On July 15, 2008, Federal Reserve Chairman Ben Bernanke sat in front of Congress for the second of his required Humphrey-Hawkins reports for that year. The original act meant for these to be more than bland economic obfuscation, where the original Full Employment and Balanced Growth Act of 1978 demanded monetary targets. The Fed stopped being able to produce them with any relevancy and meaning decades before. Now Bernanke had to answer for the consequences.

Except, of course, he didn’t. Instead, the Chairman kept to his platitudes about monetary policy being helpful and alleviating funding strain. Bernanke was cautiously optimistic following how he thought Bear Stearns was skillfully handled. He did acknowledge that significant problems remained, though especially careful to avoid all reasons why (because he didn’t really know).

These steps to address liquidity pressures coupled with monetary easing seem to have been helpful in mitigating some market strains. During the second quarter, credit spreads generally narrowed, liquidity pressures ebbed, and a number of financial institutions raised new capital. However, as events in recent weeks have demonstrated, many financial markets and institutions remain under considerable stress, in part because the outlook for the economy, and thus for credit quality, remains uncertain. In recent days, investors became particularly concerned about the financial condition of the government-sponsored enterprises (GSEs), Fannie Mae and Freddie Mac.

The very same day Bernanke was talking about them to Congress, the US Securities and Exchange Commission was issuing an emergency decree to protect Fannie and Freddie ostensibly from those evil speculators who seem to only show up when things are really bad. An easy scapegoat, one had to wonder why the stocks of these quasi-government mortgage giants (along with those of primary dealer commercial banks) would have required such extraordinary restrictions against naked short selling.

The mainstream answer is always that their falling prices are not reflective of fundamental values, and therefore require artificial assistance to adjust for artificial, speculative intrusion. Crony free markets don’t possess a downside, at least not officially – unless they are the bond market.

The funny thing about it all was that these so-called speculators were often the trading desks of these same banks. What do you do if you are holding boatloads of GSE paper, either directly or indirectly as some MBS guaranteed by the GSE’s, and the market starts to doubt valuations (black box) on all of them? If you have to, you dump them into an illiquid market but that makes things worse.

The first answer is to always hedge. That was one of the major reasons you bought the stuff in the first place. As a defined piece of a mortgage structure, its characteristics were supposed to mean control. If the price started to move against you in some way, you brought it back within tolerances (vol) with CDS or IRS. But what if there was no CDS available (or IRS) at reasonable costs? What if CDS disappeared entirely?

