The world is full of anomalies. It may seem like a paradox, but financial markets are particularly eventful places. Something happens, some people notice, and most often it goes…nowhere. It’s all the time and a constant part of analysis, trying to identify and separate what is truly contained.

The global eurodollar monetary system grew so far and so fast in large part because of what was perceived as a robust structure. Chock full of redundancies providing boundless options, flexibility was a key dynamic. Money markets operated in seamless fashion so that if you didn’t like one funding channel you could easily switch to another. There was tremendous capacity behind it all to make sure it was normal.

What happened on August 9, 2007, was the fracturing of the monolith. There was no single market for “dollars” any longer because there never was one to begin with. It seemed that way because while growing fast such energy provided the illusion of safety and flexibility. As it turns out, those redundancies proved to be just the opposite, fragile channels for spreading problems rather than containing them. Dysfunction revealed a tendency toward self-reinforcing negatives.

On this side of that divide, it’s not all chaos and contagion. Anomalies still happen, dysfunction is a constant feature, but there continues to be some minimal level of good function. The eurodollar may not work, but it at least keeps the lights on (for the most part).

But with greatly reduced function and resources (balance sheet capacity), there is a greater probability that the smallest thing becomes the proverbial snowball beginning its messy journey down the slope.

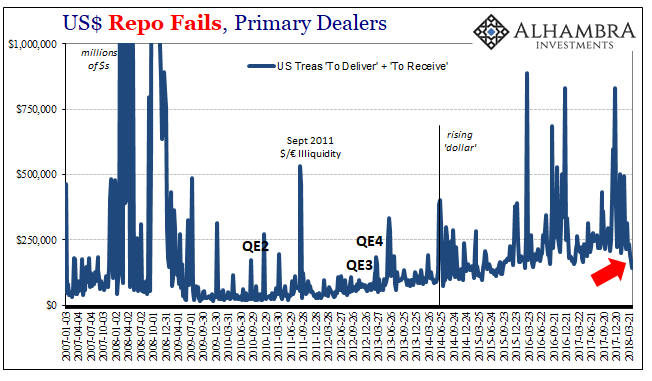

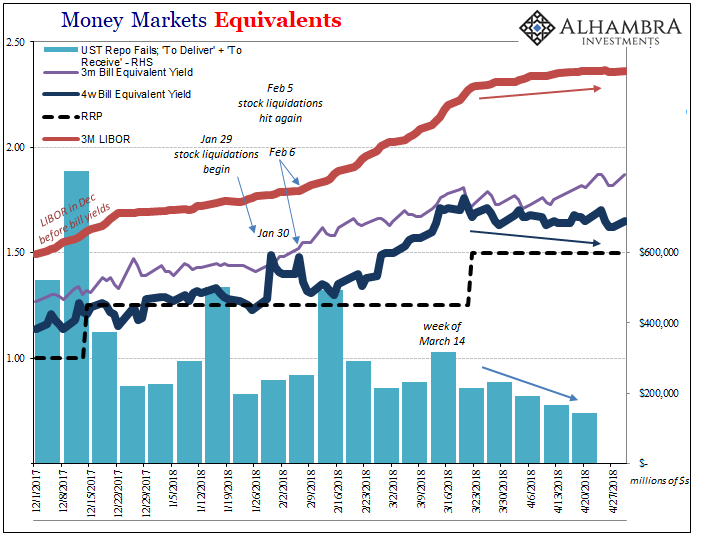

To put it into more specific terms, we might look at something like December’s massive spike in repo fails and immediately think that’s it! Something like that couldn’t possibly go unnoticed, and so “it” begins again. Fails spike, the dollar rises, and the next Lehman reveals itself no later than the following day.

These things aren’t one-to-one, however, and even the most violent crash is a lengthy process. False starts abound. Sometimes even in the most vital of funding capacities like repo, a surge in repo fails is just a surge in repo fails.

Then there are those other times.

Given that there was another jump in fails the week of January 17, 2018, it’s reasonable to question whether the repo market and collateral conditions may have played a role in what closely followed (specifically Japanese access to, and provisions from, them).

