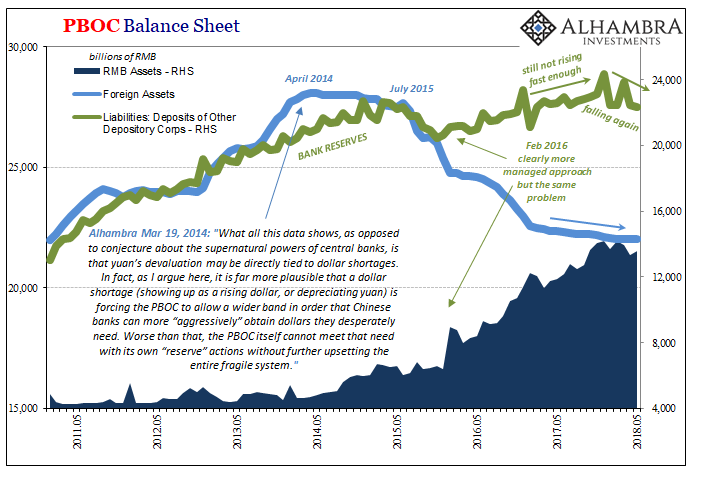

The level of Chinese bank reserves fell again in May 2018. Year-over-year, what is technically classified as Deposits of Other Depository Corporations on the PBOC’s liability (money) side of its balance sheet contracted by 1%. This advances a very different trend for reserves, breaking what had been a more continuous and determined effort toward at least minimal growth.

The central bank’s asset side persists in shrinking as China’s monetary authority has not been able to gain any new forex reserves. This despite the fact that CNY has (had) been able to significantly retrace its prior devastating decline. Without forex growth, the PBOC can only “print” RMB via its various window programs like the MLF and others in order to maintain some growth on the liability side.

The contraction now in bank reserves isn’t a surprise, at least not to us. It’s a development we’ve been tracking for two months (a more detailed explanation can be found there). I wrote last month:

To briefly review, China has a currency problem first and foremost; CNY DOWN = BAD. Chinese officials have tried everything to arrest the issue or have at times attempted to alleviate its worst tendencies. It appears as if they had early last year (after CNY continued falling even as “reflation” gripped almost every other place, especially around the EM world) settled on a stable CNY at all costs.

But that would have meant ending the remarkable RMB “printing” the PBOC had undertaken so as to keep its own asset side rising enough to produce positive bank reserve growth. It placed the central bank in quite the conundrum.

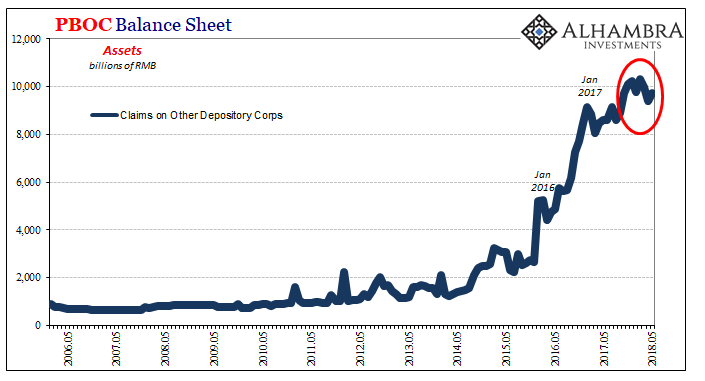

Banks did repay on the MLF in April, but not again in May. The PBOC’s asset item encompassing interbank borrowing gained some back last month, somewhat against the stated purpose. It’s not easy to tell why that may have been, since there are several technical and regular factors that are, to be frank, quite impossible to distinguish from what officials are clearly trying to do here.