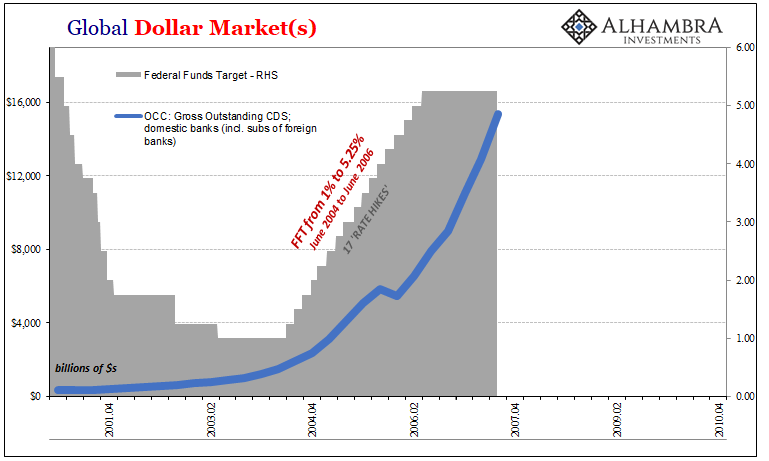

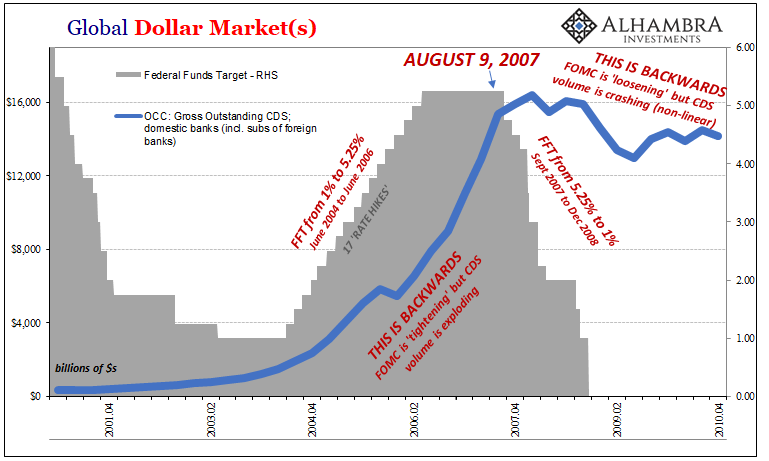

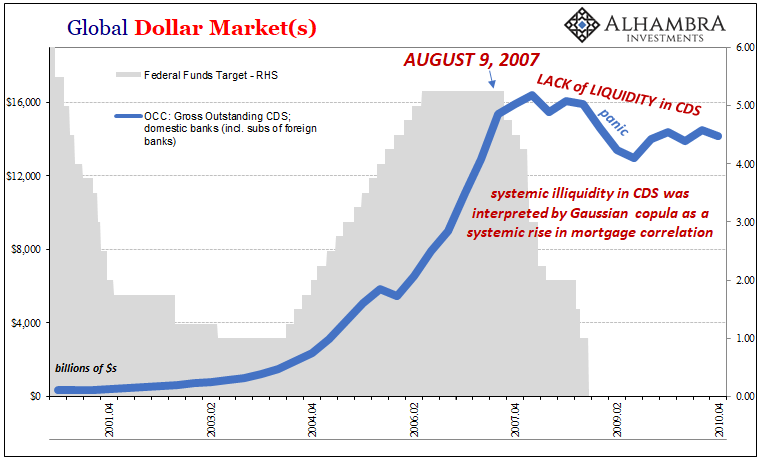

It’s not remotely a possibility anyone thought they would have to deal with before August 9, 2007. Like the Federal Reserve, banks were totally unprepared for that possibility when it became reality.

Unlike the Fed, there were consequences for funds and then banks being caught so exposed. Bear Stearns was that particular point driven home to every single boardroom and trading desk throughout not just Wall Street but the whole global banking paradigm. As I wrote today in looking back ten years, “Bear wasn’t some subprime peddler. It was Wall Street.”

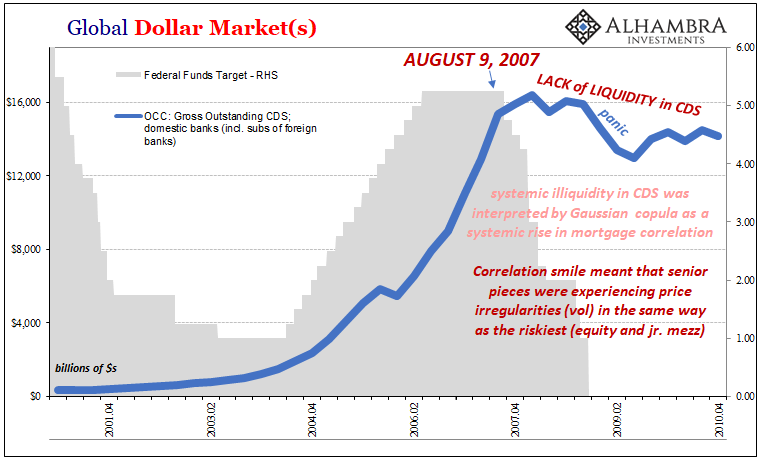

Without bank balance sheet flexibility in the systemic aggregate, dealers pulled back on risk absorption capacity, too (the money dealing activities in dark leverage like CDS). That had the effect of making the problem that much worse in two parallel ways – since correlation in MBS structures was derived from CDS prices, the illiquid pricing of even the best CDS (including all the ABX) created massive pricing problems that spread into repo (haircuts) far beyond just subprime.