The worst of it was three months ago. That’s a lot of time for something like this, including a serious monetary “anomaly”, to remain relevant. And if that aberration had its genesis in the repo market, some recent indications suggest it may be over with.

To start with, repo fails that had been on an escalator for much of last year, culminating in the sharp spikes in December and January, have over the past few weeks retreated. Not just a little, either. During the week of April 18, fails posted just $143 billion, the lowest since September 2015 (February 2016 was close).

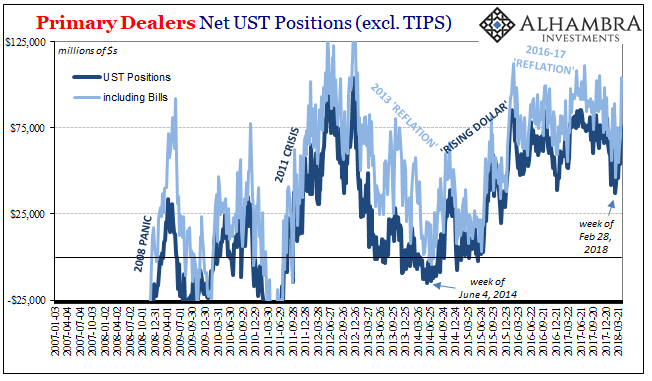

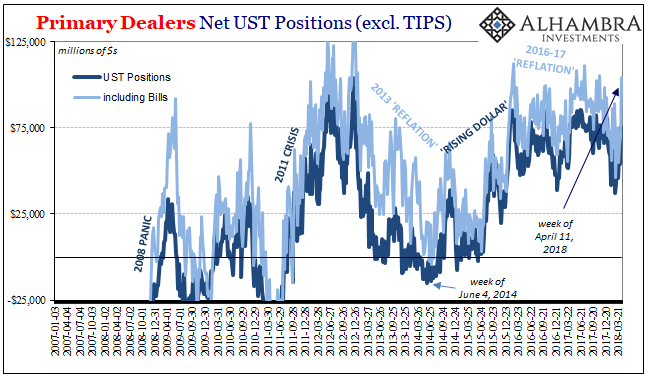

One of the essential elements in any negative collateral indication has been primary dealer participation. Either they are one cause of these disruptions in flow, or they announce its presence. They tend to hoard UST’s which correlates (not uniformly nor instantaneously) with fails, one of the few intuitive moving pieces in global wholesale eurodollars (dealers lend out less collateral, collateral flow drops, presto fails).

Throughout February, March, and into April (with a low the week of February 28), dealers were financing (hoarding) substantially smaller inventories of coupons and bills. It preceded the dramatic lowering in fails, suggesting first more favorable dealer activities and therefore a serious reduction in collateral strain (leading to better overall funding conditions outside of repo).

