumed demand beginning in 2014 but with hiring lagging if still rising, surely that meant the economy had been restored to full health if not going further past that point. Wage growth and inflation, therefore, was surely about to become a more immediate problem than the stubborn weakness of the first five years of “recovery.” For Economists, that could only mean “rate hikes”, maybe even more and faster than otherwise anticipated.

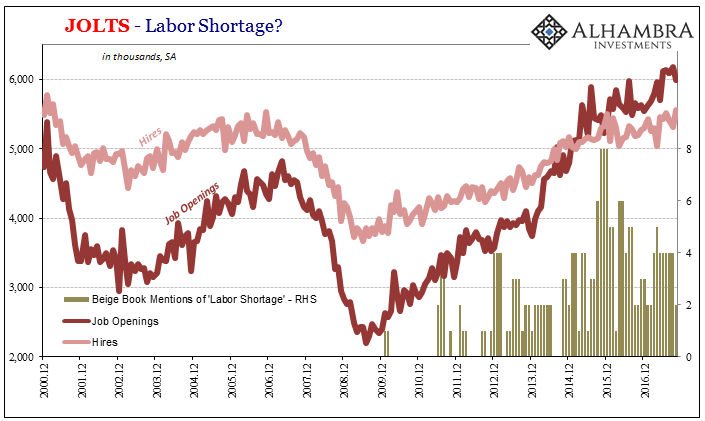

The problem with thinking this way in 2015, obviously, is by the time you get to the end of 2017 and none of it happens then you are stuck facing some very hard questions about everything you thought you knew. That’s why, among other things, the Fed’s Beige Book reached its “labor shortage” crescendo also in late 2015, with mentions of that possible factor trailing off noticeably in the two years since. Only questions remain.

What was certain back then is far less so today, perhaps even to a greater degree than is commonly understood (small wonder given what passes for mainstream economic commentary in general, let alone how much more it has been skewed whenever the unemployment rate is mentioned). Janet Yellen, who the media made such a fuss in 2015 over her labor market “dash board” including JOLTS JO, hasn’t completely changed her view this year, but she has at least started to wonder what’s really going on.

This is a big deal, as she said in Cleveland back in September:

My colleagues and I may have misjudged the strength of the labor market, the degree to which longer-run inflation expectations are consistent with our inflation objective, or even the fundamental forces driving inflation.

When you get away from all the media fluff and posturing, this is pretty simple stuff. You don’t even have to know much about labor market mechanics to appreciate this potentially awesome breakdown. Yellen expected that the BLS numbers in 2015 were accurate, therefore inflation and wages were sure to jump sometime shortly thereafter.

They didn’t.

Now two years have gone by and…nothing has changed in the economy while in the case of the labor market a lot is actually worse. Therefore, the only logical conclusion is that the BLS figures have been off to some considerable and significant degree.

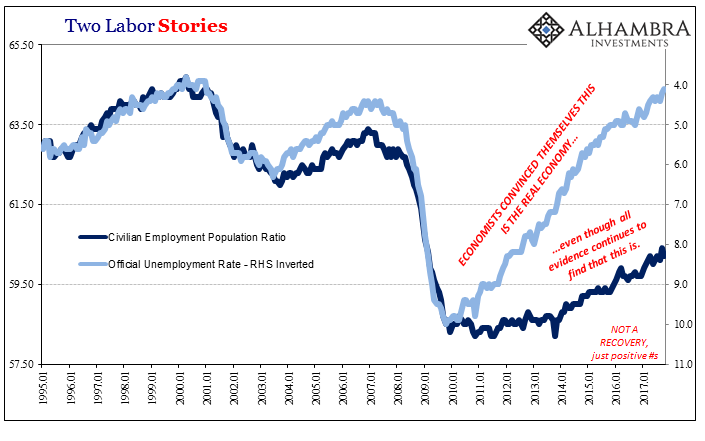

That brings back in the denominator of the unemployment rate, the one that has excluded so many potential American workers that given a 4.1% unemployment rate we have arrived at a binary possibility – either the ratio is correct and the every other economic account is way off, or it is completely wrong. They are no other options left.

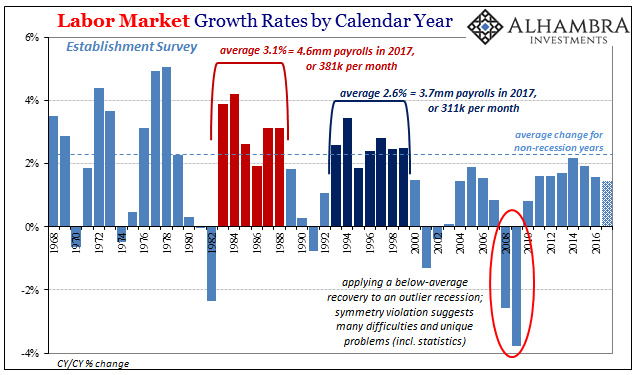

What, then, are we to make of labor demand, or JO? It has actually been problematic all along, not that you would know it from the commentary. Other versions of Job Openings (HWOL) never saw much gain in 2014 at all, and then got much weaker over the years since (though the Conference Board has yet to determine if or by how much technical factors are to blame).

If you take away JOLTS JO and then look at HI as well as other BLS estimates like the Establishment Survey in a more appropriate context (without even getting to questions about what it was really looking at also in 2014), you start much further along than where Janet Yellen was this past September.

What’s left is sheer bias; all the numbers have been there all along to refute the mainstream belief. Nothing has changed over the past three years, except now doubt where there should only be total vindication. There was always no way a “manufacturing recession”, and a global one at that, along with severe liquidity issues in “dollars” was ever consistent with “so strong and broad-based” as well as this “blowout” labor market. It never happened.

What did happen instead was an economy that is now seriously weaker for having gone through it all, and that includes the labor market no matter where Job Openings are.

Stay In Touch