On the other side, as demand for hedging against illiquid MBS pricing rose, there was nobody there to meet it with balance sheet supply. That created more problems for implied correlation pricing, and on and on it went.

Thus, if you couldn’t hedge your positions by laying off risk (vol) onto Merrill Lynch, for example, then you might surmise Merrill Lynch was itself in some similar degree of difficulty. If you couldn’t buy CDS from Merrill, then short Merrill’s stock as an ad hoc survival tactic. Or Fannie’s.

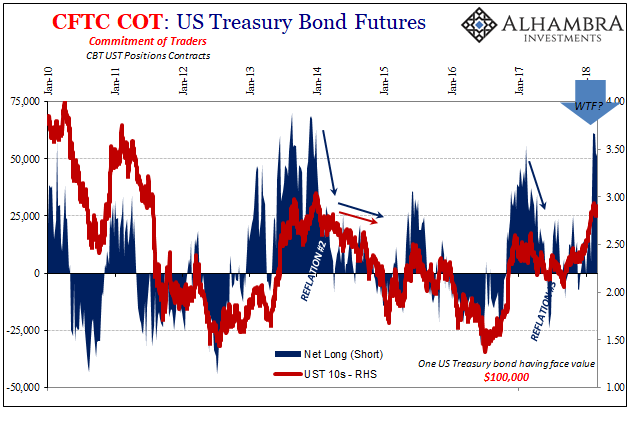

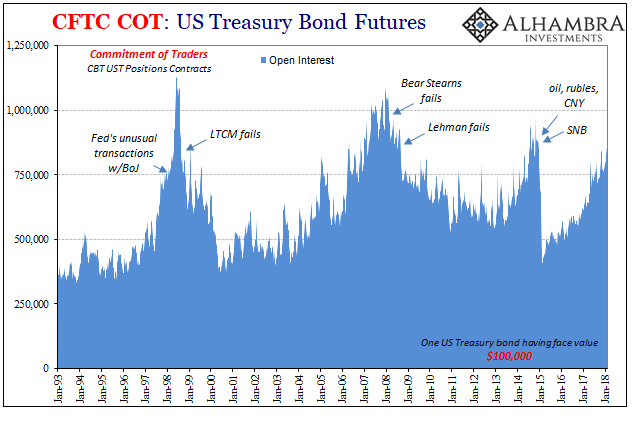

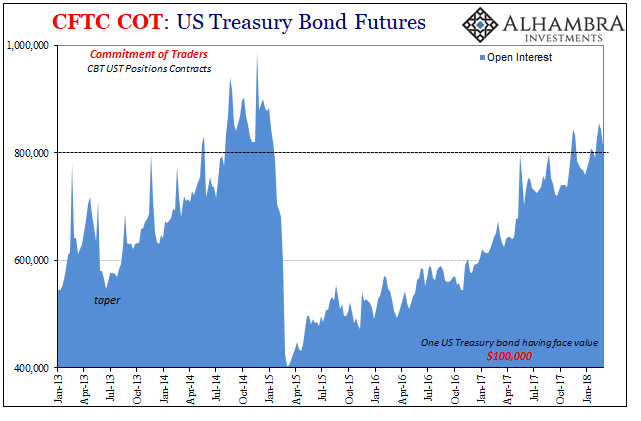

I bring this up both in the spirit of round numbers (ten years since Bear) but also to frame some very unusual recent activity in UST futures. If we thought WTI futures have been acting weird, they got nothin’ on bond futures.