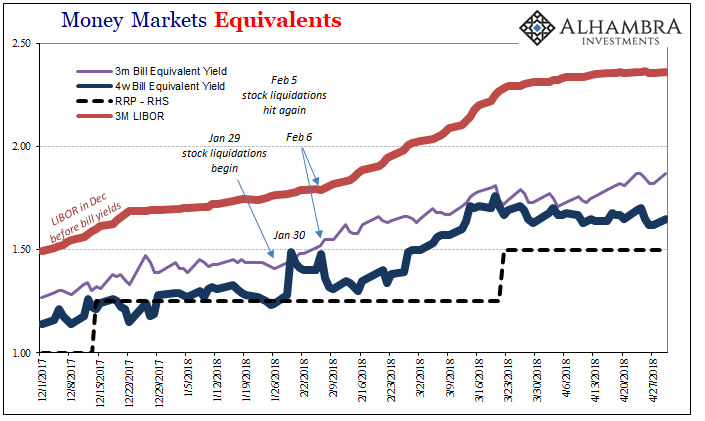

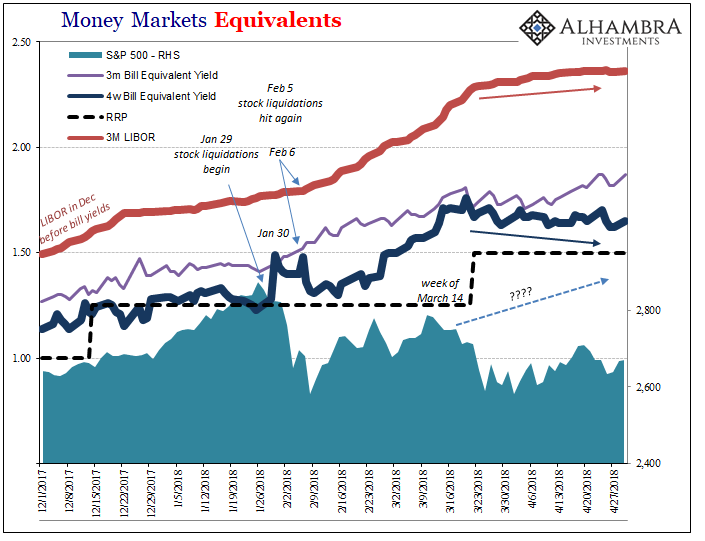

There was one more sizable uptick in fails the week of March 14, but from then on it appears the repo market has been better than perhaps any other time in years. It’s almost like the market needed one last one to get it all out of its system. After that mid-March disruption, money equivalents have noticeably smoothed (above). Unsecured rates are still moving up, just not at nearly the same attention-grabbing pace.

Liquidations over?

Maybe, but there is still that nagging feeling perhaps not. “Something” still isn’t quite right. As such:

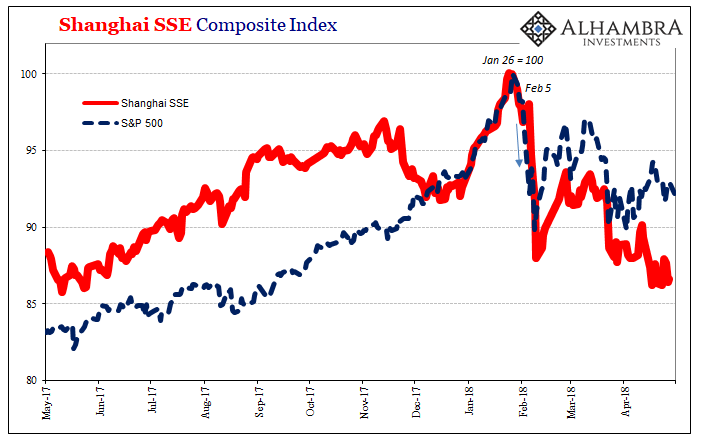

Bringing the stock market into the mix is always asking for complications. Stocks are savings and not money, therefore it isn’t a direct relationship. However, there should be no doubt that at times leverage plays an important role in at least setting the direction for the market, on both short and intermediate timescales.

In other words, you could point to any number of factors for why share prices haven’t retraced, from valuations to geopolitics, but we can’t ignore the timing. These “dollar” issues clearly played some role in what were undoubtedly global liquidations. That doesn’t necessarily mean that’s what is keeping stocks as they are, but it could be.

After that last episode in repo fails the week of March 14, stocks were again slammed in what looked like another liquidation. They haven’t recovered from it even though other money indications look so much better (including fails).

There are, of course, many other monetary angles to cover beyond just repo or even LIBOR-OIS. We also have to take note of FX. Just the fact that stocks were drawn into a global funding “anomaly” indicates there’s more substance to this one than perhaps other irregularities.

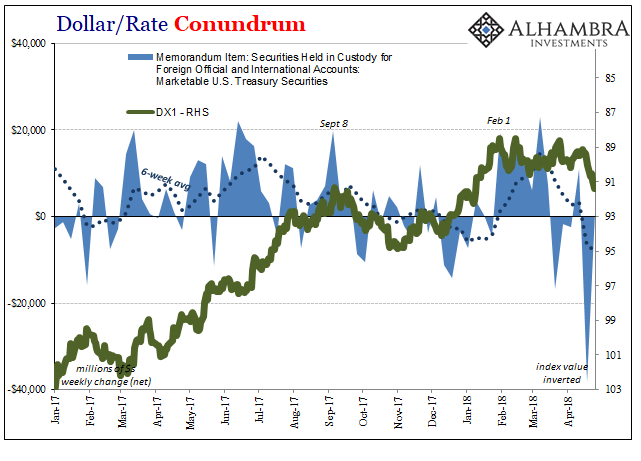

Among that latter category, I noted yesterday how the Federal Reserve reported a sharp drop in custodial holdings. While to many, if not most, that’s another bond market negative (foreigners are selling treasuries, BOND ROUT!!!!), it actually means something very different.