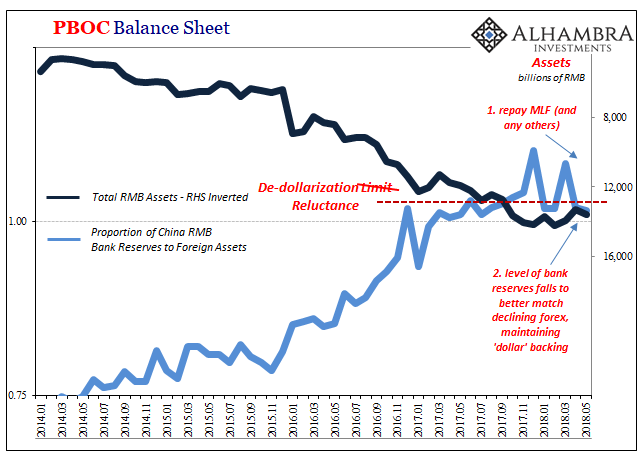

At least in terms of bank reserves, the results are clearer. Their reduction regardless of other lending activities in RMB has left them right back in the same zone of what now sure seems like a hard policy limit. The coverage relationship between bank reserves and their “backing” by forex assets on hand (shown below) is pretty well established for going on eighteen months – the same year and a half where CNY has been far better behaved toward appreciation.

That CNY hasn’t been so accommodative (“devalue”) lately might suggest one possible reason why the tinkering with bank reserves, the MLF, and RRR’s.

We can’t know for sure any direct effects this decline in bank reserves might have on China’s markets and economy, it’s still too early to draw solid conclusions. For one, things haven’t been very good for either case this year.

Still, it’s hard not to notice and engage in semi-reasonable speculation.

To put it in very broad terms, the Chinese seem very intent on prioritizing stability over growth despite the not having obtained much growth since 2016. Maybe the latter part explains the former; we tried, it didn’t work, now what?

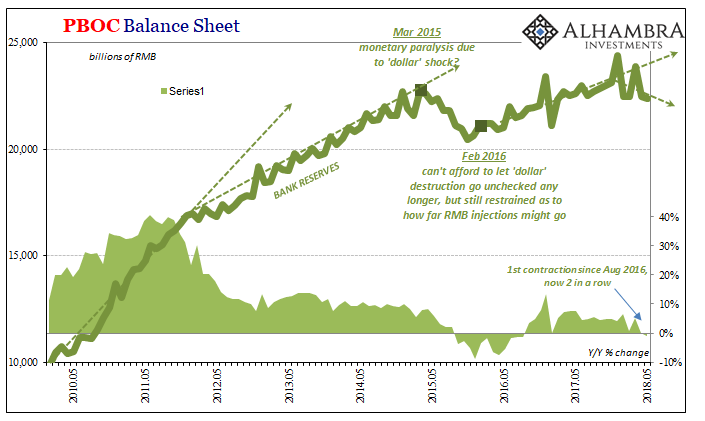

My own view is more along the lines of Uncle He’s, if Liu He was in fact the author of that infamous 2016 article. Everything the Chinese have done even as far back as the first rumblings of the “rising dollar” in later 2013 can be seen as prioritizing stability. That’s why, I believe, they were reluctant to intervene until 2016, allowing bank reserves to contract catastrophically in the middle of 2015 (mistakenly hoping, as now, the private banking system would use RRR cuts to offset that decline and maintain a neutral liquidity environment).

What’s been changing over these few years is what officials are attempting to stabilize at any one time. In one respect, they may have succeeded in getting the economy into that condition with massive “stimulus” Western Economists mischaracterized as being for recovery. The bleeding was staunched in February 2016, but only as far as further economic deceleration.

That might have allowed them to pursue CNY with so much vigor (which is the only way to characterize HK’s entry into all this) the following year, last year. So long as the economy might stay about where it is and has been, then continuing to advance a CNY-first policy could make (some) sense. But it’s the smallest needle to try and thread with such blunt instruments and a global background (“dollar”) that just isn’t going to cooperate. The best of only bad options?

Not only is the PBOC at risk of the eurodollar’s perpetual non-cooperation, the global monetary system has displayed the terrifying habit of throwing additional fits at the worst possible times, according to central bank projects of this nature. Might the events of the last two months be characterized that way? This, too, could explain why in April of all months there was suddenly more effort toward CNY via the PBOC’s RMB assets and liabilities as I’ve described.

Thinking ahead, what would happen if China’s economy starts to decelerate once more as it did in 2014 and 2015? Which one would the PBOC choose then, economy or currency? In fact, contrary to the governing narrative that presupposes this one central bank near omniscient powers, it might not be able to do much of anything given current constraints (including HKD). Not that it might not try.

It may be that Chinese authorities have backed themselves into a corner. And it also may be that Chinese authorities have been preparing for that corner. The problem for the rest of the world is nobody else is.

Stay In Touch