Throughout the most recent BOND ROUT!!!! (with hysteria) the futures market had remained quite tepid about it. That was, to put it mildly, unusual. Then, all of a sudden, the week of February 2 (the big global stock selloff), the futures market in Chicago went crazy. The way it looks on the chart above is that bonds sold off and then futures traded to the selloff afterward. Except that doesn’t happen.

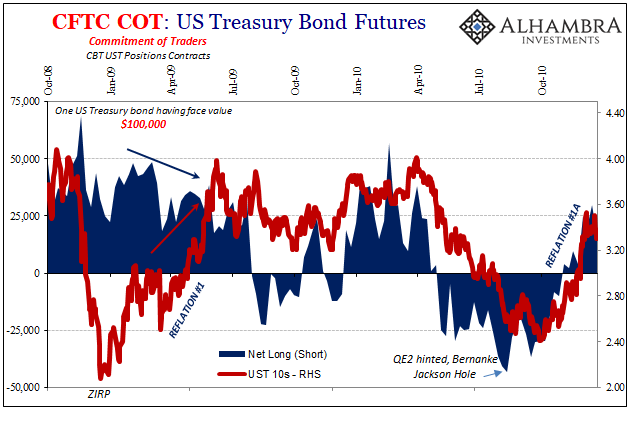

If you go back through each of the prior “reflation” selloffs, nominal yields, meaning UST prices, don’t lead. At most, they are concurrent changes but in all the big moves there is no large time lag between futures and bond prices. The last time anything close to that happened in the late crisis period after ZIRP and QE1 in December 2008.

The futures market wasn’t so optimistic about things, but bonds sold off anyway until about midyear 2009 when the two got together again (against “reflation”).

That’s, obviously, an interesting comparison given what was taking place in early 2009. Stocks were still being liquidated, balance sheet capacity still dangerously constrained (think negative swap spreads), and then heavy selling in UST’s which seemed positive except the futures market was still moving toward pessimism. In that last bit of 2009 liquidation, had evil speculators taken to selling UST’s, too, as another last ditch bypass hedge against the specter of early 2009’s trend toward full nationalizations?

What’s different today is the futures market after February 2. It suggests the possibility of similar constraint (if in very different ways) on hedging therefore balance sheet capacity forcing speculators to sell UST’s rather than the normal futures operations. They then appealed directly to futures when things were at their most recent worst, as an ad hoc ad hoc?

It’s a possibility I have raised before using nothing more than the big jump in open interest last year. UST futures tend to become very popular leading up to some of the worst moments of the last two decades.

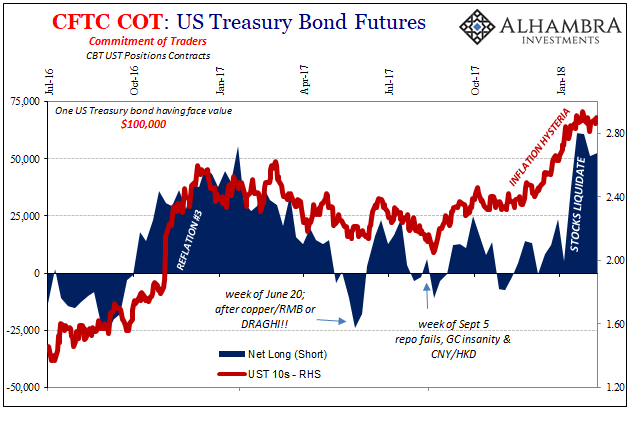

Some people are starting to get the sense that something’s wrong in funding markets by LIBOR-OIS. I’ve never preferred that metric because it’s unnecessarily esoteric. But the benefit to it this time is the blowout can’t be blamed on 2a7 like in 2015-16.

I recall last noticing ad hoc hedging (that time in the same way as 2008, short selling bank stocks) in lieu of more traditional risk capacity not all that long ago. It was also the last time LIBOR-OIS was similarly rising right at the start of February 2016. There’s always something benign to blame these constant problems on. I see another escalation.

Stay In Touch