The US central bank holds in custody trillions of US securities, primarily UST’s, on behalf of foreign central banks, governments, and institutions. A decline in those balances indicates the same thing as those same reductions reflected in the TIC data – foreign entities either selling assets to raise “dollars” because of renewed “dollar shortage” difficulties or possibly transferring UST’s in some kind of collateral operation.

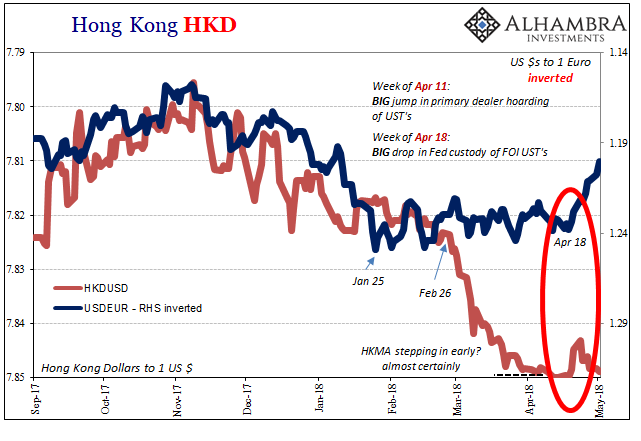

The big decline occurred the week of April 18. The week before that, the week of April 11, primary dealers reported a very sharp increase in net financed positions, or hoarding.

The very same week as the Fed custody data, “something” changed in the euro. The European currency had been one of the primary outlets of, let alone indication for, the “weak dollar” reflation trade consistent with so-called globally synchronized growth. In short, if the global economy is actually getting better it would do so by the dollar falling in exchange value with the euro a very big part of it.

That all stopped around the end of January as these global liquidations appeared (not just stocks). For several months, the euro traded more sideways, which, in a non-linear world, surely meant a significant shift across several key global funding pieces.

It has since been falling pretty steadily, meaning the “dollar rising”, going back to, surprise, April 18.

The week of April 11 was, to put a convenient finishing touch on all this, the same week HKD hit the lower band. The following week, April 18, was when the HKMA got serious about it (to little other than temporary effect).

What exactly is going on between Europe and Hong Kong (and China, and London, and NYC) is almost immaterial. I think what’s important to figure at this stage is more broadly about risk perceptions, the very notation that governs everything. They are shifting perhaps dramatically. For one, liquidations. That will get your attention even if you believe the Fed, you believe in globally synchronized growth, and were a full-throated, voluntary participant in inflation hysteria.

And then afterward, no quick retrace and putting it all behind as had happened before (such as “reflation” at the end of 2016). Instead, there have been only further issues fostering at the very least more uncertainty. Then we get HKD striking 7.85 really suggesting something other than transitory, maybe even some level of intractability.

To be perfectly clear, I’m not suggesting there is crash looming in stocks or even “dollars.” More realistically, what does seem to be happening is a widening of difficulties in terms of the dollar shortage and the dollar short. Rather than being an anomaly, we keep finding escalation.

That the repo market sat it out in late March and most of April doesn’t necessarily mean anything other than handing off problems into the next segment (FX). It could also be nothing more than the far side of reverberation, with renewed dealer hoarding April 18 indicating the possibility of the boomerang returning on its backward leg.

The big picture is this; whatever “it” is and has been, it doesn’t seem to be going away at least not yet. Instead, it may be snagging other parts of eurodollar and funding markets that were previously in “reflation.” It’s not just EUR, either; BRL, RUB, etc., all moving that wrong way again.

This is the downside of fragmentation, as if we needed a fourth demonstration.

Stay In Touch